Dollar trades broadly higher this week so far, but strength is limited by weakness in treasury yields and risk aversion. WTI crude oil dropped as low as 42.75 yesterday before recovering mildly to 43.5. DOW and S&P 500 retreated after hitting records highs on Monday and closed lower by -0.29% and -0.67% respectively. Nikkei followed and is trading down -0.48% at the time of writing. Notable weakness is seen in 30 year yield while extends this year’s decline and lost -0.053 to close at 2.735. 10 year yield also closed lower by -0.037 but stays above last week’s low at 2.103 so far. In other markets, Gold remains weak and struggles to regain 1250 after dipping to 1242.4.

Known dove Chicago Fed President Charles Evans said that the decisions on monetary policies is "much more challenging from here on out". He pointed to latest weak inflation data and said they "make me a little nervous". Evans said that Fed can "go until December and make a judgement that maybe three is the right number or maybe two is the right number". That is, the comments made it further clearer that Evans prefers Fed to pause hiking interest rates for now and don’t move in September. Currently, fed fund futures are only pricing in 13.1% chance of another hike in September, comparing to 28.8% pricing last week.

30 year yield lost hold of 38.2% retracement of 2.102 to 3.201 at 2.781 overnight and closed down at 3.735. Note that the TYX was rejected from key clear resistance at 3.255 twice. And the depth of decline now suggests that TYX is heading back to 61.8% retracement at 2.52 and possibly below. 10 year yield is kept well below 2.229 resistance and is vulnerable for another fall to 2.0 handle. While dollar index breached 97.77 resistance, the development warrants no trend reversal yet. Overall, while Dollar has stabilized, more is needed to prove that its trend is reversing.

Sterling pressured further by political uncertianties

Sterling continues to trade as the weakest major currency for the week. The selloff was triggered by comments from BoE Governor Mark Carney that it’s not the time for rate hike yet despite some calls for it in the MPC. The Pound was also also pressured by domestic political uncertainties. Prime Minister Theresa is forming a coalition with North Ireland’s Democratic Unionist Party after her Conservatives lost majority in the House of Commons. However, it’s reported that DUP believed conservatives cannot take the partnership for granted. And so far, no deal was reached between the parties after 10 days of talks. Meanwhile, more than 50 Labour politicians signed a joint statement to "stop the Tories in their tracks" over hard Brexit.

ECB Cœuré favors moving Euro clearing back

ECB executive board member Benoît Cœuré argued that it’s better for Euro clearing to move from London to EU after Brexit. Cœuré said in an interview that "we need to ensure that we can preserve a framework that ensures the safety and stability of the financial system when the UK is no longer a member of the EU." And, "in this regard, we think the European Commission proposals to amend [the rules] are a step in the right direction." On the other hand, BoE Governor Mark Carney said that moving the EUR 900b a day clearing from London is in "no one’s economic interest". Carney argue that would "reduce the benefits of central clearing" and "any development which prevented EU27 firms from continuing to clear trades in the UK would split liquidity between a less liquid onshore market for EU firms and a more liquid offshore market for everyone else."

BoJ minutes: Members comfortable with fluctation in bond purcahses

The minutes of BoJ’s April meeting showed that policy makers were comfortable with the fluctuation in JGB purchases. The minutes noted that "members reaffirmed their view that debt purchases will fluctuate within a range depending on market conditions and agreed this poses no problems to the BOJ’s guidance for market operations." This came into question as BoJ recently slowed down the bong purchases. And with the current pace, the total annual increase could be projected as JPY 60T, instead of JPY 80T as the central noted in its communications. Nonetheless, it’s been clear that BoJ changed its approach last year to the so called Yield Curve Control framework. That is, the central bank is targeting to keep long term yield at zero, instead of a figure of asset purchase.

On the data front

Australia Westpac leading index rose 0.0% mom in May. Japan all industry index rose 2.1% mom in April. UK will release public sector borrowing in European session. US will release existing home sales later in the day.

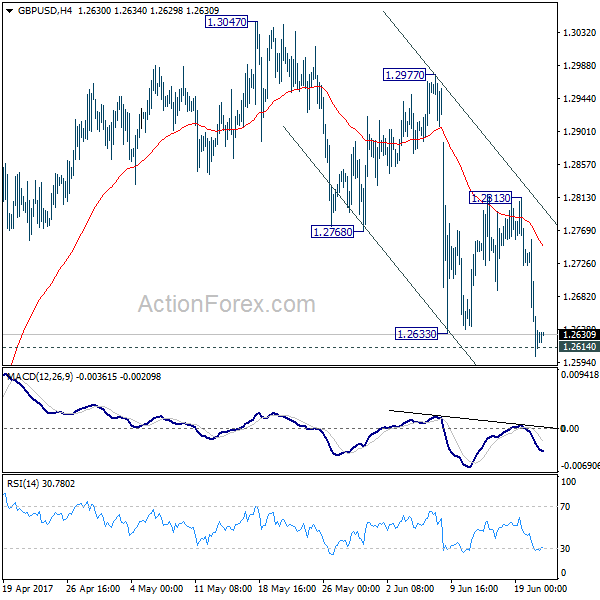

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2565; (P) 1.2661; (R1) 1.2721; More…

GBP/USD’s decline and break of 1.2633 support indicates resumption of fall from 1.3047. Intraday bias is back on the downside for deeper decline. As noted before, we’re still favoring the bearish case that consolidation pattern from 1.1946 has completed at 1.3047 already. Sustained break of 1.2614 resistance turned support should confirm our bearish view and target a test on 1.1946 low next. However, break of 1.2813 resistance will dampen our view and turn bias back to the upside for 1.3047 and above.

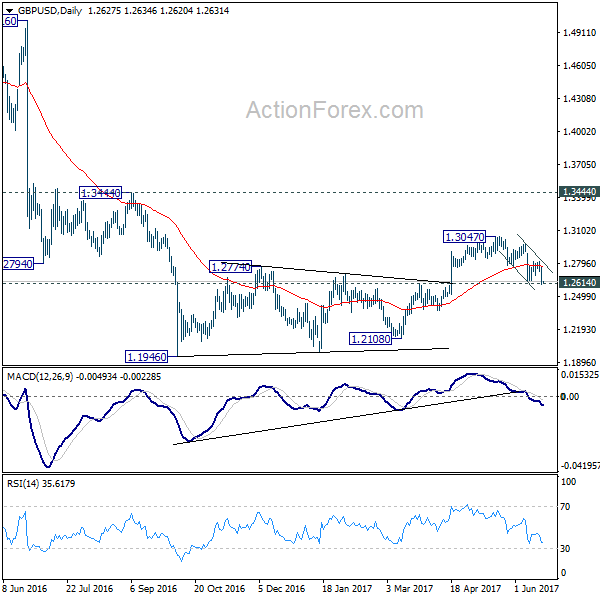

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. Price actions from 1.1946 medium term low are seen as a consolidation pattern, which could have completed after hitting 55 week EMA. Break of 1.1946 low will target 61.8% projection of 1.5016 to 1.1946 from 1.3047 at 1.1150 next. In case the consolidation from 1.1946 extends, outlook will stay remain bearish as long as 1.3444 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BOJ Minutes April Meeting | ||||

| 0:30 | AUD | Westpac Leading Index M/M May | 0.00% | -0.10% | ||

| 4:30 | JPY | All Industry Activity Index M/M Apr | 1.60% | -0.60% | ||

| 8:30 | GBP | Public Sector Net Borrowing (GBP) May | 7.3B | 9.6B | ||

| 14:00 | USD | Existing Home Sales May | 5.54M | 5.57M | ||

| 14:30 | USD | Crude Oil Inventories | -1.7M | |||

| 21:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% |

{kind=link}