Dollar overtakes Yen as the strongest current for the week as buying merges today. Overnight’s rebound in treasury yield gives the greenback a helping hand. 10 year yield gained 0.035 to close the regular session at 2.928 and it breached 2.95 in Asia. Gold also extends recent slump on a strong Dollar and hits as low as 1265. Sterling and Swiss are are mixed as markets await BoE and SNB rate decisions. Kiwi is the weakest one as GDP report confirmed slow down while Australian Dollar is also weak. But Canadian Dollar is trying to recover, except versus Dollar, as WTI crude oil is back pressing 66.

Technically, GBP/USD’s fall resumes after brief consolidations and it’s now on course for next medium term fibonacci level at 1.2875. AUD/USD follows and breaks this week’s low at 0.7346 to resume recent decline. Focus will now be on 0.9989 temporary top in USD/CHF, and 1.1509 support in EUR/USD for today, to confirm Dollar’s broad based strength.

BoE and SNB to stand pat today

BoE and SNB meetings are the biggest focuses for today. BoE is widely expected to keep monetary policy unchanged. That is, the bank rate will be held at 0.50% while asset purchase target will be kept at GBP 435B. Known hawks Ian McCafferty and Michael Saunders are expected to vote for rate hike while others would vote for standing pat. The June meeting does not include updated economic projection nor a press conference. As such the meeting minutes would be in focus, serving as an indicator for the likelihood of an August rate hike. If hopes of an August rate hike falter, the chance of a November hike would be more remote. Hawkish Ian McCafferty is leaving the Committee and would be replaced by Jonathan Haskel, an Imperial College Business School professor. It remains to be seen how Haskel is. More in BOE Preview – Focus on June Meeting Minutes.

SNB is also widely expected to stand pat, keeping three-month Libor range between -1.25 and -0.25%. The central bank will also likely maintain the the commitment to intervene the FX market when needed, reiterating that it would ‘remain active in the foreign exchange market as necessary’, while ‘taking the overall currency situation into consideration’. EUR/CHF hit SNB’s prior imposed floor at 1.2 back in April. But political turmoil in Italy and fear of global trade war send the cross down to as low as 1.1366 back in late. With EUR/CHF currently at around 1.15, there is little chance for SNB to sound more relaxed.

Canadian Trudeau can’t accept why Trump damages his own auto industry

Canadian Prime Minister Justin Trudeau said yesterday that he couldn’t imagine Trump damaging the car industry of the US by imposing auto tariffs. He said, “I have a hard time accepting that any leader might do the kind of damage to his own auto industry that would happen if he were to bring in such a tariff on Canadian auto manufacturers, given the integration of the parts supply chains or the auto supply chains through the Canada-U.S. border.”

Trudeau tried to tone down Trump’s personal attack on him. He said that “I’m not in a position to opine on motivations of the president. I’m going to stay focused on the relationship that we’re building, on defending Canada’s interests, on looking for ways to further push the benefits of improving and modernizing NAFTA … in all three of our countries.”

Accord to a recent poll by Ipsos conducted between June 13-15, approval rating of Trudeau jumped to 50%, with 12% of Canadian strongly supporting him and 39% somewhat supporting. That’s a notable increase from the low of 44% at the end of March. That came after Trump’s personal attack on Trudeau saying that he acted so “meek and mild” during the G7 meeting. And, Trump’s trade advisor Peter Navarro said “there is a special place in hell” for Trudeau.

Chinese Vice Premier to meet European Commission Vice President Katainen next week on trade

Chinese Vice Premier Liu He will be meeting with European Commission Vice President Jyrki Katainen in Beijing on June 25. That’s the seventh China-EU high level economic and trade summit since 2007, when the mechanism was established.

Spokesman of the Ministry of Commerce said in a regular briefing that the meeting is an important platform for for communications and coordinations of economic and trade policies. And it’s an important time when “trade and economic cooperation faces new historical opportunities.”

Issues to be discussed will include ” global economic governance, trade and investment, innovation-driven development, and interconnection that are of common concern to both sides”. And, it’s a “positive signal between China and the EU to oppose unilateralism and protectionism and support the multilateral trading system.”

New Zealand GDP growth slowed to 0.5% qoq in Q1

New Zealand GDP grew 0.5% qoq in the March quarter, slowed from 0.6% qoq in the prior quarter and met expectation. Over the year, GDP grew 2.7% ended March 2018. Per capita GDP was unchanged, down from 0.1% qoq rise in the prior quarter. Services industries grew 0.6%, notably slowed from prior 1.1%. Good-producing industries were flat as jump in manufacturing was offset by fall in constructions. Primary industries rebounded by growing 0.6%, up from prior quarter’s -2.6%.

On the data front

Swiss will release trade balance today. UK will release public sector net borrowing. Canada will release wholesale sales. US will release jobless claims, Philly Fed survey, house price index and leading indicators.

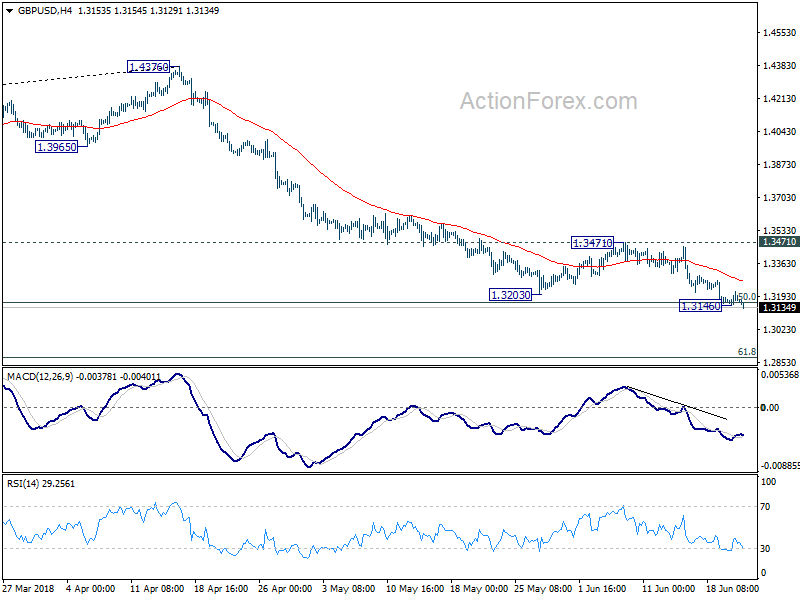

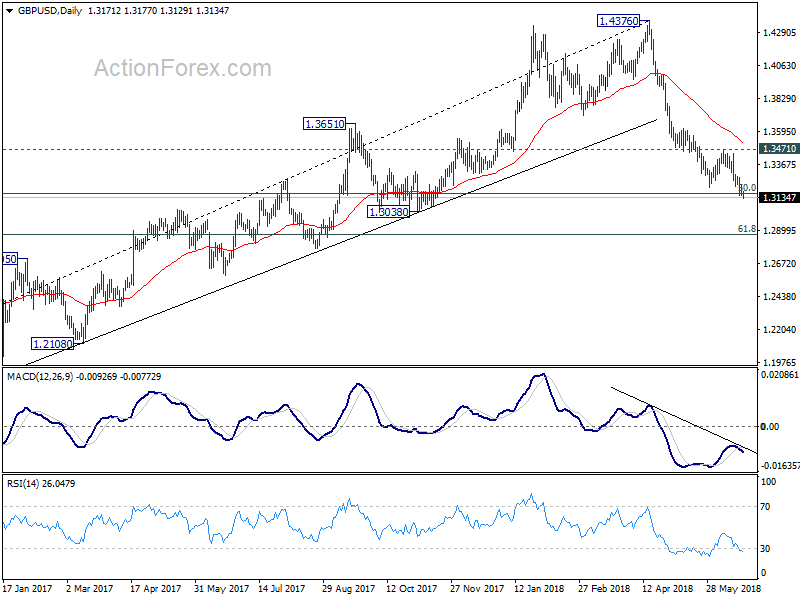

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3142; (P) 1.3179; (R1) 1.3211; More…

GBP/USD’s decline resumes after brief consolidation and reaches as low as 1.3129 so far. Intraday bias is back on the downside. Sustained trading below 50% retracement of 1.1946 to 1.4376 at 1.3161 will extend the fall from 1.4376 to 61.8% retracement at 1.2875 next. On the upside, break of 1.3471 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of another recovery.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4177). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We’ll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3527) holds, even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | GDP Q/Q Q1 | 0.50% | 0.50% | 0.60% | |

| 6:00 | CHF | Trade Balance (CHF) May | 2.76B | 1.89B | 2.29B | |

| 7:30 | CHF | SNB Sight Deposit Interest Rate | -0.75% | -0.75% | ||

| 7:30 | CHF | SNB 3-Month Libor Lower Target Range | -1.25% | -1.25% | ||

| 7:30 | CHF | SNB 3-Month Libor Upper Target Range | -0.25% | -0.25% | ||

| 8:30 | GBP | Public Sector Net Borrowing May | 5.1B | 6.2B | ||

| 11:00 | GBP | BoE Official Bank Rate | 0.50% | 0.50% | ||

| 11:00 | GBP | BoE Asset Purchase Target Jun | 435B | 435B | ||

| 11:00 | GBP | MPC Official Bank Rate Votes | 2–0–7 | 2–0–7 | ||

| 11:00 | GBP | MPC Asset Purchase Facility Votes | 0–0–9 | 0–0–9 | ||

| 12:30 | CAD | Wholesale Sales M/M Apr | 0.50% | 1.10% | ||

| 12:30 | USD | Initial Jobless Claims (JUN 16) | 220K | 218K | ||

| 12:30 | USD | Philly Fed Manufacturing Index Jun | 25 | 34.4 | ||

| 13:00 | USD | House Price Index M/M Apr | 0.30% | 0.10% | ||

| 14:00 | USD | Leading Index May | 0.40% | 0.40% | ||

| 14:00 | EUR | Eurozone Consumer Confidence (JUN A) | 0 | 0 | ||

| 14:30 | USD | Natural Gas Storage | 96B |

{kind=link}