- The RBNZ raised the OCR by 25bps to 2.5%. The decision was reached by consensus.

- The balance of the Committee seems unchanged: Gai, Gourley and Hansen remain hawkish while Breman, Conway and Silk remain more dovish.

- A key argument for the hike is a concern that financial conditions would have eased further if the OCR was left unchanged.

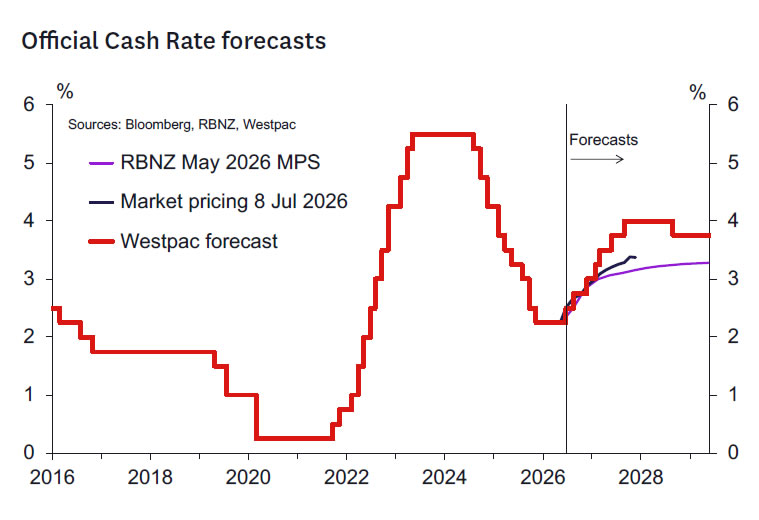

- The MPC seems to be comfortable with an end 2026 level of the OCR in the 2.75%-3% range – not very different from that shown in the May forecasts.

- Westpac expects follow-up 25bp hikes in September and December and an unchanged sequence of 25bp increases through 2027. Hence the peak OCR of 4% is reached in September, instead of December 2027.

OCR Raised by 25bps to 2.50%

Today the RBNZ raised the OCR by 25bps to 2.50%, in contrast to our expectations for an ‘on hold’ decision. The decision was reached by consensus and hence no vote was required.

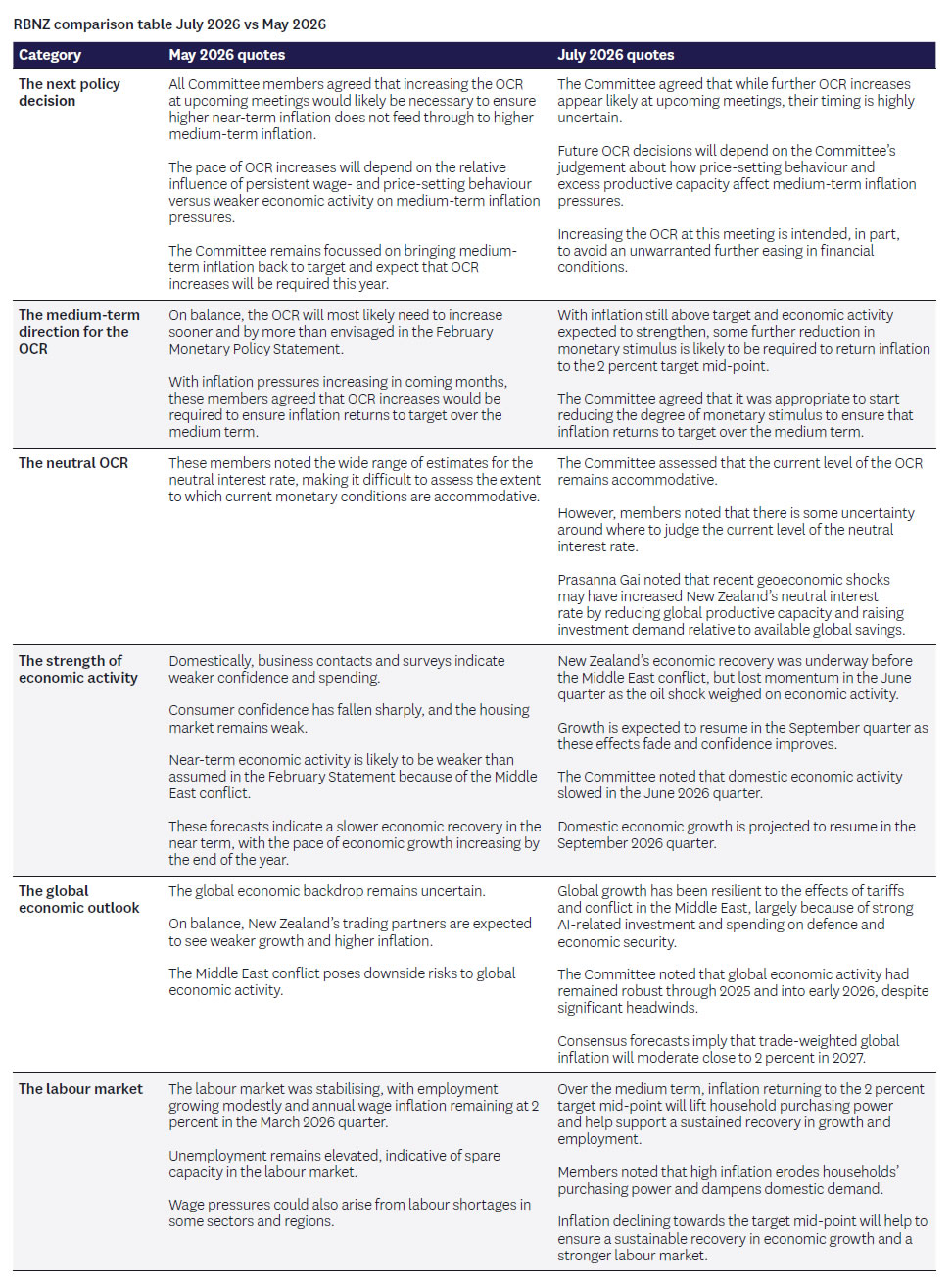

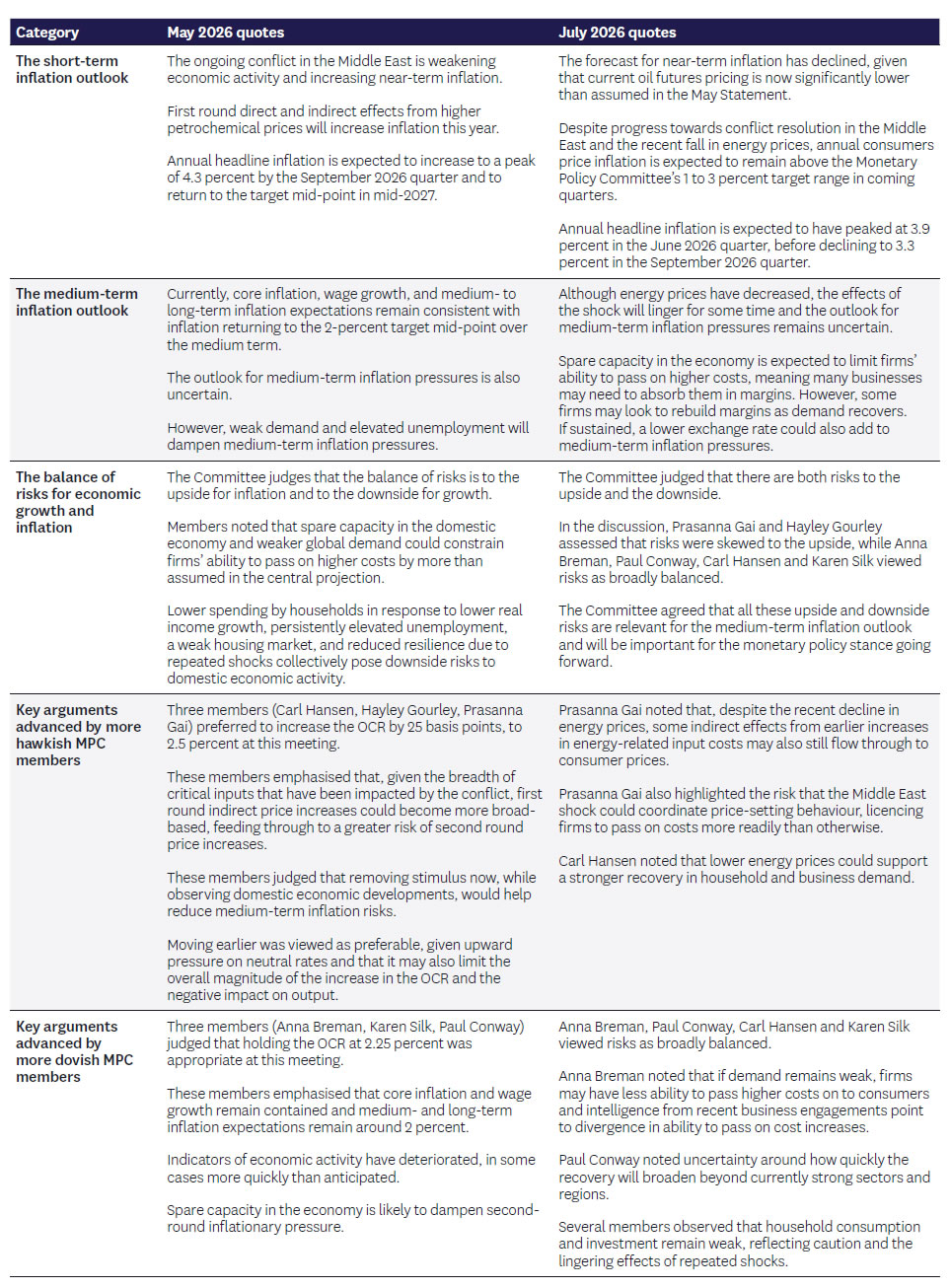

A comparison of key quotes from the July MPR statement and Record of Meeting with that from the May MPS meeting is provided at the end of this document.

The RBNZ has recognised the fall in oil prices and inflation risks that has been seen since May. Their forecasts for inflation have been revised down such that annual inflation is expected to be 3.9% in Q2 and 3.3% in Q3. These forecasts are a bit lower than our own (3.7% for Q3 in our case) but still demand OCR increases in 2026 by the MPC’s thinking.

The RBNZ recognizes that the risks around the global growth outlook are better balanced relative to those seen back in May when energy prices were much higher.

A key argument cited as supporting the case for an OCR hike today was the risk that an unchanged OCR might have prompted a further easing in financial conditions. This could have occurred through some combination of expectations of a lower end 2026 OCR and a weaker exchange rate. This suggests the RBNZ remain comfortable with the end 2026 OCR in the 2.75-3% range given where market pricing has sat in the last week or so.

The RBNZ indicates some further tightening is likely over coming meetings but notes the timing of these interest rate increases remains uncertain. The strategy seems to be to bring the OCR back to the neutral zone. For now, an OCR in the low 3% area seems to be viewed as consistent with that objective. However, there is uncertainty around where the neutral OCR is. Prasanna Gai noted a risk the neutral rate is rising in this less certain geopolitical environment. Paul Conway noted in the press conference that short-term estimates of the neutral OCR are being boosted by the higher short term inflation profile and the resultant impact on short term inflation expectations.

The balance of the MPC appears unchanged: the hawks remain Gai, Gourley and Hansen while the more dovish group includes Breman, Silk and Conway. Gai and Gourley see upside risks to the inflation outlook while the rest see the inflation risks as better balanced.

The RBNZ’s rhetoric on the key factors driving future OCR increases has shifted a little. In May the Governor emphasized the importance of indicators of second round pricing pressures, rising inflation expectations and wage pressures. No evidence has accumulated since May on these risks. Nevertheless, these factors are still seen as important, but now signs of strengthening domestic and global growth are being added to the list of relevant factors. Trends in financial conditions seem also to be on the list of relevant factors. The potential inflationary impact of the exchange rate is playing a role here.

The RBNZ also decided to bring forward slightly the time at which the LSAP portfolio will be fully extinguished to June 2027. This does not have any monetary policy implications and is portrayed as being largely technical in nature.

Westpac Outlook – 4% Peak in the OCR Reached a Little Earlier in 2027

Looking ahead, we continue to expect the 25bp increases in the OCR that we forecast prior to today’s meeting – at the September and December meetings – although these will now leave the OCR 25bps higher at year end (at 3.0%) than we had forecast previously. Thereafter, we continue to forecast a peak OCR of 4.0% next year, although our central expectation is that this will now be reached three months earlier at the September 2027 MPS meeting. In the current uncertain environment, it goes without saying that the evolution of monetary policy will depend on how both global events and key data evolve (we summarise the near-term economic diary below). Therefore, as the RBNZ noted itself today, the exact timing of the tightening profile is highly uncertain and even the tightening we forecast at the September 2026 meeting should not be regarded as a “done deal”.

Things to Watch Ahead of the 2 September Meeting

The RBNZ’s next policy review is on 2 September, when it will also publish a full Monetary Policy Statement (MPS) and refreshed economic forecasts. How the RBNZ’s policy stance evolves between now and then will depend on the path the Middle East conflict takes and what indicators and anecdotes continue to suggest about the impact of the conflict on New Zealand’s economic recovery and inflation.

In contrast to the period ahead of today’s meeting, there are many important domestic economic indicators scheduled for release ahead of the 2 September meeting. We think the following are the key ones to watch.

- Q2 CPI (21 July) and July Selected Prices (17 August): These pricing indicators will reveal whether the earlier surge in fuel prices has generated upward pressure across a broader range of goods and services.

- Q3 RBNZ surveys (13 August, 14 August, 21 August): Inflation expectations measures from the RBNZ’s surveys of professional forecasters, households and businesses will be analysed closely to see whether there has been a reversal of the energy-induced increase in inflation expectations observed in Q2.

- Q2 QSBO (14 July) and July/August ANZ Business Outlook (30 July/31 August): The data-rich QSBO survey was likely in the field before Middle East tensions eased so it will be interesting to see where the NZIER provide a breakdown of early and late responses. The ANZ surveys may provide a timelier account of how businesses are responding to the easing of the conflict and the resulting decline in oil prices.

- July/August PMI and PSI surveys (mid-July/mid-August): These may provide some early insight as to whether GDP growth has resumed in Q3.

- Q2 labour market surveys (5 August): Employment and hours worked data from the HLFS and QES surveys will cast light on the performance of the economy in Q2, while the LCI will cast light on underlying inflation pressures.

In addition to the above, we will monitor a range of other high-frequency indicators, such as monthly data on filled jobs, consumer spending, building consents, housing market activity and prices, job ads and consumer confidence. We will also be paying close attention to developments in prices for New Zealand’s key export commodities.

{kind=link}