Last week’s post-US NFP rebound has given NZD/USD some breathing room, but it has done little to convince traders that the recent downtrend has run its course. With the Reserve Bank of New Zealand set to announce its policy decision this week, the Kiwi now faces a catalyst that could determine whether the recovery develops into something more durable or simply marks another pause before sellers return.

The challenge for the RBNZ is that the arguments for both holding and hiking have become increasingly compelling. Inflation has stayed uncomfortably high after this year’s oil shock, supporting the case for pushing interest rates back toward neutral sooner rather than later. Yet domestic demand is still subdued, unemployment remains elevated and geopolitical risks have eased following the US-Iran ceasefire, reducing some of the urgency for another immediate tightening move.

That dilemma is reflected across the policy debate. The NZIER Monetary Policy Shadow Board marginally favors leaving the Official Cash Rate unchanged at 2.25%, but characterizes the July meeting as an exceptionally close call. Members supporting a hike cited persistent inflation pressures, while others argued the economic effects of the earlier energy shock and slowing domestic activity justify waiting for greater clarity. Importantly, there is little disagreement over the medium-term direction of policy, with most members expecting the OCR to climb toward 3.00%-3.25% over the next year.

Forecasts from New Zealand’s major banks tell a similar story. ANZ and BNZ expect a 25 basis point increase this week, though ANZ believes any move should be accompanied by balanced guidance to avoid boxing policymakers into an overly aggressive tightening path if economic data weakens. BNZ likewise argues inflation risks have not disappeared despite the improvement in global geopolitical conditions.

ASB and Westpac instead expect the RBNZ to stay on hold. ASB reversed its previous forecast for a July increase after the easing of Middle East tensions, while Westpac believes policymakers are now more likely to reach a consensus in favor of waiting than they were at the May meeting. In both cases, the emphasis is on allowing more time to assess whether inflation pressures continue to broaden after the energy shock.

As a result, markets may focus less on the headline decision than on what comes next. A hold that signals another hike is only being delayed could limit downside in the Kiwi. Equally, a 25 basis point increase accompanied by softer forward guidance may fail to generate lasting gains. Investors will be looking for clues on how quickly the RBNZ expects policy to move back toward neutral rather than treating this week’s decision in isolation.

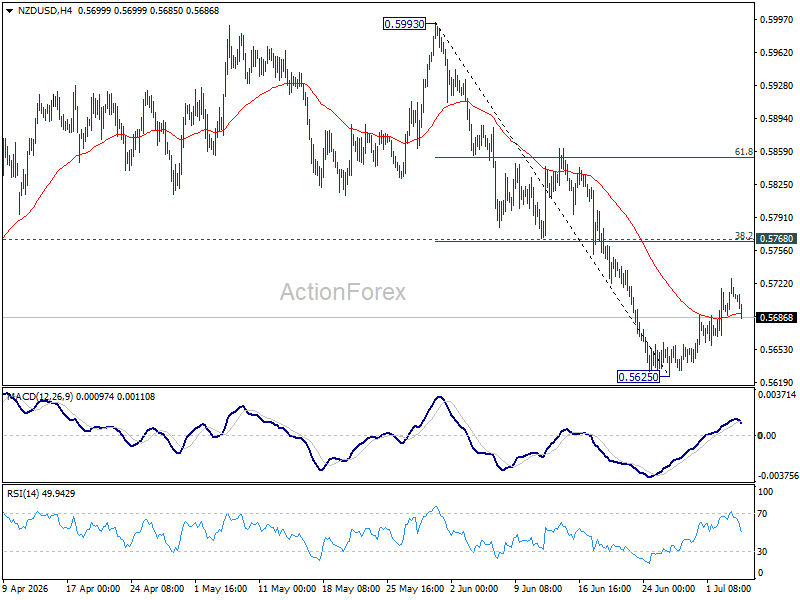

Technically, NZD/USD still looks vulnerable. The recovery from last week’s lows was driven largely by broad-based Dollar weakness after the softer US employment report rather than a meaningful improvement in New Zealand’s outlook. As long as 0.5768 cluster resistance (38.2% retracement of 0.5993 to 0.5625 at 0.5766) continues to cap rallies, the near-term bias stays tilted to the downside. A break below 0.5625 would resume the decline from 0.6092 towards 0.5579 structural support.

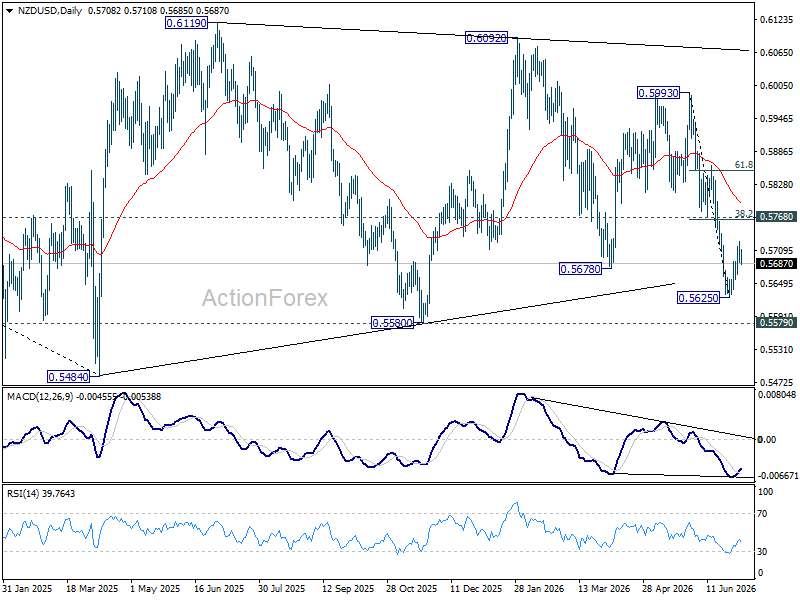

The longer-term chart tells a similar story. The price action from the 2025 low at 0.5484 continues to look corrective within the broader downtrend from the 2021 peak at 0.7463. While momentum has not yet confirmed a decisive bearish breakout, sustained trading below 0.5625 would suggest that correction has run its course and increase the likelihood of another test of the 2025 lows.

{kind=link}