Sterling rises broadly today on optimism that a Brexit deal could finally be reached by the end of next month. For now, Swiss Franc and Yen are following as next strongest. On the other hand, Dollar turns soft as post-FOMC lift continued to fade, followed by New Zealand Dollar and than Canadian. For the week, the Pound is currently the strongest one, followed by Yen and then Canadian. Kiwi is the weakest, followed by Aussie.

Technically, GBP/USD takes out 1.2502 fibonacci level solidly and should target next level at 1.2837. GBP/JPY might finally make up its mind through 135.07 fibonacci level to 140.33. EUR/GBP’s decline from 0.9324 is in progress for next key support at 0.8472.

In Asia, Nikkei rose 0.16%. Hong Kong HSI is flat. China Shanghai SSE is up 0.10%. Singapore Strait Times is up 0.05%. Japan 10-year JGB yield is up 0.0066 at -0.219. Overnight, DOW dropped -0.19%. S&P 500 closed flat. NASDAQ rose 0.07%. 10-year yield dropped -0.012 to 1.774.

EU Juncker said Brexit deal could be reached by Oct 31

Sterling rises notably after comments from European Commission President Jean-Claude Juncker. He told Sky News that he didn’t have “an erotic relation” to the so-called Irish backstop. As long as alternative arrangements are in place to achieve all main objectives of the backstop, he’s prepared to remove it from the Brexit withdrawal agreement. He also said that no-deal Brexit would have “catastrophic consequences” and he was doing “everything to get a deal Juncker believed that a Brexit deal can be reached by October 31.

Chinese officials to visit US farms next week to build good will

Deputy level US-China trade talks stated yesterday in Washington in preparation for the top level meeting next month. It’s reported that agriculture was having a disproportionate amount of time in the discussions. But there is not official confirmation of the news. Yet separately, Agriculture Department Secretary Sonny Perdue said yesterday that Chinese officials will visit American farms next week as part of efforts to “build goodwill.” But he wasn’t sure if China will announcement any purchases during the visit.

At the same time, Commerce Secretary Wilbur Ross reiterated that the administration is pushing for something “more complicated than just buying a few more soybeans.” He told Fox Business Network that “what we need is to correct the big imbalances, not just the current trade deficit, but also the structural imbalances, the impediments to market access, disrespect for intellectual property, forced technology transfers.”

Lagarde: Fragile global growth under threat

Ex-IMF chief, soon to be ECB President, Christine Lagarde urged global policymakers to “try to reduce the fragility and … resolve the uncertainty,” facing the global economy. She noted that “what we have at the moment is a rather mediocre growth” which is “fragile and it is under threat.”

She added that “central bankers have done an awful lot and were for many years regarded as the only game in town”. And government policies must not step up. However, she also warned that experience showed political intervention on central banks “doesn’t pan out very well”. And central banks should strive to be “predictable”, because “there is enough uncertainty around the world, not to add the uncertainty of what a central banker is going to do.”

Japan CPI core slowed to 0.5%, further away from BoJ’s target

Japan CPI core (all items less fresh food) slowed to 0.5% yoy in August, down from 0.6% yoy, matched expectations. All items CPI slowed to 0.3% yoy, down from 0.5% yoy. CPI core-core (all items less fresh food and energy) was unchanged at 0.6% yoy.

The CPI core reading moved further away from BoJ’s 2% inflation target. It’s expected to stay subdued in the coming months as as lower mobile phone service fees and education costs weigh on prices. Additionally, the upcoming sales tax hike (from 8% to 10%) in October may further hit consumer sentiment and weigh on underlying inflation.

Elsewhere

German PPI came in at -0.5% mom, 0.3% yoy, well below expectation of 0.0% mom, 0.6% yoy. Canada retail sales will be a major focus today. Eurozone will also release consumer confidence.

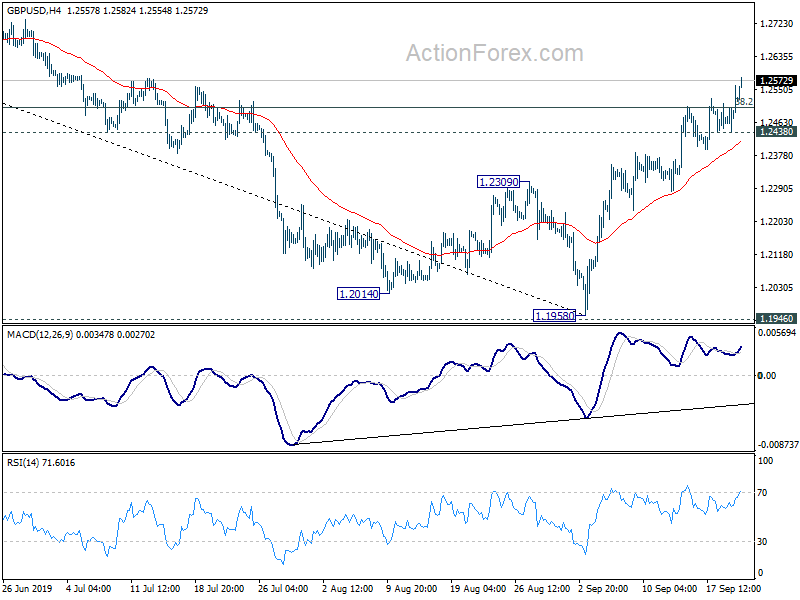

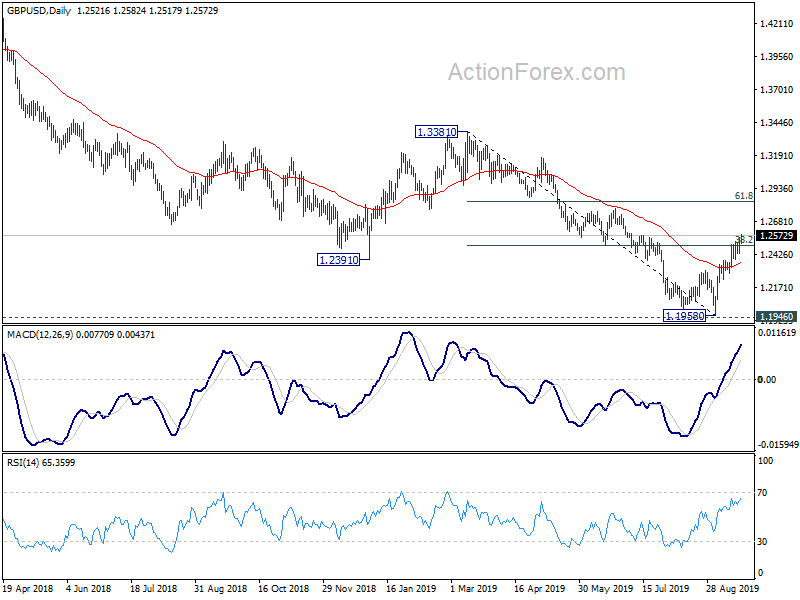

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2455; (P) 1.2507; (R1) 1.2577; More….

GBP/USD’s rally resumes after brief consolidations and hits as high as 1.2582 so far. Intraday bias is back on the upside. With 38.2% retracement of 1.3381 to 1.1958 at 1.2502 firmly taken out, next target is 61.8% retracement at 1.2837. On the downside, below 1.2438 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, we’d remain cautious on medium term bottoming around 1.1946 (2016 low). Sustained trading above 55 week EMA (now at 1.2769) will extend the consolidation pattern from 1.1946 with another rise to 1.4376 resistance. Nevertheless, decisive break of 1.1946 will resume down trend from 2.1161 (2007 high) to 61.8% projection of 1.7190 to 1.1946 from 1.4376 at 1.1135.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Aug | 0.50% | 0.50% | 0.60% | |

| 06:00 | EUR | German PPI M/M Aug | -0.50% | 0.00% | 0.10% | |

| 06:00 | EUR | German PPI Y/Y Aug | 0.30% | 0.60% | 1.10% | |

| 12:30 | CAD | Retail Sales M/M Jul | 0.40% | 0.00% | ||

| 12:30 | CAD | Retail Sales Ex Auto M/M Jul | 0.20% | 0.90% | ||

| 14:00 | EUR | Eurozone Consumer Confidence Sep A | -7.2 | -7.1 |

{kind=link}