Risk sentiments are rather firm in Asian markets as major indices opened up and are extending gains. UK Prime Minister Theresa May’s survival of the leadership challenge is a positive factor. Also, progress and US-China trade talk is another factor. It’s reported that China has already purchased more than 1.5m tonnes of US soybeans this week, the first major purchase in six months. And of course there were reports that China is considering to lower auto tariffs from 40% to 15%. The WSJ also reported that China is working on replacing the “Made in China 2025” initiative with something that allows more foreign participations. Focus will now turn to SNB and then ECB rate decision.

In the currency markets, Australian Dollar is so far the strongest one for today, followed by Dollar and then Euro. Yen is trading as the weakest one. Sterling follow as the second weakest as yesterday’s rebound fades. For the week, Aussie is the strongest one followed by Dollar. But with the exception of GBP/USD, all Dollar and Aussie pairs are limited below last week’s high, suggesting lack of follow through momentum. Sterling remains the worst performing one followed by Yen.

In other markets, DOW closed up 0.64% overnight. S&P 500 rose 0.54% and NASDAQ added 0.95%. 10 year yield rose 0.027 to 2.906. 3-year (2.783) to 5-year (2771) yield remains inverted. In Asia, at the time of writing, Nikkei is up 0.99%, Hong Kong HSI up 1.33%, China Shanghai SSE up 1.60%, Singapore Strait Times up 0.46%. Japan 10 year JGB yield is up 0.0066 to 0.064. USD/CNH dropped sharply yesterday and it’s now at 6.870, comparing to this week’s high at 6.922.

ECB to revise down growth and inflation forecasts, SNB to stay cautious

ECB is widely expected to keep benchmark interest rate unchanged at 0.00% today. And it should stick with the plan to end the asset purchase program after December. Nevertheless, there are prospects of some dovish shifts. As indicated by recent economic data, growth momentum in the Eurozone, in particular in Germany, has slowed down quite notably. Recent slump in oil prices would also put some downward pressure in the energy led headline inflation in the bloc. ECB is generally expected to revise down 2019 growth and inflation forecasts.

President Mario Draghi’s comments on the economy will also be watched. ECB has so far viewed the slowdown in second half as temporary. But policy makers could start to feel more uncertainty about that. In particular, the slowdown in global trade due to protectionism is starting to bite exports growth, most notably in Germany. But for now, we’re not expecting ECB to change the forward guidance of keeping interest rates at present level at least through summer of 2019. The forward guidance itself is flexible enough.

SNB is also widely expected to keep the Sight Deposit rate unchanged at -0.75%, with 3-month Libor target range held at -1.25 to -0.25%. Some traders might look for hints of a rate hike in 2019. But it’s rather unlikely. EUR/CHF ‘s uptrend topped at 1.2004 back in April, rejected by the key 1.2 handle. Subsequent events, including Iran sanctions, Italian elections and budget, Turkish Lira crisis, trade war, stock markets rout, etc, sent the cross back to below 1.15. Meanwhile, domestically, Swiss economy also contracted -0.2% in Q3. There is little room for SNB policy makers to move away from negative interest rate.

Some suggested readings on ECB and SNB

- ECB Preview: Dovish Surprise Possible, But Draghi Likely To Leave His Options Open

- Will Europe’s Slowdown Restrain the ECB?

- ECB to End QE But Support Still Needed

- ECB: A Matter Of Less Accommodation, Not Tightening

- ECB Preview: A New Chapter Of Dovish Tightening

- ECB Preview – Focus on Reinvestment Plan, New Round of TLTRO

- SNB Meeting: No Hawkish Bits Yet

Sterling rebound lost steam after UK PM May survived leadership challenge

Sterling softens mildly in Asia after UK Prime Minister Theresa May survived the leadership challenge. 200 Conservative MPs voted in support for May in the no-confidence vote. 117 voted against her. That’s way more than enough to secure her place as Prime Minister. But it’s still alarming than more than a third of the MPs of her party wanted her out. May herself also admitted that “a significant number of colleagues did cast a vote against me and I’ve listened to what they said”. But she added it’s time to “get on with the job of delivering Brexit for the British people”.

May will go to Brussels for the two day EU summit today. But she’s only given 10 mins to tell EU leaders what she needs to get the Brexit agreement through parliament. EU’s stance is very clear that the agreement itself is not renegotiable. But they’re open to offer “assurances” regarding the Irish border backstop, and others. The results of the summit could continue to trigger volatility in the pound.

Canada warns US not to politicize extradition, China urges Canada to distance from US hegemonism

Canadian Foreign Minister Chrystia Freeland warned the US (not China) not to politicize the arrest and extradition of Huawei top executive Meng Wanzhou. Trump said on Tuesday that he could intervene in the case if it’s good for trade negotiation with China. When asked about Trump’s comments, Freeland said “our extradition partners should not seek to politicize the extradition process or use it for ends other than the pursuit of justice and following the rule of law”.

Separately, Chinese state-owned hawkish media Global Times urged Canada to “distance itself from US hegemonism and fulfill its obligations to help maintain international order and protect human rights”. And the media also warned that “Washington is mistaken if it thinks it can take Meng hostage and ransom her for concessions in the upcoming trade talks.”

On the data front

Australian consumer inflation expectation rose to 4.0% in December. UK RICS house price balance dropped to -11 in November. Germany will release CPI final while Swiss will release PPI in European session. US will release import price index and jobless claims later in the day. But main focuses will be on SNB, ECB and May’s Brussel trip.

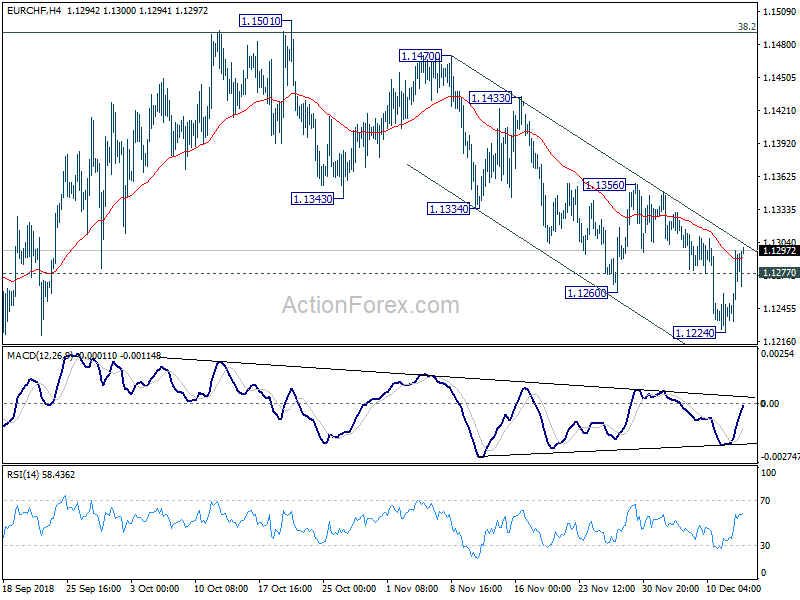

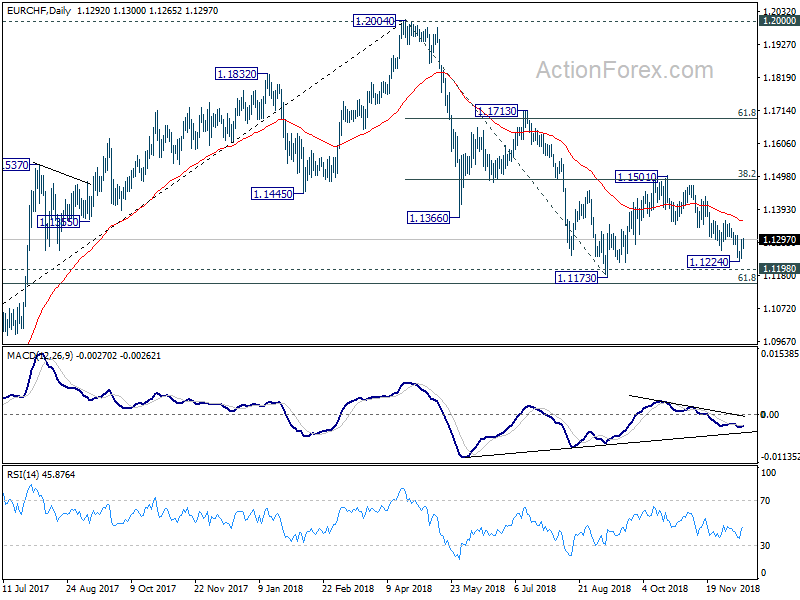

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1253; (P) 1.1276; (R1) 1.1316; More…

Considering bullish convergence condition in 4 hour MACD, EUR/CHF’s rebound and break of 1.1277 minor resistance suggests short term bottoming at 1.1224. Intraday bias is turned back to the upside for 1.1356 resistance first. Decisive break there should indicate near term reversal and target 1.1501 key resistance. On the downside, below 1.1224 will dampen this bullish case and extend the fall to 1.1173 low instead. But still, we’d expect strong support inside 1.1154/98 key support zone to bring reversal.

In the bigger picture, price actions from 1.2004 medium term top is seen as a correction only. Downside should be contained by support zone of 1.1198 (2016 high) and 61.8% retracement of 1.0629 to 1.2004 at 1.1154 to complete it and bring rebound. A break of 1.2 key resistance is still expected in the medium term long term. However, sustained break of the mentioned support zone will mark reversal of the long term trend. In that case, 1.0629 key support will be back into focus.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectation Dec | 4.00% | 3.60% | ||

| 00:01 | GBP | RICS House Price Balance Nov | -11% | -9% | -10% | |

| 07:00 | EUR | German CPI M/M Nov F | 0.10% | 0.10% | ||

| 07:00 | EUR | German CPI Y/Y Nov F | 2.30% | 2.30% | ||

| 08:15 | CHF | Producer & Import Prices M/M Nov | 0.00% | 0.20% | ||

| 08:15 | CHF | Producer & Import Prices Y/Y Nov | 2.30% | |||

| 08:30 | CHF | SNB Sight Deposit Interest Rate | -0.75% | -0.75% | ||

| 08:30 | CHF | SNB 3-Month Libor Lower Target Range | -1.25% | -1.25% | ||

| 08:30 | CHF | SNB 3-Month Libor Upper Target Range | -0.25% | -0.25% | ||

| 12:45 | EUR | ECB Bank Rate Decision | 0.00% | 0.00% | ||

| 13:30 | CAD | New Housing Price Index M/M Oct | 0.00% | 0.00% | ||

| 13:30 | USD | Import Price Index M/M Nov | -1.00% | 0.50% | ||

| 13:30 | USD | Initial Jobless Claims (DEC 8) | 227K | 231K | ||

| 15:30 | USD | Natural Gas Storage | -81B | -63B |

{kind=link}