Canadian Dollar jumps broadly in early US session, after stronger than expected inflation data remove another reason for BoC rate cut. Though, for now, Loonie is overshadowed by Sterling and Swiss Franc, which are the strongest ones. Meanwhile, risk appetite recedes mildly ahead of FOMC rate decision. Dollar is also mixed. Australian and New Zealand Dollars are the weakest ones. Yen is third weakest as German and US treasury yields recover.

There is practically no chance for Fed to cut interest rate from 2.25-2.50% today. It’s too early for the “insurance” rate cut given that Trump and Xi still have a chance to avoid trade war escalation in next week’s G20 meeting. Though there are still two major focuses. First one is on whether Fed will drop the “patient” stance from the statement, which will be an indication on readiness to act. Secondly, we believed that Fed’s new economic projections adopt a base case of no escalation in trade conflicts. Such projections might not be dovish enough to push for a rate cut. Or, if the forecasts are dovish, they’re really rather dovish.

In Europe, currently, FTSE is down -0.30%. DAX is down -0.05%. CAC is up 0.19%. German 10-year yield is up 0.025 at -0.293. Earlier in Asia, Nikkei rose 1.72%. Hong Kong HSI rose 2.56%. China Shanghai SSE rose 0.96%. Singapore Strait Times rose 1.53%. Japan 10-year JGB yield dropped -0.0042 to -0.134.

Canada CPI accelerated to 2.4%, beat expectations

Canada CPI accelerated to 2.4% yoy in May, up from 2.0% yoy and beat expectation of 2.1% yoy. CPI core-common was unchanged at 1.8% yoy, missed expectation of 1.9% yoy. But CPI core-median rose to 2.1% yoy, up from 1.9% yoy and beat expectation of 1.9% yoy. CPI core-trim also accelerated to 2.3% yoy, up from 2.0% yoy and beat expectation of 2.1% yoy.

Looking at some details, prices increased year over year in all eight major components in May, with six components growing at faster rates and two components growing at the same pace compared with April. Higher prices for food (3.5%) and transportation (3.1%) contributed to the increased growth in the all-items index.

UK CPI slowed to 2.0% in May, core CPI slowed to 1.7%

UK CPI rose 0.3% mom in May. Annually, CPI slowed to 2.0% yoy, down from 2.1% yoy. Core CPI slowed to 1.7%, down from 1.8%. All three figures matched expectations. RPI was unchanged at 3.0% yoy, above expectation of 2.9% yoy.

PPI input slowed to 1.3% yoy, beat expectation of 0.8% yoy. PPI output slowed to 1.8% yoy, matched expectations. PPI output core slowed to 2.0% yoy, matched expectations. House price index was unchanged at 1.4% yoy in April, above expectation of 1.1% yoy. CBI trends total orders dropped to -15 in June, down from -10 and missed expectation of -12.

Also release in European session, German PPI slowed to 1.9% yoy in May, down from 2.5% yoy and missed expectation of 2.2% yoy. Eurozone current account deficit narrowed to EUR 20.9B in April, versus expectation of EUR 23.2B.

ECB de Guindos: If inflation expectations start to de-anchor, we will act

ECB Vice President Luis de Guindos said today that the centra bank foresees “lingering softness” n the near term, due to geopolitical factors and trade tensions. Both are weighing on exports and manufacturing in Eurozone economy.

He emphasized that “if we see that inflation expectations start to de-anchor, we will act.” ECB has a “wide range of instruments available”, including forward guidance, TLTRO and QE is one of them. And, “a combination of actions” could be used to restore inflation.

De Guindos’ comments echoed President Mario Draghi’s yesterday. Draghi said, “in the absence of improvement, such that the sustained return of inflation to our aim is threatened, additional stimulus will be required.”

Japan exports shrank for sixth straight months, won’t take sides on US-China trade war

In Japan, trade balance recorded deficit of JPY -0.97T (non seasonally adjusted) in May, first deficit in four months. Exports dropped -7.8% yoy to JPY 5.84T, sixth consecutive month of decline. Imports dropped -1.5% to JPY 6.80T, first decline in three months. Sluggish exports are generally seen as the results of on-going, escalating US-China trade war, which remains a negative factor for the Japanese economy.

Looking at some details (non seasonally adjusted): Exports to China dropped -9.7% yoy. Imports from China dropped -0.9% yoy. Exports to EU dropped -7.1% yoy. Imports from EU rose 8.7% yoy. Exports to US rose 3.3% yoy. Imports from US dropped -1.6% yoy.

Separately, Masatsugu Asakawa, Japan’s vice finance minister for international affairs, said more substantial talks on trade policy will be held in the G20 summit in Osaka next week. But he also noted that “Japan won’t take sides on US-China trade friction, our stance is to not take steps that violate WTO rules.”

Asian business sentiment sank to decade low, not just uncertainty but true slowdown

The Thomson Reuters/INSEAD Asian Business Sentiment Index dropped sharply from 63 to 53 in Q2. Worries over US-China trade war sent sentiments down to the worst reading since Q2 of 2009. The index tracks companies’ six-month outlook. The survey interviewed 95 companies in 11 Asia-Pacific countries that together contribute about a third of GDP and are home to 45% of the world’s population. It was conducted from May 31 to June 14.

Antonio Fatas, professor at global business school INSEAD said “it was the uncertainty about the trade war and people were worried about the future”. And, “after four quarters of low numbers that now, it’s not just uncertainty. This is a true slowdown in growth. We see activity declining — it’s not just the expectation that activity will decline.”

China: Four decades of history shows it’s possible to have positive outcomes in Xi-Trump meeting

Regarding the upcoming meeting between Trump and Xi at G20, Chinese Foreign Ministry spokesman Lu Kang said “The two leaders will talk about whatever they want”. And, “a deal is not only in the interests of the two peoples but meets the aspirations of the whole world.” He added “I’m not getting ahead of myself, but communication over four decades shows it is possible to achieve positive outcomes.”

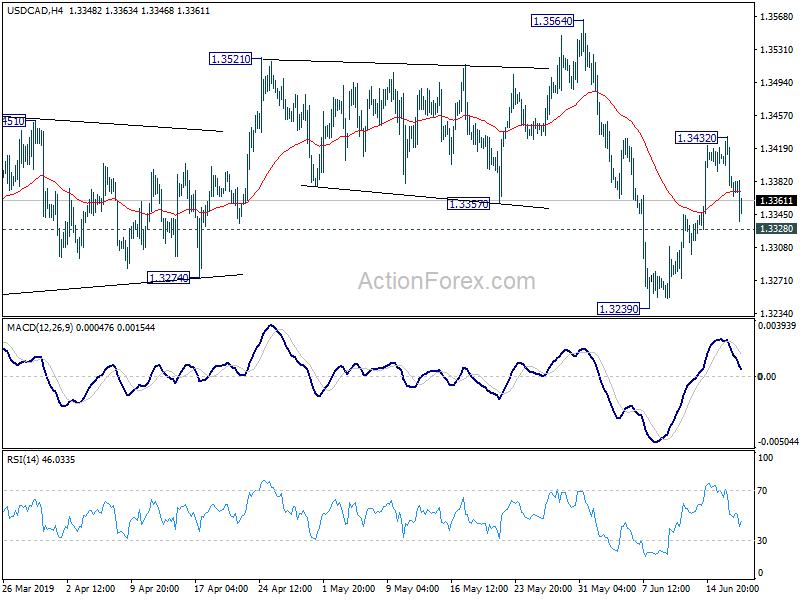

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3357; (P) 1.3395; (R1) 1.3416; More…

USD/CAD drops notably today but stays above 1.3328 minor support. Intraday bias remains neutral first and another rise is still in favor with 1.3328 minor support intact. Above 1.3432 will resume the rebound from 1.3239 to 1.3564 resistance next. On the downside, below 1.3328 minor support will turn intraday bias back to the downside for 1.3239 support instead.

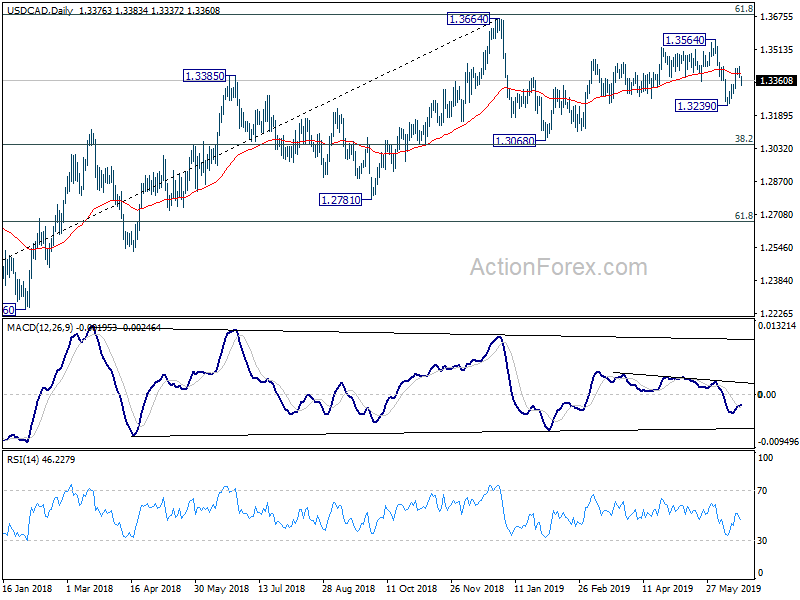

In the bigger picture, outlook is turned mixed after USD/CAD drew strong support from 55 week EMA (now at 1.3232) and rebounded. Nevertheless, sustained break of 61.8% retracement of 1.4689 (2016 high) to 1.2061 at 1.3685, is needed to confirm resumption of up trend from 1.2061 (2017 low), towards 1.4689. Otherwise, medium term outlook will stay neutral first. Break of 1.3239 will revive the case of medium term topping at 1.3664. And, decisive break of 1.3068 cluster support (38.2% retracement of 1.2061 to 1.3664 at 1.3052) will confirm and pave the way to 61.8% retracement at 1.2673 next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Current Account (NZD) Q1 | 0.68B | 0.16B | -3.26B | -3.49B |

| 23:50 | JPY | Trade Balance (JPY) May | -0.61T | -0.80T | -0.11T | -0.17T |

| 00:30 | AUD | Westpac Leading Index M/M May | -0.10% | -0.09% | -0.10% | |

| 06:00 | EUR | German PPI M/M May | -0.10% | 0.20% | 0.50% | |

| 06:00 | EUR | German PPI Y/Y May | 1.90% | 2.20% | 2.50% | |

| 08:00 | EUR | Eurozone Current Account (EUR) Apr | 20.9B | 23.2B | 24.7B | |

| 08:30 | GBP | CPI M/M May | 0.30% | 0.30% | 0.60% | |

| 08:30 | GBP | CPI Y/Y May | 2.00% | 2.00% | 2.10% | |

| 08:30 | GBP | Core CPI Y/Y May | 1.70% | 1.70% | 1.80% | |

| 08:30 | GBP | RPI M/M May | 0.30% | 0.20% | 1.10% | |

| 08:30 | GBP | RPI Y/Y May | 3.00% | 2.90% | 3.00% | |

| 08:30 | GBP | PPI Input M/M May | 0.00% | 0.20% | 1.10% | |

| 08:30 | GBP | PPI Input Y/Y May | 1.30% | 0.80% | 3.80% | 4.50% |

| 08:30 | GBP | PPI Output M/M May | 0.30% | 0.20% | 0.30% | |

| 08:30 | GBP | PPI Output Y/Y May | 1.80% | 1.80% | 2.10% | |

| 08:30 | GBP | PPI Output Core M/M May | 0.10% | 0.10% | 0.20% | |

| 08:30 | GBP | PPI Output Core Y/Y May | 2.00% | 2.00% | 2.20% | |

| 08:30 | GBP | House Price Index Y/Y Apr | 1.40% | 1.10% | 1.40% | |

| 10:00 | GBP | CBI Trends Total Orders Jun | -15 | -12 | -10 | |

| 12:30 | CAD | CPI M/M May | 0.40% | 0.10% | 0.40% | |

| 12:30 | CAD | CPI Y/Y May | 2.40% | 2.10% | 2.00% | |

| 12:30 | CAD | CPI Core – Common Y/Y May | 1.80% | 1.90% | 1.80% | |

| 12:30 | CAD | CPI Core – Median Y/Y May | 2.10% | 1.90% | 1.90% | |

| 12:30 | CAD | CPI Core – Trim Y/Y May | 2.30% | 2.10% | 2.00% | |

| 14:30 | USD | Crude Oil Inventories | -1.5M | 2.2M | ||

| 18:00 | USD | FOMC Rate Decision (Upper Bound) | 2.50% | 2.50% | ||

| 18:00 | USD | FOMC Rate Decision (Lower Bound) | 2.25% | 2.25% | ||

| 18:30 | USD | Fed Chair Powell Press Conference |

{kind=link}