Sterling jumps broadly today as currency markets respond positive to UK Prime Minister Theresa May’s call for a snap election this June. GBP/USD powers through 1.2614 near term resistance and reaches as high as 1.2695 so far. GBP/JPY also took out 137.51 near term resistance which now suggests trend reversal. FTSE 100, however, is trading down -1.8% as stocks investments clearly dislike the uncertainties. Meanwhile, Euro also follows the Pound higher as markets are calm on French election. US Dollar, on the other hand, reversed earlier gains, against European majors but stays firm against commodity currencies.

UK PM May called snap elections

UK Prime Minister Theresa May surprised the world by calling for a snap election on June 8, "with reluctance", today. A election isn’t due until 2020. But opinion polls showed that May’s Conservative is having more than 20 points over Labour for the first time in nine years. The call for election is seen as an act to solidify public support for Brexit negotiation with EU. May emphasized that "we want a deep and special partnership between a strong and successful European Union and a United Kingdom that is free to chart its own way in the world." And, "our opponents believe that because the Government’s majority is so small, our resolve will weaken and that they can force us to change course. They are wrong."

US housing data missed

Released from US, housing starts dropped to 1.22m annualized rate in march, below expectation of 1.28m. Building permits rose to 1.26m annualized rate, meeting consensus. US Treasury Secretary Steven Mnuchin noted yesterday that "as the world’s currency, the primary reserve currency, I think that over long periods of time the strength of the dollar is a good thing." And, "it’s a function of the confidence and the strength of the US economy." Nonetheless, he still agreed with President Donald Trump’s comments regarding strength of the greenback in short term. Mnuchin said that "The president’s comment – which again I agree with – is that over short periods of time the strength of the dollar creates certain issues that hurt our exports. I think that is what he has referred to, which is again factually correct."

French election in focus

French presidential election will be a major focus in April and May. Recent surge in support for far-left Jean-Luc Melenchon is seen as making the election a four way match with far right Marine Le Pen, centrist Emmanuel Macron and conservative François Fillon. Some see increasing risk of having two euro-sceptic candidates, Le Pen and Melenchon, heading to the run-off in May. The markets responded by dumping French bonds and stocks. The five year French-German yield spread has indeed jumped to the highest level since 2013. However, it’s believed that support for Melenchon mainly came within the left-wing and is approaching limit. Thus, a run-off of Le Pen and Macron is still the base case. More in French Presidential Election: Macron and Le Pen Still Favorite as Melenchon Closing to Limit

Japan PM Abe nominated one dove, one centrist to replace two hawks in BoJ

In Japan, Prime Minister Shinzo Abe nominated two new members to replace Takehiro Sato and Takahide Kiuchi. Both are seen as hawks by the markets as they regularly dissented the ultra-loose monetary policies of the central bank. The two nominated are Goshi Kataoka, senior economist at Mitsubishi UFJ Research & Consulting, and Hitoshi Suzuki, an executive at the Bank of Tokyo-Mitsubishi UFJ. They are seen as one dove and one centrist. If the nominations are approved by the parliament, Abe would have then selected the entire BoJ policy board. And that would give him the advantage to continue with Abenomics.

BoJ Governor Haruhiko Kuroda said yesterday that consumer spending is picking up. And this is supported by steady improvements in employment and wages. And he noted that firms are likely to offer base-salary raise for staff during the current financial year. Separately, Deputy Governor Hiroshi Nakaso said that the central bank has been discussing the "means and how" of monetary stimulus exit" that could affect its revenues. But for now, BoJ’s priority is still on maintaining sustainable inflation through the massive stimulus program.

RBA April minutes less upbeat that the March one

RBA minutes for the April meeting came in less upbeat than the March one, underpinning concerns over developments in Australia’s labor and housing market. Policymakers refrained from delivering an upbeat forward guidance as it was in March. In the March minutes, RBA suggested that "year-ended growth was expected to pick up gradually to be above its potential rate over the forecast period". However, it only noted this month that "Australian economy had continued to grow moderately at the beginning of 2017, supported by the low level of interest rates". This apparently sounded less confident over the growth outlook. In the concluding statement, it was added that that "developments in the labour and housing markets warranted careful monitoring over coming months". More in RBA’s April Minutes Revealed Concerns Over Labor And Housing Markets.

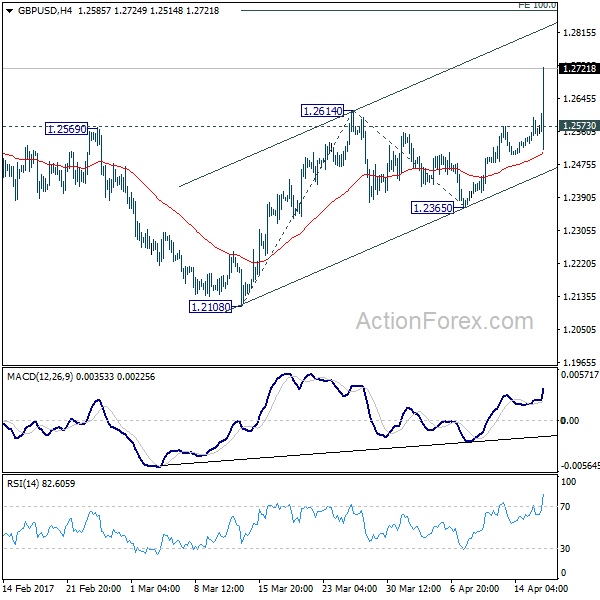

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2522; (P) 1.2558; (R1) 1.2599; More…

GBP/USD’s rally accelerates to as high as 1.2714 so far today. The strong break of 1.2614 resistance confirms resumption of rise from 1.2108. Intraday bias stays on the upside for 100% projection of 1.2108 to 1.2614 from 1.2365 at 1.2871. However, such rally is seen as part of the consolidation from 1.1946 low. Hence, we’d expect strong resistance around 55 week EMA (now at 1.3016) to limit upside and bring down trend resumption. On the downside, break of 1.2573 minor support will turn bias back to the downside for 1.2365 support first.

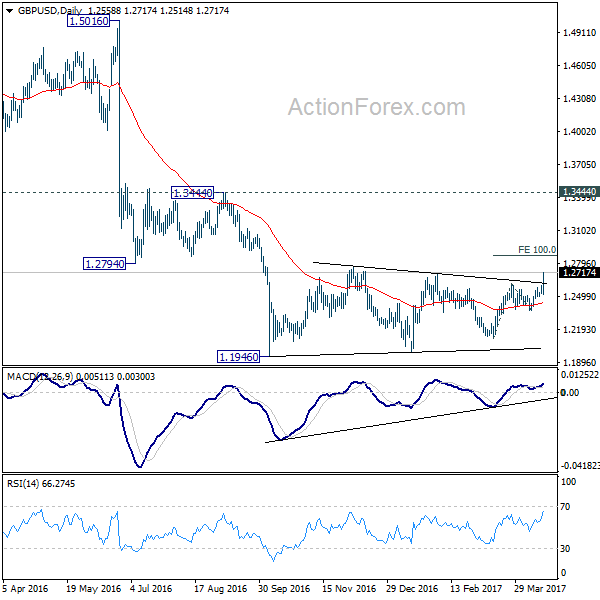

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | RBA Minutes Apr | ||||

| 12:30 | CAD | International Securities Transactions (CAD) Feb | 6.20b | |||

| 12:30 | USD | Housing Starts Mar | 1.22M | 1.28M | 1.29M | 1.30M |

| 12:30 | USD | Building Permits Mar | 1.26M | 1.26M | 1.21M | 1.22M |

| 13:15 | USD | Industrial Production Mar | 0.50% | 0.00% | ||

| 13:15 | USD | Capacity Utilization Mar | 76.00% | 75.40% |

{kind=link}