Financial markets spent much of today’s session waiting rather than reacting. Most major currency pairs traded comfortably within yesterday’s ranges as investors resisted making large directional bets ahead of tomorrow’s RBNZ decision and next week’s US inflation report. Dollar and Yen were the day’s strongest performers, but neither attracted enough follow-through buying to establish fresh trends, underscoring a market searching for its next catalyst.

The relatively subdued price action in USD/JPY also suggests both bulls and bears are becoming more selective. While the pair remains close to last week’s 40-year high, Dollar bulls have shown little appetite to force a breakout. Traders recognize that, for Japanese authorities, intervention is more about timing than any specific exchange-rate level. Thin-liquidity periods, when official buying can have the greatest market impact, remain the preferred windows for action.

For the Dollar, the next meaningful opportunity to establish direction is likely to come from next week’s June CPI report. Last week’s weaker-than-expected payrolls reduced expectations for an earlier Fed rate hike, but they did not overturn the broader view that policymakers still expect one increase before year-end. Inflation data therefore remain the key test of whether the Fed’s more hawkish June projections will ultimately be validated.

Kiwi, meanwhile, lagged ahead of tomorrow’s RBNZ meeting, where policymakers face one of the most evenly balanced decisions of the year. The NZIER Shadow Board recommended leaving the Official Cash Rate unchanged but described the decision as a “line-ball” call. That uncertainty is echoed by New Zealand’s major banks, with ANZ and BNZ expecting a hike while ASB and Westpac forecast another hold. With conviction low on both sides, markets appear content to wait for the policy statement rather than speculate aggressively beforehand.

Yet perhaps the more interesting debate this week has not been about where rates are heading, but about how central banks should communicate them. A philosophical divide has emerged within the Federal Reserve over the role of forward guidance, raising broader questions about how investors should interpret future policy signals.

Kevin Warsh — structural skeptic, near-blanket opposition

Fed Chair Kevin Warsh’s position isn’t “use it carefully,” it’s closer to “don’t use it, full stop, for now.” At his first press conference (June 17) he declined to submit a dot-plot projection at all, explicitly because of his opposition to forward guidance, making him the only one of 19 policymakers with no dot on the chart. He shortened the FOMC statement itself from 341 words to 132. His stated logic: forward guidance can lock policymakers into positions too early and compound mistakes when the economic picture shifts, and financial markets have become too dependent on Fed signaling in a way that reduces the Fed’s own flexibility.

At the ECB’s Sintra forum (June 30), he went further, framing this as a philosophical stance shared with other central bankers rather than a Fed-specific policy quirk — arguing central banks should stop trying to predict the economy, alongside ECB’s Lagarde, BoE’s Bailey, and BoC’s Macklem, who separately voiced the same skepticism. Lagarde’s framing is telling: she said she regretted having “felt bound and compelled by forward guidance” — Warsh is positioning this as guidance-as-trap, not guidance-as-tool.

He’s held this line even under pressure to clarify next steps: as recently as July 1 he declined to say what the Fed would do next, saying “I’m not going to make a judgment now… the tactics, the strategy, and the rest, that’s still to come.”

Christopher Waller — tool-specific, situational usefulness

Governor Christopher Waller’s framing is narrower and more conventional central-bank-economist: forward guidance can aid the transmission of monetary policy by influencing expectations and market reactions — evidenced by Treasury yields moving ahead of actual rate hikes — but it’s not appropriate in all cases. That’s a “right tool for the right regime” argument, not a rejection of the concept. Waller has separately been on record wanting the Committee to strip out any easing bias and move to a more neutral policy stance — a substantive rate-path view distinct from Warsh’s process critique.

Where the contrast really lies

The interesting split isn’t hawk-vs-dove — both are currently reading the data cautiously given May’s 4.2% CPI print — it’s methodological: Warsh’s objection is closer to epistemic (he thinks the exercise of publishing forward paths is itself flawed and creates false precision that constrains later decisions), while Waller’s is closer to operational (guidance is a legitimate instrument, deploy it when the transmission mechanism benefits, hold back when it doesn’t). Waller would likely still show up on a dot plot with a number; Warsh pointedly won’t. That’s a genuine philosophical difference about the Fed’s communication function, layered on top of whatever their individual rate-path views happen to be.

For investors, the implication is straightforward. If the Fed gradually shifts toward Warsh’s philosophy, markets may receive fewer explicit policy signals and become increasingly dependent on incoming data. That would make releases such as CPI, employment and inflation expectations even more important, reinforcing the transition already taking place in FX markets toward a world driven less by central bank guidance and more by country-specific economic fundamentals.

Bitcoin Passed a Key Stress Test. Now Comes the Hard Part.

Bitcoin’s biggest story last week wasn’t its rebound above $60,000—it was the market’s ability to absorb a $216 million sale by Strategy without breaking lower. That resilience suggests much of the recent forced selling may have already been flushed out. We examine why a near-term base could be forming, why a durable market bottom is still unconfirmed, and the technical levels that could decide Bitcoin’s next major move. Read More.

GBP/CHF Nears Trend-Reversal Zone as Political Risk Fades and Sterling Shorts Unwind

Sterling’s rally has been driven less by improving UK fundamentals than by the rapid unwinding of political risk and one of the market’s largest speculative short positions. With the Bank of England maintaining a restrictive policy stance and GBP/CHF approaching a major technical resistance zone, the conditions for a medium-term bullish reversal are falling into place. Read More.

ECB’s Panetta: Fragile Outlook Means No Predetermined Path for Rates

The ECB should not lock itself into a predetermined policy path, according to Governing Council member Fabio Panetta. While inflation risks remain elevated, he warned that the Eurozone’s fragile growth outlook and ongoing geopolitical uncertainty require policymakers to stay flexible and data-dependent. Read More.

Japan Real Wages Extend Longest Growth Streak Since 2021

Japan’s wage growth remained solid in May as real wages extended their longest positive run since 2021, while household spending declined far less than expected. The latest data point to improving household purchasing power and resilient consumer demand despite moderating wage momentum. Read More.

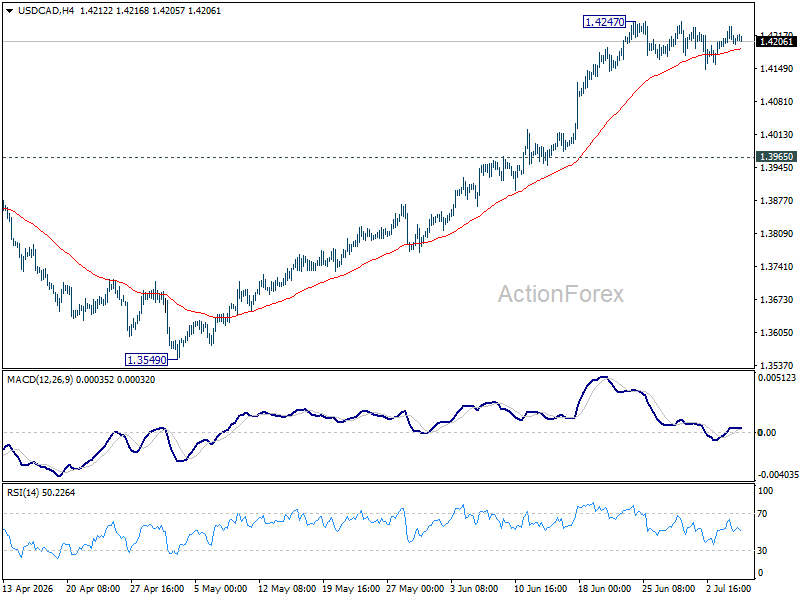

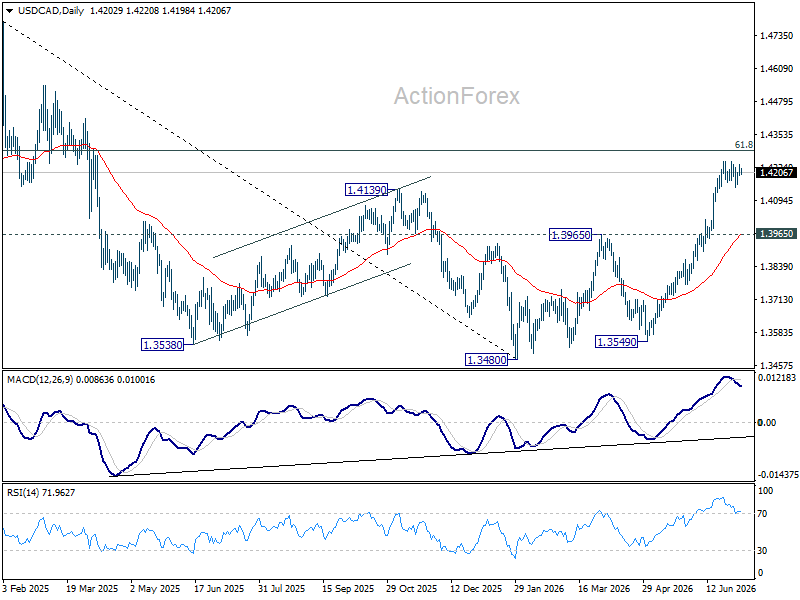

USD/CAD Daily Outlook

USD/CAD is staying in consolidations below 1.4247 and intraday bias remains neutral. Deeper pullback cannot be ruled out. But downside should be contained above 1.3965 resistance turned support. Above 1.4247 will resume the rally from 1.3480 to 61.8% retracement of 1.4791 to 1.3480 at 1.4290. Firm break there will pave the way back to 1.4791 high.

In the bigger picture, current development suggests that fall from 1.4791 has completed as a three wave correction to 1.3480. It’s still early to judge if rise from there a corrective bounce, or resumption of the larger up trend from 1.2005 (2021 low). But in either case, retest of 1.4791 high should be seen next.

{kind=link}