Markets are generally quiet in a typical Monday. Sterling is trading generally lower. Prime Minister Boris Johnson’s push for general election ahead of Brexit deadline will likely be voted down today. But it’s reported that he’s planning to block the parliament’s attempts at enforcing Brexit extension. At this point, Swiss Franc is the second weakest followed by Canadian Dollar. Australian Dollar is the strongest one, followed by Yen, suggesting rather calm risk sentiments.

Technically, further rises are in favor Yen crosses in general. But rebounds since last week are generally seen as corrective. Thus, we’d look for sign of loss of momentum ahead. Similarly, EUR/USD, GBP/USD and AUD/USD could extend current rebound. But such rises are also seen as corrective, as Dollar is pulling back. Hence, we’d also look for loss of momentum ahead.

In Asia, Nikkei rose 0.57%. Hong Kong HSI is down -0.04%. China Shanghai SSE rose 0.62%. Singapore Strait Times is up 0.10%. Japan 10-year JGB yield is down -0.0113 at -0.256.

Japan Q2 GDP finalized at 0.3% qoq, private consumption driven

Japan Q2 GDP growth was finalized at 0.3% qoq, revised down from 0.4% qoq. The economy grew at annualized pace of 1.3%, sharply lower than preliminary reading of 1.8%. GDP deflator was finalized at 0.4% yoy, unrevised.

Growth was primarily driven by consumer spending, which grew 0.6% qoq. While continued growth in private consumption is expected ahead, it could take a hit from the planned sales tax hike in October.

Meanwhile, business investment was weak and just grew 0.2% qoq. Considering global slowdown and uncertainties from trade tensions, business investment has already shown some resilience. Yet, as US-China trade war intensified in Q3, there is more headwind for businesses for the rest of the year.

Also from Japan, current account surplus narrowed to JPY 1.65T in July, slightly below expectation of JPY 1.70T.

ECB stimulus expected in the week ahead

ECB meeting this week will be a major focus as it’s widely expected to announce some sort of new stimulus program. The question is on what the package would be. Some expected a cut in already negative deposit rate, by -10bps or -20bps. The forward guidance of keeping interest rates at current level or lower could be extended. Also, there might be a restart of QE, probably in the size of EUR 45-60B per month. There could also be a tiering system on interest rate. Elsewhere, US will release CPI and retail sales. UK will release GDP, productions and employment data.

Here are some highlights for the week:

- Monday: New Zealand manufacturing sales; Australia home loans; Japan GDP final, current account; Swiss unemployment rate; Germany trade balance; Eurozone Sentix investor confidence; UK GDP, industrial and manufacturing productions, goods trade balance.

- Tuesday: Japan M2, machine tools orders; China CPI, PPI; Australia NAB business confidence; UK employment; Canada housing starts, building permits.

- Wednesday: Japan BSI manufacturing index; Australia Westpac consumer sentiment; US PPI

- Thursday: Japan PPI, tertiary industry index; UK RICS house price balance; Germany CPI final; Swiss PPI; Eurozone industrial production, ECB rate decision; Canada new housing price index US CPI, jobless claims.

- Friday: New Zealand Business NZ manufacturing; Eurozone trade balance; US retail sales, import prices, business inventories, U of Michigan consumer sentiment

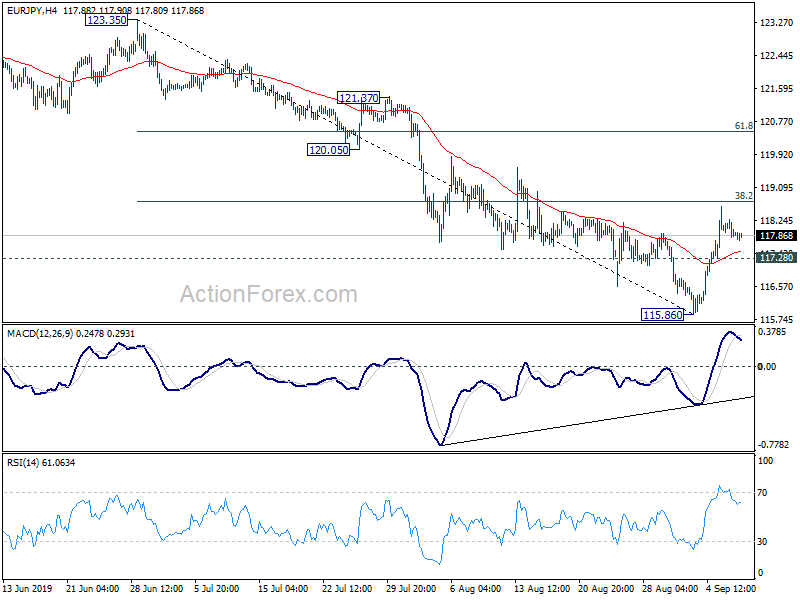

EUR/JPY Daily Outlook

Daily Pivots: (S1) 117.70; (P) 117.99; (R1) 118.15; More….

.With 117.28 minor support intact, EUR/JPY’s rebound from 115.86 short term bottom could extend higher. Break of 38.2% retracement of 123.35 to 115.86 at 118.72 will pave the way to 61.8% retracement at 120.48. On the downside, break of 11.7.28 minor support will turn bias back to the downside for retesting 115.86 instead.

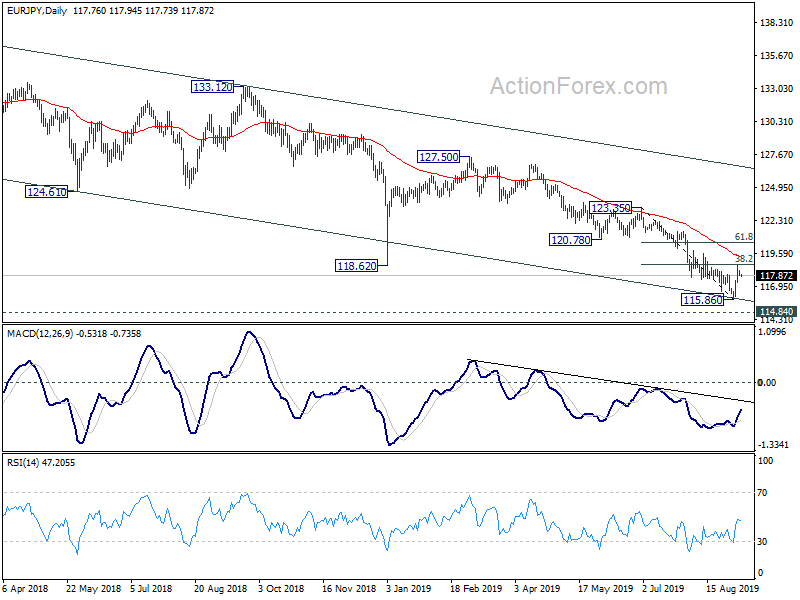

In the bigger picture, down trend from 137.49 (2018 high) is still in progress. It’s seen as a falling leg of multi-year sideway pattern. Deeper fall could be seen to 109.48 (2016 low and below). On the upside, break of 120.78 support turned resistance is needed to be the first sign medium term reversal. Otherwise, outlook will remain bearish in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Manufacturing Activity Q2 | -0.70% | 1.00% | 0.80% | |

| 23:50 | JPY | Current Account (JPY) Jul | 1.65T | 1.70T | 1.94T | |

| 23:50 | JPY | GDP Q/Q Q2 F | 0.30% | 0.30% | 0.40% | |

| 23:50 | JPY | GDP Deflator Y/Y Q2 F | 0.40% | 0.40% | 0.40% | |

| 1:30 | AUD | Home Loans M/M Jul | 5.00% | 0.50% | -0.90% | -0.80% |

| 5:45 | CHF | Unemployment Rate Aug | 2.3% | 2.30% | 2.30% | |

| 6:00 | EUR | German Trade Balance (EUR) Jul | 20.2B | 18.8B | 18.1B | 18.0B |

| 8:30 | EUR | Eurozone Sentix Investor Confidence Sep | -16 | -13.7 | ||

| 8:30 | GBP | Monthly GDP M/M Jul | 0.10% | 0.00% | ||

| 8:30 | GBP | Industrial Production M/M Jul | 0.00% | -0.10% | ||

| 8:30 | GBP | Industrial Production Y/Y Jul | -1.00% | -0.60% | ||

| 8:30 | GBP | Manufacturing Production M/M Jul | 0.00% | -0.20% | ||

| 8:30 | GBP | Manufacturing Production Y/Y Jul | -1.00% | -1.40% | ||

| 8:30 | GBP | Construction Output M/M Jul | 0.20% | -0.70% | ||

| 8:30 | GBP | Index of Services 3M/3M Jul | 0.10% | 0.10% | ||

| 8:30 | GBP | Visible Trade Balance (GBP) Jul | -9.6B | -7.0B |

{kind=link}