The forex markets are having no clear direction for the moment. In particular, positive data from Europe were generally ignored by currencies even though yields and stocks are lifted. At the same time, there is no clarity regarding Brexit after Commons Speaker John Bercow ruled out meaningful vote on the same Brexit deal yesterday. Sterling edged higher earlier in European session but quickly retreated back. Prime Minister Theresa May may finally tell us what’s next after her Cabinet meeting.

Staying in the currency markets, Canadian Dollar is currently the strongest one for today, with help from oil prices. However, it should be noted that WTI crude oil, hitting 59.80, is now in key resistance zone around 60 and reversal could happen any time. New Zealand Dollar is the second strongest, followed by Euro. Australian Dollar, Dollar and Yen are the weakest ones. Nevertheless, given than most pairs are stuck in tight range, the picture can easily change in US session.

In other markets, FTSE is currently up 0.53%. DAX is up 1.13%. CAC is up 0.54%. German 10-year yield jumps 0.029 to 0.117, back above 0.1 handle. Earlier in Asia, Nikkei dropped -0.08%. Hong Kong HSI rose 0.19%. China Shanghai SSE dropped -0.18%. Singapore Strait Times rose 0.25%. Japan 10-year yield dropped -0.008 to -0.044.

UK government looking for Brexit vote solutions

There are reports that EU is going to offer UK a conditional Brexit extension in the summit later this week. With that change in circumstance, Prime Minister Theresa May could bring her deal back to the Commons for another meaningful vote. Additionally, it’s reported that UK could theoretically ask for a long Brexit delay but leave the EU before it runs out.

As Brexit Minister Stephen Barclay noted, Bercow already “pointed to possible solutions” to the current crisis. He added “you can have the same motion but where the circumstances have changed.” Also, Barclay noted “the speaker himself has said that where the will of the House is for a certain course of action, then it is important that the will of the House is respected.” Thus, both an extension or a shift in support, could indicate a change in context.

However, we’d point out that whether there is another vote on Brexit deal or not, and through what workaround, the fundamental question is not solved. That is, is there enough votes to the current Brexit deal through? Without enough votes, all solutions are just solutions to the problem of Brexit vote, not to Brexit itself.

EU officials give strong warnings to UK for clarity and purpose for Brexit extension

European Commission spokesman Margaritis Schinas warned that “We are now exactly 10 days away form the United Kingdom’s withdrawal for the European Union”. And, “It will be for the Prime Minister and Her Majesty’s government to decide on the next steps and then to inform us accordingly and swiftly. The European Council in the art 50 constellation is on Thursday,”

Germany’s Europe Minister Michael Roth warned that “our patience as the European Union is being sorely tested at the moment.” He added “I can only call once again on our British partners in London to make concrete proposals at last on why they want an extension.”

French EU affairs minister Nathalie Loiseau also complained that “this uncertainty is unacceptable”. She added: “We need an initiative, we need something new because if it’s an extension to remain in the same deadlock… How do we get out of this deadlock? – this is a question for the British authorities.” Also, “Grant an extension – what for? Time is not a solution, it’s a method. If there is an objective and a strategy and it has to come from London.”

UK unemployment rate dropped to 3.9%, wage growth solid at 3.4%

UK unemployment rate dropped to 3.9% in the three months to January, down from 4.0% and beat expectation of 4.0%. That’s also the lowest level since the period between November 1974 to January 1975. For men, unemployment rate dropped to 4.0%, lowest since 1975. For women, unemployment rate dropped to 3.8%, lowest since 1971.

Average weekly earnings including bonus rose 3.4% yoy, unchanged from December and beat expectation of 3.2% yoy. Average weekly earnings excluding bonus rose 3.4% yoy, down from December’s 3.5% and matched expectations. Also release, jobless claims rose 27.9k in February, above expectation of 13.1k.

German ZEW improved significantly as major risks considered less dramatic

German ZEW Economic Sentiment improved notably to -3.6 in March, up from -13.4 and beat expectation of -11.0. German ZEW Current Situation, however dropped to 11.1, down from 15.0 and missed expectation of 13.0. Eurozone ZEW Economic Sentiment improved to -2.5, up from -16.6 and beat expectation of -15.1. Eurozone ZEW Current Situation also dropped to -6.6, down from -3.0.

ZEW President Professor Achim Wambach said in release that the significant improvement shows that “major economic risks are considered to be less dramatic than before”. Those include possible delay in Brexit and renewed hope for a deal. Also, “progress made in the negotiations between China and the US to end the trade war between the two nations may also have contributed”. Still the indicators point to “relatively weak growth” in first half in Germany.

Australia house price dropped -2.4% qoq, -5.1% yoy in Q4

Australia house price index dropped -2.4% qoq in Q4, deepened from Q3’s -1.5% qoq and missed expectation of -2.0% qoq. Sydney led the way by dropped -3.7% qoq, followed by Melbourne at -2.4%. Hobart (up 0.7%) and Adelaide (up 0.1%) bucked the trend.

Through the year growth in residential property prices fell 5.1% yoy in the December quarter 2018. Falls were recorded in Sydney (-7.8 per cent), Melbourne (-6.4% yoy), Darwin (-3.5% yoy), Perth (-2.5 % yoy) and Brisbane (-0.3% yoy).

Chief Economist for the ABS, Bruce Hockman said: “While property prices are falling in most capital cities, a tightening in credit supply and reduced demand from investors and owner occupiers have had a more pronounced effect on the larger property markets of Sydney and Melbourne.”

RBA awaits more data to resolve tensions in domestic data

In the March meeting minutes, RBA noted the “tension” between ongoing improvement in job data and slowdown in output growth in H2 2018. Leading indicators pointed to further tightening in the job market and wages growth picked up in Q4. Growth slowed but business and public spending remained positive. However, there continued to be “considerable uncertainty” around consumption outlook, given fall in house prices.

Taken into account the available information, RBA judged that current monetary policy stance was “supporting jobs growth and a gradual lift in inflation”. But “significant uncertainties around the forecasts remained”. The scenarios of a rate hike and rate hike were “more evenly balanced” than over the preceding year. And, “it would be appropriate to hold the cash rate steady while new information became available that could help resolve the current tensions in the domestic economic data.”

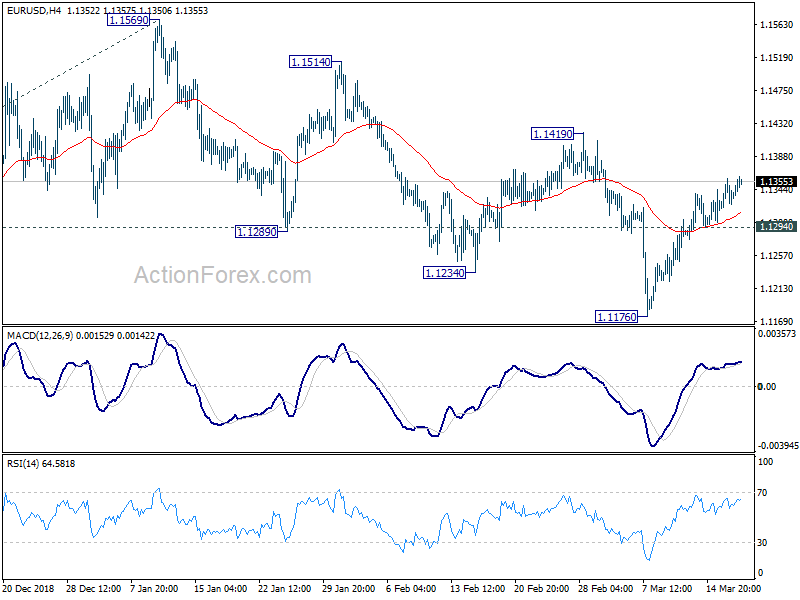

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1319; (P) 1.1340; (R1) 1.1362; More…..

No change in EUR/USD’s outlook. The corrective rebound from 1.1176 could extend higher. But upside should be limited below 1.1419 resistance to bring down trend resumption. On the downside, below 1.1294 minor support will turn bias to the downside for 1.1176 low first. Break of 1.1176 will target 100% projection of 1.1814 to 1.1215 from 1.1569 at 1.0970 next.

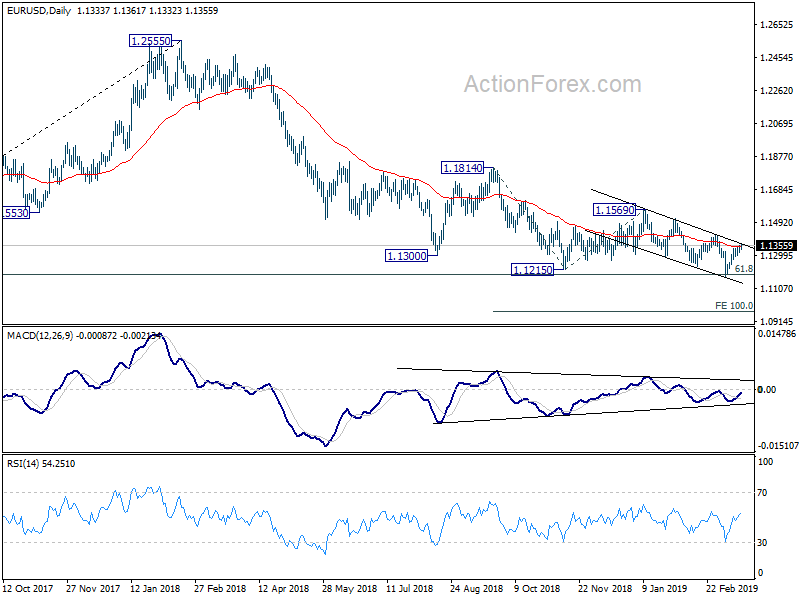

In the bigger picture, down trend from 1.2555 medium term top is still in progress. Bearishness is affirmed by sustained trading below falling 55 week EMA. 61.8% retracement of 1.0339 (2017 low) to 1.2555 at 1.1186 is met. Sustained break there will pave the way to retest 1.0339. On the upside, break of 1.1569 resistance will now indicate completion of such down trend and turn medium term outlook bullish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 20:00 | NZD | Westpac Consumer Confidence Q1 | 103.8 | 109.1 | ||

| 0:30 | AUD | House Price Index Q/Q Q4 | -2.40% | -2.00% | -1.50% | |

| 0:30 | AUD | RBA Minutes Mar | ||||

| 7:00 | CHF | Trade Balance (CHF) Feb | 3.13B | 2.88B | 3.04B | |

| 9:30 | GBP | Jobless Claims Change Feb | 27.0K | 13.1K | 14.2K | 15.7K |

| 9:30 | GBP | Claimant Count Rate Feb | 2.90% | 2.80% | ||

| 9:30 | GBP | ILO Unemployment Rate 3Mths Jan | 3.90% | 4.00% | 4.00% | |

| 9:30 | GBP | Average Weekly Earnings 3M/YoY Jan | 3.40% | 3.20% | 3.40% | |

| 9:30 | GBP | Weekly Earnings ex Bonus 3M/Yo Jan | 3.40% | 3.40% | 3.40% | 3.50% |

| 10:00 | EUR | German ZEW Economic Sentiment Mar | -3.6 | -11 | -13.4 | |

| 10:00 | EUR | German ZEW Current Situation Mar | 11.1 | 13 | 15 | |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Mar | -2.5 | -15.1 | -16.6 | |

| 14:00 | USD | Factory Orders Jan | 0.30% | 0.10% |

{kind=link}