Early rebound in US stocks overnight initially supported Dollar. But the greenback couldn’t hold on to the gains as stocks suffered steep reversal. Fed’s rate hike was not the reason for the selloff. Instead, the trigger of the late selloff in US equities was threat of Trump’s escalation of US-China trade war. In particular, NASDAQ suffered worst single day reversal in three years. Though, Asian markets stabilized after Trump tried to tone down a bit in a TV interview. But sentiments would remain vulnerable due to erratic nature of Trump.

In the currency market, Yen is currently the weakest one for today, followed by Dollar and then Swiss Franc. Australian Dollar leads commodity currencies higher. Eurozone and Sterling are mixed. Technically, for now, EUR/USD and GBP/USD are held well below 1.1493 and 1.2919 minor resistance levels, hence, near term outlook stays bearish. Though, in case of further declines, we’d be cautious on bottoming at around 1.1300 1.2661 lows respectively.

In other markets, Asian stocks are mostly in black for now. Nikkei is up 1.57%, Hong Kong HSI is up 0.30%, China Shanghai SSE is up 1.70%. But Singapore Strait Times is down -0.38%. Overnight, DOW lost -0.99%, S&P 500 down -0.66% and NASDAQ down -1.63%. 10 year yield rose 0.010 to 3.087 but was way off day high at 3.117.

DOW suffered bearish U-turn on new threat of Trump’s China tariffs, but Asia recovered

US stocks suffered heavy selloff towards the end of the session overnight, single handedly knocked down by Trump’s trade policy. DOW rebounded in early trading to as high as 25040.58 but closed down -0.99% or -245.39 pts at 24442.92. That’s the biggest U-turn in eight months. S&P 500 hit 2706.85 before closing down -0.66% at 2641.25. NASDAQ jumped to 7296.51 and close down -1.63% or -116.92 pts at 7050.29. The U-turn in NASDAQ was the worst in three years.

Selloff emerged as Bloomberg reported that Trump is going to impose additional tariffs on all Chinese imports, should the summit with Chinese President Xi Jinping fail. The two leaders plan to meet at sideline of G20 summit in Buenos Aires in November, but even this arrangement is not finalized yet. The announcement of the new tariffs could come in as early as December. The total amount of imports to be tariffs could add up to USD 257B, in addition to the USD 250B already covered by current tariffs.

White House Press Secretary Sarah Huckabee Sanders declined talked about the specifics of the Xi-Trump meeting. She just said “You have two of the most powerful leaders in the world. I think that’s consequential no matter how you look at it and we’ll see what happens when they sit down.”

In Asia, though, Chinese and Hong Kong stocks reversed early losses after Trump’s comment in an interview with Fox news. He said, “I think we will make a great deal with China, and it has to be great because they’ve drained our country.”

Separately, according to Gallup polling during the week ended October 28, Trump’s job approval rating dropped steeply by 4% to 40%, sharpest decline since June 24, on the controversy over his policy of separating families apprehended illegally crossing the US-Mexico border. On the other hand, his disapproval rating rose to 54%.

UK Hammond: It’s double dividend if Brexit negotiation turns out right

Yesterday in his budget speech, UK Chancellor of Exchequer Philip Hammond raised the total funding for Brexit preparation to GBP 4B. He also noted that budget deficit has fallen to less that 1.5% this year. And it’s projected to fall further to 0.8% by 2023-24.

Hammond emphasized that it’s a “pivotal moment” in Brexit negotiations. If things turn out right, it will be “double Brexit dividend”. Firstly, investments current on hold will come on stream. Secondly, Treasury will no longer have to hold back money for preparations.

On the economy, he raised growth forecasts for 2019 and 2020. For 2021 and 2022, growth projections are kept unchanged. But growth is expected to pickup again in 2023.

Here is a quick summary on GDP growth projections:

- 2019: 1.6%, up from 1.3% in the spring statement

- 2020: 1.4%, up from 1.3% in the spring statement

- 2021: 1.4%, unchanged from 1.4% in the spring statement

- 2022: 1.5%, unchanged from 1.5% in the spring statement

- 2023: 1.6% (new forecast)

Japan unemployment rate dropped to 2.3%, BoJ meeting starts

Japan’s unemployment rate dropped for the second month by -0.1% to 2.3% in September, better than expectation of 2.4%. That’s also just 0.1% above May’s low at 2.2%. Unemployment rate has been in steady decline in recent years.

BoJ monetary policy meeting starts today. It’s widely expected that the central bank will stand pat in the announcement tomorrow. Interest rate will be held unchanged at -0.1%. A major focus is the new economic forecasts but a majority of economists expect them to be largely unchanged.

A major change in BoJ’s communications this year was the explicit allowance of 10 year JGB yield to move in a range of -0.1% to 0.1%. And, JGB is has already moved more than that. Hence, there is possibly unnecessary for BoJ to widen that band further.

Also release in Asian session, Australia building approvals rose 3.3% mom in September, below expectation of 3.9% mom.

Elsewhere

Eurozone data will catch a lot of attention today. Eurozone, Fran and Italy will release Q3 GDP. Germany will Eurozone unemployment and CPI flash. Eurozone will also release confidence indicators.

Later in the day, US S&P Case-Shillar house price and Conference Board consumer confidence will be featured.

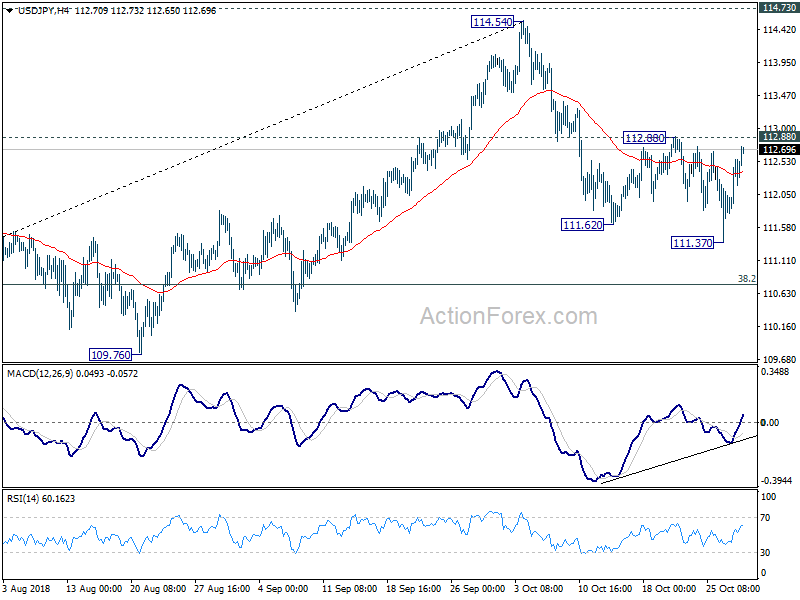

USD/JPY Daily Outlook

Daily Pivots: (S1) 111.92; (P) 112.24; (R1) 112.70; More..

USD/JPY’s rebound from 111.37 extends today but stays below 112.88 resistance. Intraday bias remains neutral first. Another fall cannot be ruled out yet. On the downside, break of 111.37 will extend the fall from 114.54 to 38.2% retracement of 104.62 to 114.54 at 110.75. As such fall is seen as part of medium term correction, we’ll look for bottoming signal above 109.76 key support. On the upside, break of 112.88 resistance will suggest that the fall has completed and turn bias back to the upside for retesting 114.54.

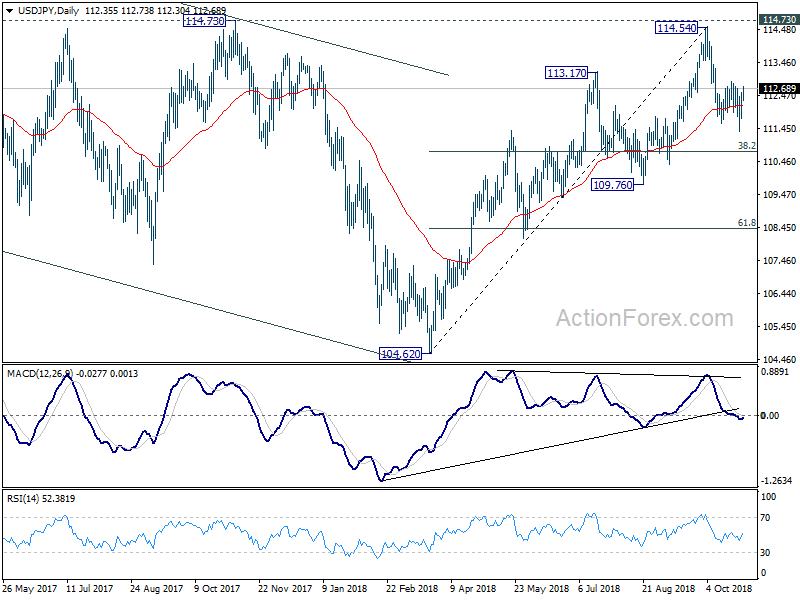

In the bigger picture, corrective fall from 118.65 (2016 high) should have completed with three waves down to 104.62. Decisive break of 114.73 resistance will likely resume whole rally from 98.97 (2016 low) to 100% projection of 98.97 to 118.65 from 104.62 at 124.30, which is reasonably close to 125.85 (2015 high). This will stay as the preferred case as long as 109.76 support holds. However, decisive break of 109.76 will dampen this bullish view and turns outlook mixed again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Jobless Rate Sep | 2.30% | 2.40% | 2.40% | |

| 0:30 | AUD | Building Approvals M/M Sep | 3.30% | 3.90% | -9.40% | -8.10% |

| 6:30 | EUR | French GDP Q/Q Q3 A | 0.40% | 0.20% | ||

| 8:00 | CHF | KOF Leading Indicator Oct | 100.8 | 102.2 | ||

| 8:55 | EUR | German Unemployment Change Oct | -12K | -23K | ||

| 8:55 | EUR | German Unemployment Claims Rate Oct | 5.10% | 5.10% | ||

| 9:00 | EUR | Italian GDP Q/Q Q3 P | 0.20% | 0.20% | ||

| 10:00 | EUR | Eurozone Business Climate Indicator Oct | 1.15 | 1.21 | ||

| 10:00 | EUR | Eurozone Economic Confidence Oct | 110 | 110.9 | ||

| 10:00 | EUR | Eurozone Industrial Confidence Oct | 3.9 | 4.7 | ||

| 10:00 | EUR | Eurozone Services Confidence Oct | 14 | 14.6 | ||

| 10:00 | EUR | Eurozone Consumer Confidence Oct F | -2.7 | -2.7 | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q3 A | 0.40% | 0.40% | ||

| 10:00 | EUR | Eurozone GDP Y/Y Q3 A | 1.90% | 2.10% | ||

| 13:00 | EUR | German CPI M/M Oct P | 0.10% | 0.40% | ||

| 13:00 | EUR | German CPI Y/Y Oct P | 2.40% | 2.30% | ||

| 13:00 | USD | S&P/Case-Shiller Composite-20 Y/Y Aug | 5.80% | 5.90% | ||

| 14:00 | USD | Consumer Confidence Index Oct | 135 | 138.4 |

{kind=link}