Yen remains the strongest one for the day, as risk aversion dominates. Commodity currencies, Australia, New Zealand and Canadian Dollar remain the weakest. But some additional strength is seen in Euro as German Ifo business confidence came is not too badly. At the time of writing, FTSE and DAX are trading down -1.3% as initial selloff accelerates. CAC is the relatively resilient and is down -0.8% only. US futures point to another day of loss as DOW might open three-digits lower.

Trade tensions are the key concerns of investors for the moment. The EU’s retaliations on US steel and aluminum tariffs were effective last Friday. Trump quickly responded by threatening to impose 20% tariffs on EU cars. And he warned of “more than reciprocity” actions if others don’t put down their trade Barriers and tariffs. Yet, at the same time, he is building up barriers for even the closest trade and security allies of the US.

There are more retaliations to the US steel tariffs coming up. Canada’s will be effective on July, and Mexico’s on July 5. At the same time, the section 301 tariffs on China will come effective on July 6, with China’s retaliation on the same day. And, upcoming will be tariffs on the second list of Chinese imports. Furthermore, there will be target everyone auto tariffs. It’s just the start of the beginning.

German Ifo dropped to 101.8, fell markedly in trade

German Ifo business climate dropped to 101.8 in June, down from 102.3, slightly higher than expectation of 101.7. Current assessment dropped to 105.1, down from 106.1 and missed expectation of 105.6. Expectations gauge was unchanged at 98.6, meeting consensus.

Ifo President Clemens Fuest noted in the release that companies were less satisfied with their current business situation while business expectations remained slightly optimistic. Nonetheless, “the tailwind enjoyed by the German economy is calming down.”

He also pointed out that the index “fell markedly in trade”. “Companies downwardly revised their very good assessments of the current business situation. Their business outlook turned slightly pessimistic for the first time since February 2015. Indicators dropped far more sharply in retailing than in wholesaling.”

China and EU agreed to oppose unilateralism and trade protectionism

Chinese Vice Premier Liu He met with European Commission Vice President Jyrki Katainen in Beijing today. After the meeting, Liu said in a media briefing that “both sides believe that we must resolutely oppose unilateralism and trade protectionism and prevent such behavior from causing volatility and recession in the global economy.” Additionally, both sides will prepare lists of proposals for bilateral investment agreement at another China-EU summit next month.

Katainen, on the other hand, emphasized there some areas must be addressed to take the economic, trade and investment relationship further. For example, he said “it is essential that we work together to tackle overcapacity in sectors such as steel and aluminum.” And he urged China to avoid overcapacity in other sectors too, including those targeted by the “Made in China 2025” initiative.

PBOC Cut RRR, Injecting Most Liquidity to Market So Far This Year

Yesterday, PBOC announced a -50 bps reduction in reserve requirement ratio (RRR) for commercial banks. The move, effective from July 5, aims at easing the tightening in credit condition with the injection of about RMB 700B of liquidity to the market. The decision came in line with our assessment that China, struggling with growth moderation and intensification of trade conflict with the US, would have to adopt a more accommodative policy, with RRR cut a usual tool adopted by the Chinese government.

Fed’s gradual rate hike, ECB’s completion of QE later in the year and a more hawkish BOE have contributed to a less easy global monetary environment. While this, together with the elevated debt environment (the need to deleverage) in China, suggests the Chinese government might actually need to adopt a less accommodative policy, the rapid deterioration in economic activities in April and May is alarming and has forced the government shift its focus from deleveraging to growth stability.

We expect this dilemma would continue to haunt the government in coming years. A mishandling not only would cause disaster in the world’s second largest economy, but also the world.

More in PBOC Cut RRR, Injecting Most Liquidity to Market So Far This Year

BoJ: Inappropriate to adopt policy that forcibly push up demand in a short time

In the summary of opinions at the June 14/15 BoJ monetary policy meeting, the central noted that the economy is “expanding moderately”. But it also cautioned that the effect of US “protectionist trade policy” warrant “close attention”. In addition to that, other concerns include “political situation in southern Europe and volatile movements in some emerging markets. Though, the latter have “limited” effects on the global economy at this point.

Regarding inflation, BoJ noted that “upward pressure on wages has been weak despite the increased tightness in the labor market”. And, “if wages do not rise in line with inflation, this would pose a burden on people.” BoJ said “close attention should be paid to developments in labor productivity and real wages, while taking into account mainly the effects of a reduction in overtime work hours under working-style reforms.”

On monetary policy, since there is “still a long way” to meet 2% inflation target, it is “appropriate to pursue powerful monetary easing with persistence under the current guideline”. But BoJ also noted that “the reason for the sluggishness in prices is unlikely to be merely a shortage of demand”. Therefore, “it is not appropriate to adopt a policy that would forcibly push up demand in a short period of time.

BIS: Protectionism, snapback in yields, politics in Euro area are possible triggers of downturn

The Bank for International Settlements warned in its annual report that escalation of protectionist measures is one possible trigger of global economic slowdown or downturn. It said that “its impact could be very significant, if such escalation was seen as threatening the open multilateral trading system.” And, there are already signs that the these measures and the “ratcheting-up of rhetoric” are “inhibiting investment”. And, trade negotiations would “become more complicated” with recent reversal US Dollar depreciation.

Sudden “decompression” of historically low bond yields, or “snapback” in core sovereign market yields could be another trigger. And, Biassed it could take place “in response to an inflation surprise” and “the perception that central banks will have to tighten more than anticipated. In the US, “the prospective heavy issuance of government debt, combined with the gradual unwinding of central bank purchases, could add to this risk.” BIS also noted that the surprise “need not be a large one”, yet the impact could spread globally.

General reversal in risk appetite is a third possible trigger. And, such reversal could reflect a range of factors, including disappointing profits, the drag of the contraction phase of financial cycles where these have turned, a souring of sentiment vis-à-vis EMEs, or untoward political events threatening stability in some large economies. BIS added that from this perspective, “recent events in the euro area are a source of concern.”

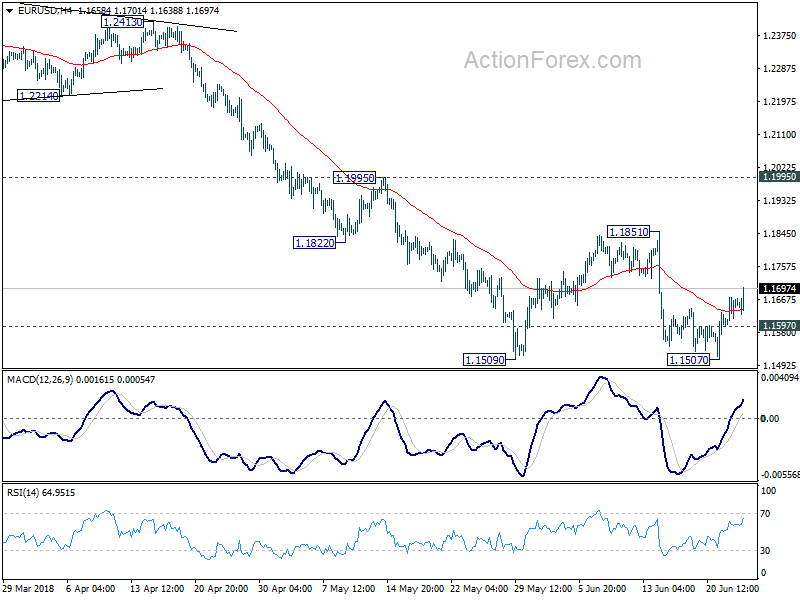

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1614; (P) 1.1645 (R1) 1.1690; More…..

EUR/USD’s rebound from 1.1507 is in progress and further rise could be seen. But it’s after all, seen as part of the consolidation from1.1509. Upside should be limited by 1.1851 resistance to bring fall resumption. On the downside, below 1.1597 minor support will bring retest of 1.1507 first. Break will resume the whole fall from 1.2555 through 50% retracement of 1.0339 to 1.2555 at 1.1447 to 61.8% retracement at 1.1186.

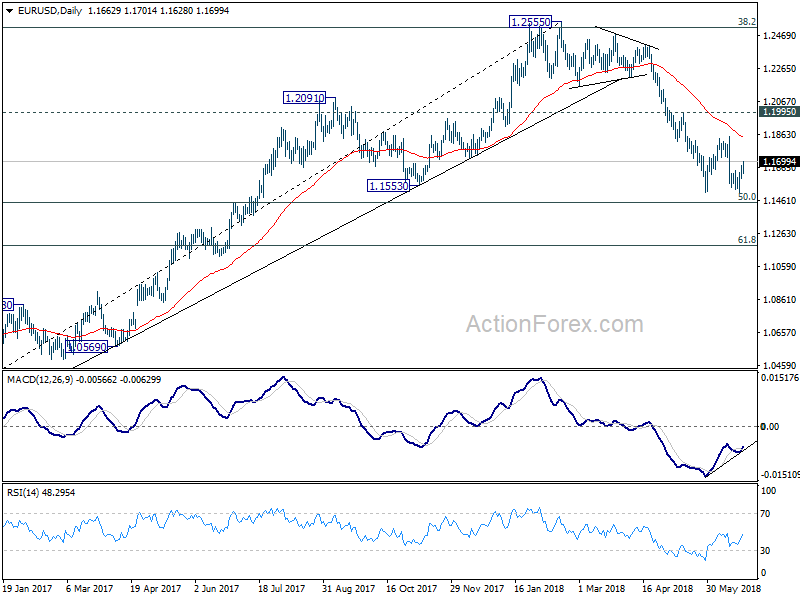

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won’t consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BOJ Summary of Opinions | ||||

| 8:00 | EUR | German IFO Business Climate Jun | 101.8 | 101.7 | 102.2 | 102.3 |

| 8:00 | EUR | German IFO Expectations Jun | 98.6 | 98 | 98.5 | 98.6 |

| 8:00 | EUR | German IFO Current Assessment Jun | 105.1 | 105.6 | 106 | 106.1 |

| 14:00 | USD | New Home Sales May | 665K | 662K |

{kind=link}