Yen trades broadly higher today, followed by Dollar and Swiss Franc as sentiments are weighed down by escalating trade rhetorics. Nikkei closed down by -0.79% at 22339.15, after hitting session low at 22312.79. China’s Shanghai composite opened higher, as lifted by PBoC’s RRR cut, but turned red soon after. Commodity currencies are trading as the weakest ones in risk aversion environment as usual, with Aussie leading the way down.

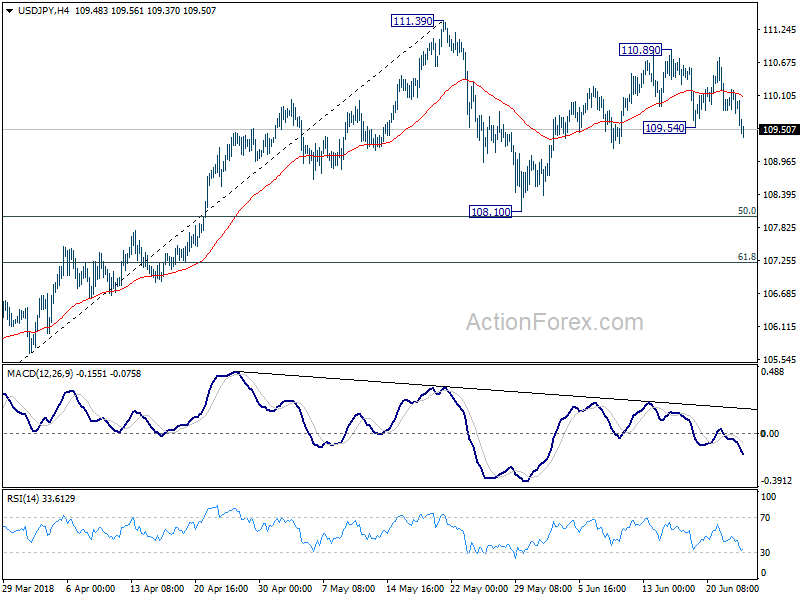

Technically, USD/JPY’s break of 109.54 reaffirm the case that near term rebound from 108.10 has completed at 110.89 already. And recent consolidation pattern from 111.39 is starting the third leg for 108.10 and below. EUR/JPY and GBP/JPY both staged slightly stronger than expected rebound last week. But with today’s selloff, focuses are back on recent support at 126.62 and 144.37 respectively.

Trump escalates trade war threats to the world

Concerns of global trade war is a factor driving stocks down. Trump stepped up his rhetoric as he is now pushing all countries to remove “artificial trade barriers and tariffs”. Or, he warned of “more than reciprocity by the USA”. He tweeted that “The United States is insisting that all countries that have placed artificial Trade Barriers and Tariffs on goods going into their country, remove those Barriers & Tariffs or be met with more than Reciprocity by the U.S.A. Trade must be fair and no longer a one way street!”

This was a follow up to his warning to EU on Friday that 20% tariffs could be imposed to their cars. That’s a response to EU’s retaliation to US steel and aluminum tariffs. He tweeted “Based on the Tariffs and Trade Barriers long placed on the U.S. & its great companies and workers by the European Union, if these Tariffs and Barriers are not soon broken down and removed, we will be placing a 20% Tariff on all of their cars coming into the U.S. Build them here!”

European Commission Vice President Jyrki Katainen told French newspaper Le Monde that “if they decide to raise their import tariffs, we’ll have no choice, again, but to react. And, he added that “We don’t want to fight (over trade) in public via Twitter. We should end the escalation.”

BoJ: Inappropriate to adopt policy that forcibly push up demand in a short time

In the summary of opinions at the June 14/15 BoJ monetary policy meeting, the central noted that the economy is “expanding moderately”. But it also cautioned that the effect of US “protectionist trade policy” warrant “close attention”. In addition to that, other concerns include “political situation in southern Europe and volatile movements in some emerging markets. Though, the latter have “limited” effects on the global economy at this point.

Regarding inflation, BoJ noted that “upward pressure on wages has been weak despite the increased tightness in the labor market”. And, “if wages do not rise in line with inflation, this would pose a burden on people.” BoJ said “close attention should be paid to developments in labor productivity and real wages, while taking into account mainly the effects of a reduction in overtime work hours under working-style reforms.”

On monetary policy, since there is “still a long way” to meet 2% inflation target, it is “appropriate to pursue powerful monetary easing with persistence under the current guideline”. But BoJ also noted that “the reason for the sluggishness in prices is unlikely to be merely a shortage of demand”. Therefore, “it is not appropriate to adopt a policy that would forcibly push up demand in a short period of time.

PBoC cuts RRR by 50bps to release CNY 700B in funds

China’s central bank, PBoC, announced to lower some banks’ reserve requirement ratios by 50 bps, effective July 5. The targeted banks include large state-owned commercial banks, joint-stock commercial banks, postal savings banks, urban commercial banks, non-county rural commercial banks and foreign banks.

PBoC also encourages the five state-owned large-scale commercial banks and 12 joint-stock commercial banks to use directional RRR cuts and funds raised from the market to implement the “debt-to-equity swap” project.

It’s estimated that the RRR cut will release around CNY 700B in funds that could help ease credit strain for small and micro businesses.

BIS: Protectionism, snapback in yields, politics in Euro area are possible triggers of downturn

The Bank for International Settlements warned in its annual report that escalation of protectionist measures is one possible trigger of global economic slowdown or downturn. It said that “its impact could be very significant, if such escalation was seen as threatening the open multilateral trading system.” And, there are already signs that the these measures and the “ratcheting-up of rhetoric” are “inhibiting investment”. And, trade negotiations would “become more complicated” with recent reversal US Dollar depreciation.

Sudden “decompression” of historically low bond yields, or “snapback” in core sovereign market yields could be another trigger. And, Biassed it could take place “in response to an inflation surprise” and “the perception that central banks will have to tighten more than anticipated. In the US, “the prospective heavy issuance of government debt, combined with the gradual unwinding of central bank purchases, could add to this risk.” BIS also noted that the surprise “need not be a large one”, yet the impact could spread globally.

General reversal in risk appetite is a third possible trigger. And, such reversal could reflect a range of factors, including disappointing profits, the drag of the contraction phase of financial cycles where these have turned, a souring of sentiment vis-à-vis EMEs, or untoward political events threatening stability in some large economies. BIS added that from this perspective, “recent events in the euro area are a source of concern.”

Looking ahead

RBNZ is the main central bank event this week and it’s widely expected to stand pat again. Other than that, there are quite a number of economic data to watch. German Ifo business climate and Eurozone CPI flash are important for the Euro. US durable goods, trade balance will be watched too but the impacts on markets may not be long lasting. Canada GDP is another key event that could finally remove the already slim chance of a July BoC hike. Here are some highlights for the week:

- Monday: German Ifo; US new home sales

- Tuesday: Japan CSPI; UK BBA mortgage approvals, CBI realized sales; US S&P Case-Shilller house price, consumer confidence

- Wednesday: New Zealand trade balance, business confidence; Eurozone M3; US durable goods, trade balance, wholesale inventories, pending home sales

- Thursday: RBNZ rate decision; Japan retail sales; German CPI flash; US Q1GDP final, jobless claims

- Friday: New Zealand building permits; Japan Tokyo CPI, unemployment rate, industrial production, housing starts, consumer confidence; German retail sales, import prices, unemployment; Swiss KOF; UK Q1 GDP final, M3, mortgage approvals; Eurozone CPI flash; Canada GDP, IPPI and RMPI; US personal income and spending, Chicago PMI

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.79; (P) 110.00; (R1) 110.21; More…

USD/JPY’s break of 109.54 suggests that fall from 110.89 has resumed. Such decline is seen as the third leg of the consolidation pattern from 111.39. Intraday bias is back on the downside for 108.10 support and possibly below. But, we’d expect strong support from 61.8% retracement of 104.62 to 111.39 at 107.20 to contain downside and bring rebound. On the upside, above 110.89 will extend the rise from 108.10 towards 111.39 instead.

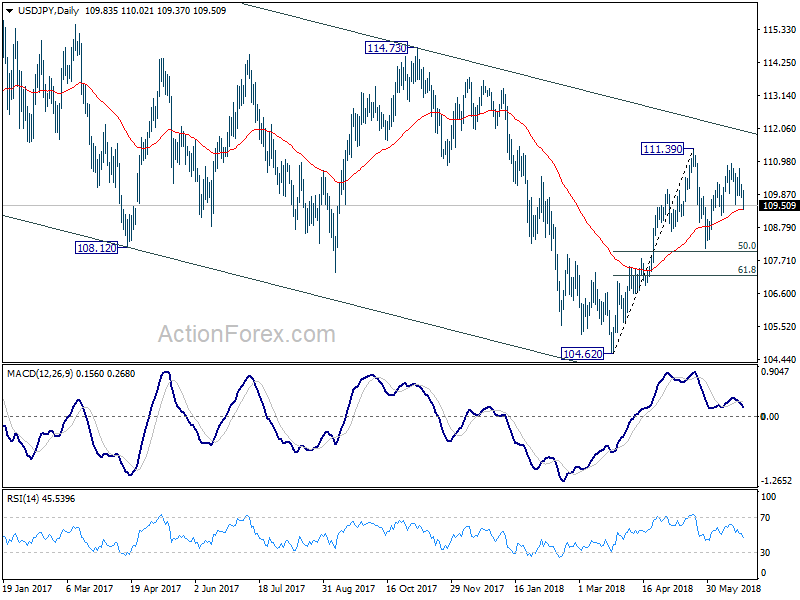

In the bigger picture, at this point, we’re slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BOJ Summary of Opinions | ||||

| 08:00 | EUR | German IFO Business Climate Jun | 101.7 | 102.2 | ||

| 08:00 | EUR | German IFO Expectations Jun | 98 | 98.5 | ||

| 08:00 | EUR | German IFO Current Assessment Jun | 105.6 | 106 | ||

| 14:00 | USD | New Home Sales May | 665K | 662K |

{kind=link}