- Geopolitics, Kevin Warsh and inflation data are likely to cause sharp fluctuations in the USD index.

- Gold is under pressure from real Treasury yields.

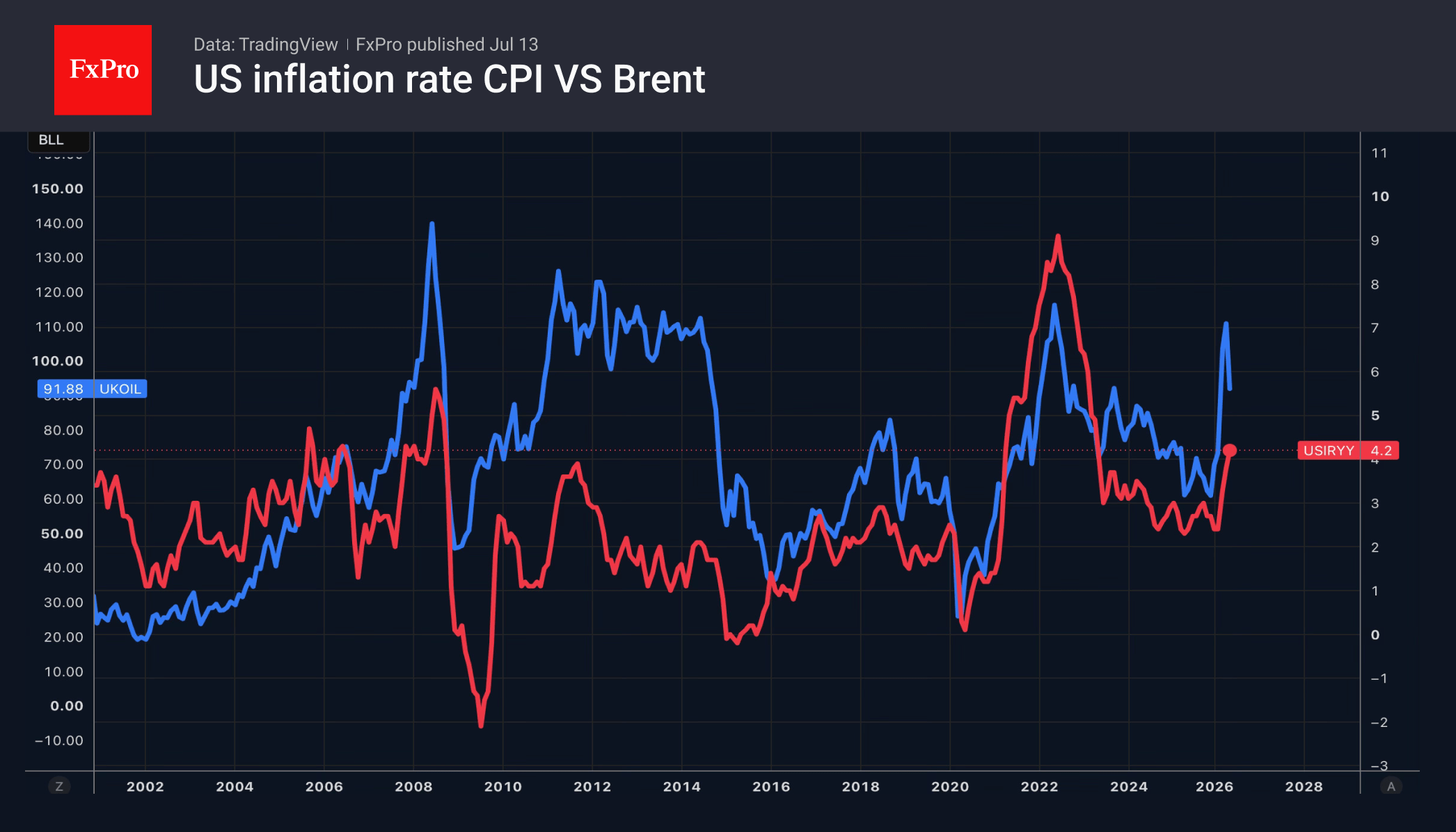

The US dollar began the week on an upward trend against the backdrop of escalating tensions in the Middle East. Donald Trump declared that the ceasefire is over, whilst Tehran denied the White House’s claims that it was seeking opportunities for negotiations. Confrontation is evident, and with it, the direct correlation between oil prices and the dollar is re-emerging.

Markets are factoring geopolitics into their expectations of potential Fed rate adjustments. Consequently, the probability of two rate rises in 2026 has risen from 36% to 50% over the past week.

However, investors’ attention is focused not only on geopolitics, but also on the release of US inflation figures for June and Kevin Warsh’s testimony before the US Congress. Warsh has twice caused turmoil in the financial markets. First, at his first FOMC meeting, he stated that the Fed intended to do everything in its power to bring consumer prices back to target, which caused the dollar to rise. Then, in Sintra, Portugal, the new Fed Chair’s comments on progress in the fight against inflation, by contrast, weakened the greenback.

Consumer prices are expected to fall by 0.1% month-on-month in June, marking the first decline since the pandemic and suggesting the indicator peaked in May. However, FOMC hawks may seize upon the acceleration in core inflation from 0.2% to 0.3% month-on-month. The market’s reaction will depend on the actual figures.

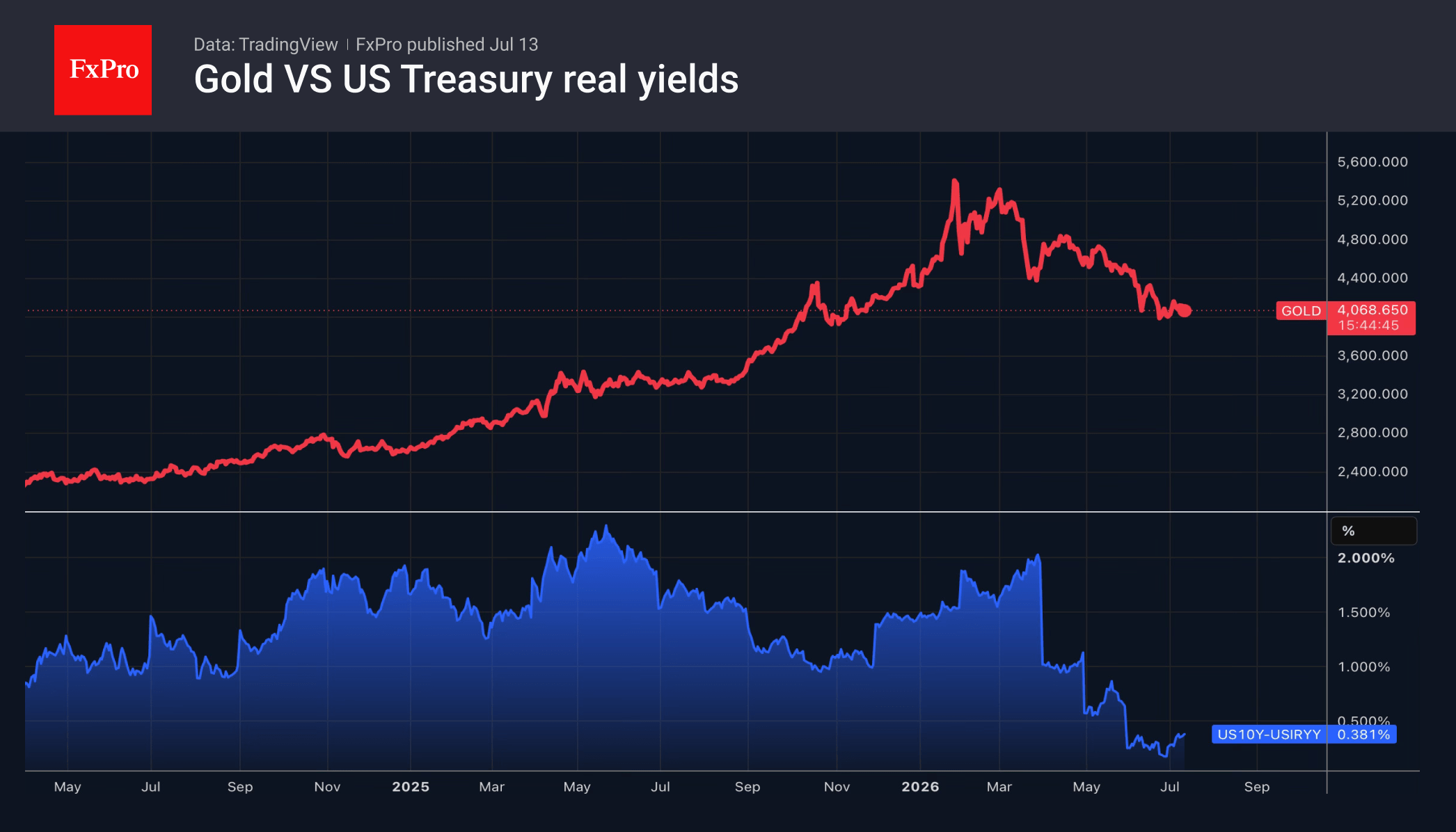

The escalation of the conflict in the Middle East has caused gold to retreat towards $4,000 per ounce. The precious metal is sensitive to movements in real Treasury bond yields, which for 10-year bonds have reached their highest level in over a year. This, combined with the strengthening of the US dollar and the increasing likelihood of aggressive monetary tightening by the Fed, is creating headwinds for gold.

The FxPro Analyst Team

{kind=link}