Risk aversion intensifies again today as Trump uses his one old tricky in tariffs again, but turned to Mexico. 5% tariffs will be imposed on all Mexican imports on June 10, and “gradually” move up to 25% in less than 4 months time if Mexico doesn’t help on border security “crisis” of the US. The announce came as German Chancellor Angela Merkel urged Harvard graduates to “tear down walls of ignorance and narrow-mindedness, for nothing has to stay as it is.” in a speech. And she called for “truthfulness in our attitude toward others” which “requires us not to describe lies as truth and truth as lies”.

Yen surges broadly today, together with Swiss Franc, and that in turn reinforced the selloff in Nikkei. Canadian Dollar is the weakest one for today, partly dragged down by renewed selloff in WTI crude oil. Though, Australian and New Zealand Dollar has been rather firm this week despite trade war threats. Dollar is the second weakest for today so far. There are increasing talks of so called “insurance cut” by Fed. But such speculation will have to pass the test of today’s PCE inflation data first.

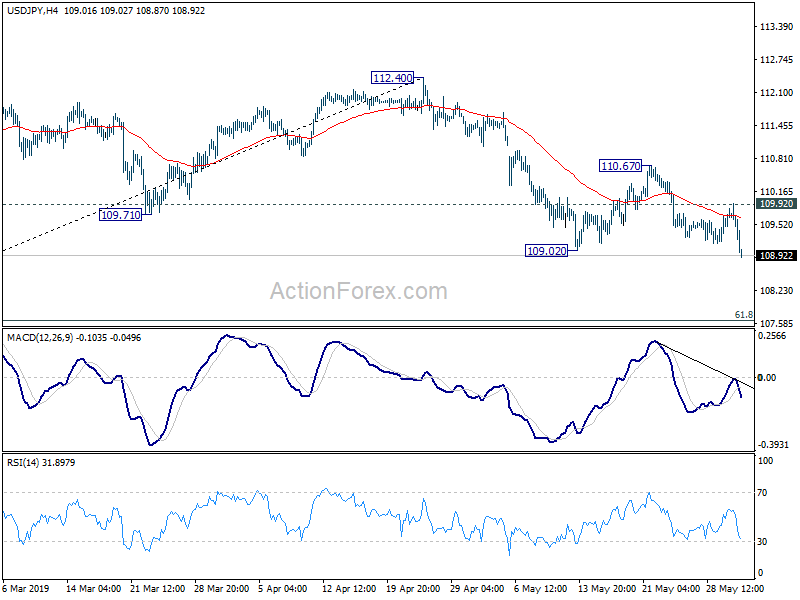

Technically, USD/JPY has finally broken 109.02 support and fall from 112.40 is resuming for 107.63 fibonacci level. EUR/JPY and GBP/JPY are extending near term decline too, targeting 118.62 and 131.51 respectively. After some brief retreat, USD/CAD’s rally resumes today and is on track to 1.3664 resistance. EUR/USD, USD/CHF and AUD/USD are stuck in range as breakout awaited.

In Asia, Nikkei closed down -341.34 pts or -1.63%. Hong Kong HSI is down -0.42%. China Shanghai SSE is down -0.20%. Singapore Strait Times is down -0.78%. Japan 10-year yield is down -0.016 at -0.097. Overnight, DOW closed up 0.17%. S&P 500 rose 0.21%. NASDAQ rose 0.27%. 10-year yield dropped -0.009 to 2.227. DOW future is currently down -200pts and we’d probably see DOW loses 25000 handle before month end.

Trump uses tariffs to stop illegal migrants through Mexico

The highly anticipated “big league statement” of Trump regarding border security turned out to be announcement of the same old “one-trick”. In a rather shocked, he announced, by his tweets, to impose 5% tariff on all Mexican imports, “until such time as illegal migrants coming through Mexico, and into our Country, STOP.” And the tariff will “gradually increase until the Illegal Immigration problem is remedied”.

In the more detailed announcement by the White House, Trump said he was “invoking the authorities granted to me by the International Emergency Economic Powers Act.”. Starting June 10, 5% tariff will be imposed on all goods imported from Mexico. If the “crisis persist”, tariffs will be raised to 10% on July 1, then 15% on August 1, 20% on September 1, and 25% on October 1.

He further warned: “If Mexico fails to act, Tariffs will remain at the high level, and companies located in Mexico may start moving back to the United States to make their products and goods. Companies that relocate to the United States will not pay the Tariffs or be affected in any way.”

Fed Clarida: Interest rate consistent with Talyor-type rule results

Fed Vice Chair Richard Clarida reiterated the view that US economy is in a “very good place”. Also current interest rate lies in the range of neutral and remain appropriate. Softness in recent inflation is seen as “transitory”. Though, he also outlined the conditions for a rate cut, in persistent inflation miss or deterioration in global economic financial developments.

In a speech delivered yesterday, he said “the U.S. economy is in a very good place, with the unemployment rate near a 50-year low, inflationary pressures muted, expected inflation stable, and GDP growth solid and projected to remain so.”

Also, the federal funds rate is now in the range of estimates of its longer-run neutral level, and the unemployment rate is not far below many estimates of u*. And, “plugging these inputs into a 1993 Taylor-type rule produces a federal funds rate between 2.25 and 2.5 percent, which is the range for the policy rate that the FOMC has reaffirmed”.

Fed’s decision to leave interest rate unchanged in May “reflects our view that some of the softness in recent inflation data will prove to be transitory.”

Nevertheless, Clarida also noted “if the incoming data were to show a persistent shortfall in inflation below our 2 percent objective or were it to indicate that global economic and financial developments present a material downside risk to our baseline outlook, then these are developments that the Committee would take into account in assessing the appropriate stance for monetary policy.”

BoC Wilkins: Trade war is a wild card and our major preoccupation

BoC Senior Deputy Governor Carolyn Wilkins reiterated in a speech the central bank’s view that ” the slowdown in late 2018 and early 2019 was temporary.” However, “global trade risks have increased”. Thus, the current accommodation provided by BoC remains “appropriate”. And upcoming rate decisions will remain data dependent, with attention to “household spending, oil markets and the global trade environment.”

She described trade war as the “wild card” on global and domestic outlook. “How costly are trade wars for the global economy? In April, we said tariffs over the past two years and trade policy uncertainty would chop 0.4 per cent from global GDP by the end of 2021—that’s about US$350 billion. While this can only be a rough estimate, we know it matters more for trade-dependent economies like Canada’s.”

Wilkins noted the positive development that US has dropped steel and aluminum tariffs recently, increasing chance of ratification of USMCA. But “other developments are discouraging”, with US and China escalated their dispute and Canada “caught in the crossfire”. She also noted the “potential for more friction between the United States and European Union.”

She warned “if the disputes were to worsen and become long lasting, the outlook would be quite different. Not only would we see weaker economic demand, but the supply side of the economy would also take a hit as companies deal with disruptions to their supply chains. Obviously, this remains a major preoccupation for us.”

Japan unemployment rate dropped, so was consumer confidence

The batch of economic data released from Japan today is mixed. Unemployment rate dropped to 2.4% in April, down from 2.5%, matched expectations. However, better employment was not reflected in retail sales nor consumer sentiment. Retail sales rose 0.5% yoy, missed expectation of 1.0% yoy. Consumer confidence dropped to 39.4, below expectation of 40.6.

Meanwhile, industrial production rose 0.6% mom in April, above expectation of 0.2% mom. However, the road ahead could be bumpy with trade war escalation in May. Housing starts dropped -5.7% yoy in April, below expectation of -0.8% yoy. Tokyo CPI core slowed to 1.1% yoy in May, down from 1.3% yoy and missed expectation of 1.2% yoy.

China PMI manufacturing dropped to 49.4, widening decline, increasing downward pressure

The official China PMI manufacturing dropped to 49.4 in May, down from 50.1 and missed expectation of 49.9. It further confirmed that March’s recovery was a false dawn and the slowdown trajectory in China is ongoing. More importantly, deterioration could quick further with the current round of US-China trade war escalation. Non-manufacturing PMI was unchanged at 54.3.

Analyst Zhang Liqun noted that “the decline was widening, indicating that the downward pressure on the economy has increased.” And, “foundation for economic stabilization has not yet been established.” In particular, new orders index, the export order index decreased significantly, “reflecting the lack of market demand is more prominent, especially the downward pressure on exports”.

Looking at some details: Production dropped -0.4 to 51.7; New order dropped -1.6 to 49.8; New Export order dropped -2.7 to 46.5; Import dropped -2.6 to 47.1; Employment dropped -0.2 to 47.0.

Elsewhere

UK Gfk consumer sentiment improved to -10 in May, up from -13 and beat expectation of -12. Australia private sector credit rose 0.2% mom in April, missed expectation of 0.3% mom. Germany retail sales dropped -2.0% mom in April, below expectation of 0.4% mom.

Looking ahead. UK will release mortgage approvals and M4. Germany will release May CPI flash. Main focus will be US personal income and spending, with PCE inflation. US will release Chicago PMI. Canada GDP will be another major focus, while IPPI and RMPI will also be featured.

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.42; (P) 109.68; (R1) 109.88; More…

USD/JPY drops to as low as 108.87 so far today. Break of 109.02 support indicates resumption of fall from 112.40. Intraday bias is back on the downside for 61.8% retracement of 104.69 to 112.40 at 107.63 next. Sustained trading below 107.63 will pave the way to retest 104.69 low. On the upside, break of 109.92 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

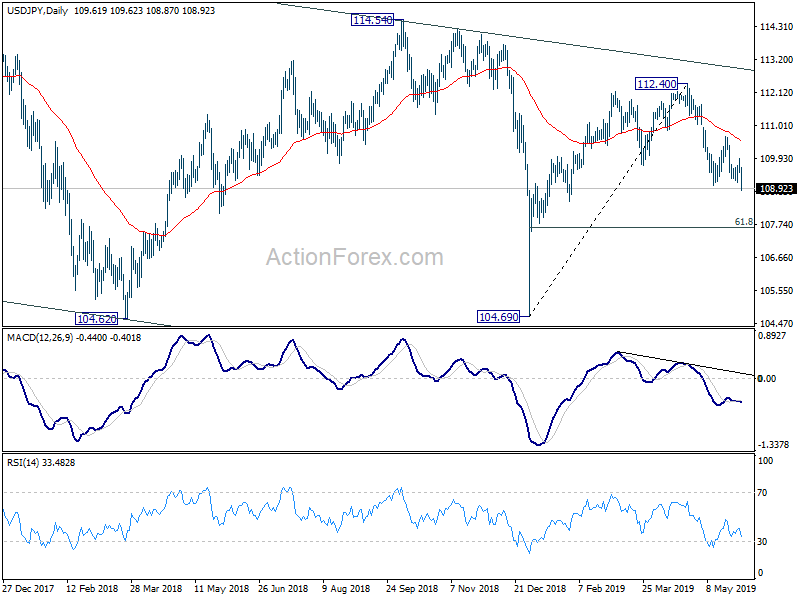

In the bigger picture, USD/JPY is staying inside falling channel from 118.65. Current development suggests that rebound from 104.69 is only a corrective move. And fall from 118.65 is not completed yet. Decisive break of 104.69 will extend the down trend towards 98.97 support (2016 low). For now, we’d expect strong support above there to bring rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | GfK Consumer Confidence May | -10 | -12 | -13 | |

| 23:30 | JPY | Unemployment Rate Apr | 2.40% | 2.40% | 2.50% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y May | 1.10% | 1.20% | 1.30% | |

| 23:50 | JPY | Industrial Production M/M Apr P | 0.60% | 0.20% | -0.60% | |

| 23:50 | JPY | Retail Trade Y/Y Apr | 0.50% | 1.00% | 1.00% | |

| 1:00 | CNY | Manufacturing PMI May | 49.4 | 49.9 | 50.1 | |

| 1:00 | CNY | Non-manufacturing PMI May | 54.3 | 54.3 | 54.3 | |

| 1:30 | AUD | Private Sector Credit M/M Apr | 0.20% | 0.30% | 0.30% | |

| 5:00 | JPY | Consumer Confidence Index May | 39.4 | 40.6 | 40.4 | |

| 5:00 | JPY | Housing Starts Y/Y Apr | -5.70% | -0.80% | 10.00% | |

| 6:00 | EUR | German Retail Sales M/M Apr | -2.00% | 0.40% | -0.20% | |

| 6:30 | CHF | Retail Sales Real Y/Y Apr | -0.80% | -0.70% | ||

| 8:30 | GBP | Mortgage Approvals Apr | 64K | 62K | ||

| 8:30 | GBP | Money Supply M4 M/M Apr | 0.40% | -0.50% | ||

| 12:00 | EUR | German CPI M/M May P | 0.30% | 1.00% | ||

| 12:00 | EUR | German CPI Y/Y May P | 1.60% | 2.00% | ||

| 12:30 | CAD | GDP M/M Mar | 0.30% | -0.10% | ||

| 12:30 | CAD | GDP Y/Y Mar | 1.20% | 1.10% | ||

| 12:30 | CAD | Industrial Product Price M/M Apr | 1.30% | |||

| 12:30 | CAD | Raw Materials Price Index M/M Apr | 2.80% | |||

| 12:30 | USD | Personal Income Apr | 0.30% | 0.10% | ||

| 12:30 | USD | Personal Spending Apr | 0.20% | 0.90% | ||

| 12:30 | USD | PCE Deflator M/M Apr | 0.30% | 0.20% | ||

| 12:30 | USD | PCE Deflator Y/Y Apr | 1.60% | 1.50% | ||

| 12:30 | USD | PCE Core M/M Apr | 0.20% | 0.00% | ||

| 12:30 | USD | PCE Core Y/Y Apr | 1.60% | 1.60% | ||

| 13:45 | USD | Chicago PMI May | 54 | 52.6 | ||

| 14:00 | USD | U. of Mich. Sentiment May F | 101 | 102.4 |

{kind=link}