Selloff in Sterling remains the focus in Asian session today, as markets are adding their best to no-deal Brexit. The currency markets are relatively quiet elsewhere. Canadian Dollar is currently the second weakest, then Euro. Yen and Swiss Franc are the strongest, with help by falling treasury yields. Dollar is the third strongest as markets await Fed’s rate cut tomorrow.

Technically, GBP/USD is in downside acceleration and should be targeting 1.1946 low next. GBP/JPY is on track to retest 131.51 low and break will resume fall from 156.96 towards 122.36 low in medium term. EUR/GBP’s strong break of 0.9101 key resistance also carry long term bullish implication and the cross should target 0.9305 (2017 high). Both upside USD/CHF and USD/JPY lost upside moment ahead of near term resistance. The greenback will likely turn into consolidation first, in general, except versus Pound.

In Asia, Nikkei is trading up 0.33%. Hong Kong HSI is up 0.32%. China Shanghai is up 0.56%. Singapore Strait Times is up 0.15%. Japan 10-year JGB yield is down -0.0033 at -0.149. Overnight, DOW rose 0.11%. S&P 500 dropped -0.16%. NASDAQ dropped -0.44%. 10-year yield dropped -0.026 to 2.055.

UK Johnson: Brexit presents enormous opportunities for our country

Sterling’s selloff continues today as markets are adding their bets to no deal Brexit. UK Prime Minister Boris Johnson is insisting that he could get a new Brexit deal with the EU. He said in televised comments that “we’re very confident, with goodwill on both sides, two mature political entities — the U.K. and EU — can get this done”.

And, “it’s responsible for any government to prepare for a no deal if we absolutely have to. That’s the message I’ve been getting across to our European friends. I’m very confident we’ll get there.” He also insisted that the Irish backstop is “dead” along with former PM Theresa May’s withdrawal agreement.

Johnson also emphasized that “Once we leave the EU on Oct. 31, we will have a historic opportunity to introduce new schemes to support farming – and we will make sure that farmers gets a better deal”. And, “Brexit presents enormous opportunities for our country, and it’s time we looked to the future with pride and optimism.”

At this point, there is no sign of EU shifting its position yet. That is, the negotiation for the Brexit Withdrawal Agreement was closed and won’t be re-opened. European Commission also indicated that while an orderly withdrawal is in everyone’s interest, the bloc is well-prepared for a no-deal Brexit.

BoJ stands pat, economy to continue on an expanding trend

BoJ left monetary policy unchanged today as widely expected. Under the yield curve control framework, short-term policy interest rate is held at -0.10%. 10-year JGB yield will be held at around zero percent with JGB purchases. Monetary base will increase at an annual pace of around JPY 80T. The decisions are made with 7-2 vote with Y. Harada and G. Kataoka dissented again.

In the outlook for economic activity and prices report, BoJ said the economy is “likely to continue on an expanding trend throughout the projection period” through fiscal 2021. Exports are projected to “show some weakness” for the time being, but are still expected to be on a “moderate increasing trend”. Domestic demand would “follow an uptrend” against the background of highly accommodative financial conditions and government spending.

Regarding inflation, all item CPI “continued to show relatively weak developments”. But “further price rises are likely”. Year-on-year rate of change in CPI is “likely to increase gradually toward 2 percent”. And both growth and CPI projections are “more or less unchanged” from previous projections.

Risks to economic activity are “skewed to the downside”, particularly regarding overseas developments. Risks to prices are also “skewed to the downside”. The momentum towards 2% inflation target is “maintained” but is “not yet sufficiently firm”.

Japan industrial production dropped -3.6% in indecisive fluctuations

Japan industrial production dropped sharply by -3.6% mom in June, much worst than expectation of -1.8% mom. That’s also the largest decline since January 2018. Shipments dropped -3.3% mom while inventories rose 0.3% mom.

A Ministry of Economy, Trade and Industry said in the press briefing that the decline was a reversal of the unexpectedly strong production in the preceding months.” He added, “we don’t believe there is a downward trend, though there isn’t an upward trend either”. Production just “fluctuates indecisively”.

Also from Japan, unemployment rate improved to 2.3% in June, down from 2.4%. Number of people in work hit record 67.5m. Ministry of Internal Affairs and Communications said “the jobless rate has been firm and moving narrowly at that level”.

Looking ahead

Lots of Eurozone data will be featured in European session. France GDP, Germany Gfk consumer sentiment and CPI will be released. Eurozone will publish confidence indicators. Swiss will release KOF economic barometer.

Later in the day, US personal income and spending, with PCE inflation will be the major focus, together with consumer confidence. Pending home sales and S&P Case-Shiller house price will also be released.

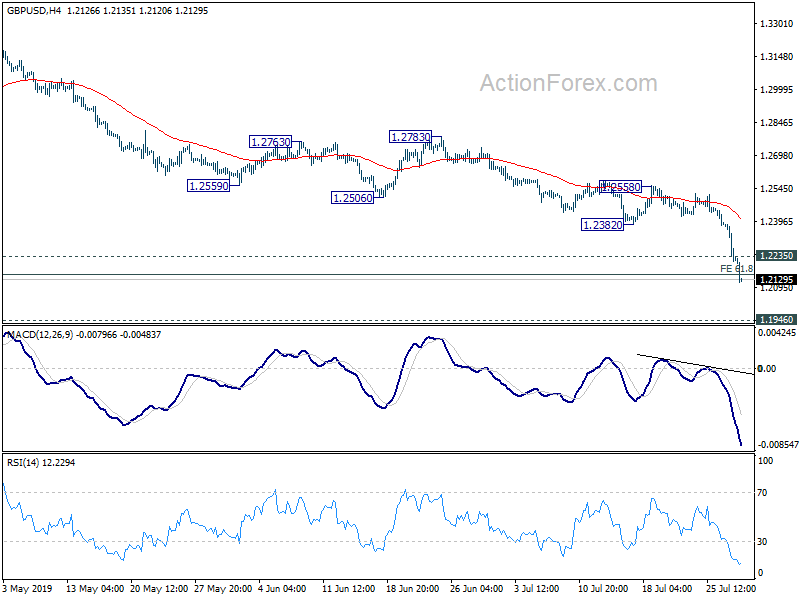

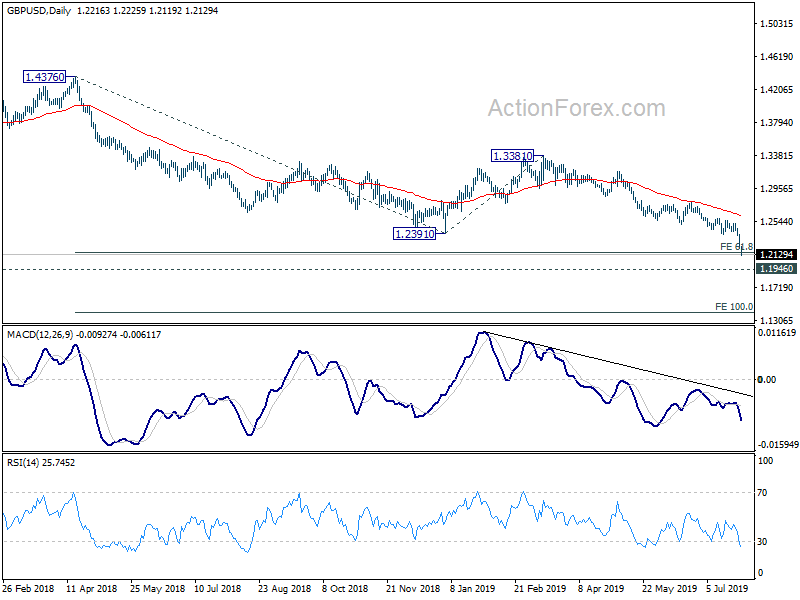

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2159; (P) 1.2272; (R1) 1.2331; More…

GBP/USD’s decline continues today and accelerates to as low as 1.2119 so far, breaking 61.8% projection of 1.4376 to 1.2391 from 1.3381 at 1.2154. There is no sign of bottoming yet. Intraday bias stays on the downside for 1.1946 low next. We’d be cautious on bottoming there. But break will target 100% projection at 1.1396. On the upside, above 1.2235 minor resistance will turn intraday bias neutral and bring consolidation. But recovery should be limited by 1.2383 support turned resistance to bring fall resumption.

In the bigger picture, down trend from 1.4376 (2018 high) is still in progress and is resuming. Such decline should target a test on 1.1946 long term bottom (2016 low) next. For now, we don’t expect a firm break there yet. Hence, focus will be on bottoming signal as it approaches 1.1946. However, firm break of 1.1946 will resume down trend from 2.1161 (2007 high) to 61.8% projection of 1.7190 to 1.1946 from 1.4376 at 1.1135. In any case, medium term outlook will stay bearish as long as 1.3381 resistance holds, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Consensus | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Jun | -3.90% | 13.20% | 13.50% | |

| 23:30 | JPY | Jobless Rate Jun | 2.30% | 2.40% | 2.40% | |

| 23:50 | JPY | Industrial Production M/M Jun P | -3.60% | -1.80% | 2.00% | |

| 1:30 | AUD | Building Approvals M/M Jun | -1.20% | 0.20% | 0.70% | 0.30% |

| 2:00 | JPY | BOJ Rate Decision | -0.10% | -0.10% | -0.10% | |

| 5:30 | EUR | French GDP Q/Q Q2 P | 0.30% | 0.30% | ||

| 6:00 | EUR | German GfK Consumer Confidence Aug | 9.7 | 9.8 | ||

| 7:00 | CHF | KOF Leading Indicator Jul | 93.3 | 93.6 | ||

| 9:00 | EUR | Eurozone Business Climate Indicator Jul | 0.1 | 0.17 | ||

| 9:00 | EUR | Eurozone Economic Confidence Jul | 102.7 | 103.3 | ||

| 9:00 | EUR | Eurozone Industrial Confidence Jul | -6.7 | -5.6 | ||

| 9:00 | EUR | Eurozone Services Confidence Jul | 10.7 | 11 | ||

| 9:00 | EUR | Eurozone Consumer Confidence Jul F | -6.6 | -6.6 | ||

| 12:00 | EUR | German CPI M/M Jull P | 0.30% | 0.30% | ||

| 12:00 | EUR | German CPI Y/Y Jull P | 1.50% | 1.60% | ||

| 12:30 | USD | Personal Income Jun | 0.30% | 0.50% | ||

| 12:30 | USD | Personal Spending Jun | 0.30% | 0.40% | ||

| 12:30 | USD | PCE Deflator M/M Jun | 0.10% | 0.20% | ||

| 12:30 | USD | PCE Deflator Y/Y Jun | 1.50% | 1.50% | ||

| 12:30 | USD | PCE Core M/M Jun | 0.20% | 0.20% | ||

| 12:30 | USD | PCE Core Y/Y Jun | 1.70% | 1.60% | ||

| 13:00 | USD | S&P/Case-Shiller Composite-20 Y/Y May | 2.40% | 2.54% | ||

| 14:00 | USD | Pending Home Sales M/M Jun | 0.30% | 1.10% | ||

| 14:00 | USD | Consumer Confidence Index Jul | 125 | 121.5 |

{kind=link}