The forex markets are rather mixed today even though stocks are generally in risk averse mode. Sterling regains some strength and takes Euro higher with it. Yet, there is no follow through buying through near term resistance against Dollar and Yen yet. Yen and Dollar turned mixed as markets sentiments stabilize mildly. US-China trade negotiations remain the main driver but there is no clear break through yet. Meanwhile, Canadian Dollar is the weakest one on dovish BoC and poor job data.

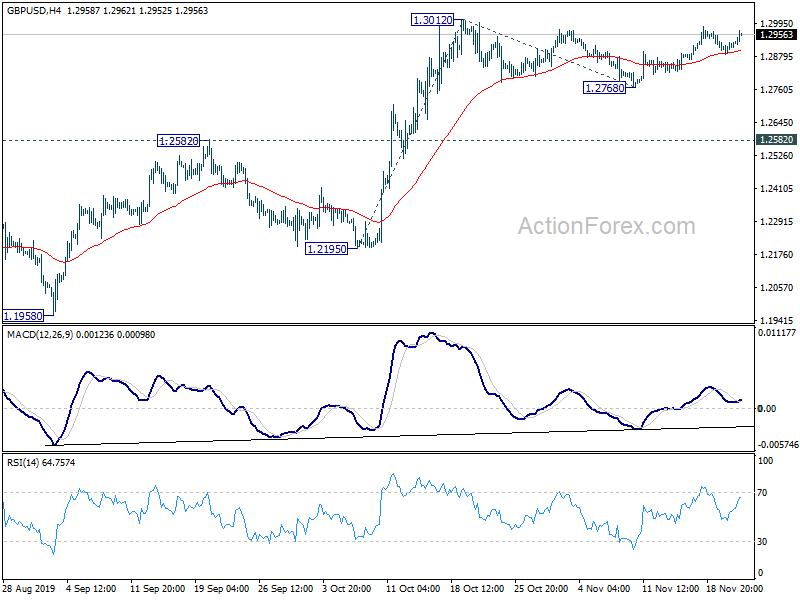

Technically, with today’s rebound, focus is immediately back on 1.3012 resistance in GBP/USD. Decisive break there will resume whole rise form 1.1958. GBP/JPY might also take on 141.50 for resuming rise from 126.54. EUR/USD edged higher through 1.1089 temporary top but quickly retreat. Focus is indeed back on 1.1053 minor support and break will indicate completion of rebound from 1.0989.

In Europe, FTSE is down -0.75%. DAX is down -0.18%. CAC is down -0.18%. German 10-year yield is up 0.0087 at -0.334. Earlier in Asia, Nikkei dropped -0.48%. Hong Kong HSI dropped -1.57%. China Shanghai SSE dropped -0.25%. Singapore Strait Times dropped -1.16%. Japan 10-year JGB yield rose 0.0009 to -0.109.

China working on phase 1 trade deal, inviting US trade officials to visit again

Chinese Ministry of Commerce spokesman Gao Feng reiterated at that China is willing to work with US to address each other’s core concerns to reach the phase one trade deal. And, “this is in line with the interests of both China and the United States, and of the world”. Gao also dismissed “outside rumors” regarding farm purchases and tariff rollbacks a sticking points as “not accurate”.

WSJ reported that China has invited top US trade negotiators for another round of face-to-face meeting in Beijing, preferably before next Thursday’s Thanksgiving holiday. But US have indicated that they’re only willing to travel if China would make clear its commitments on intellectual property protection, forced technology transfers and agricultural purchases.

Separately, on the issue of Hong Kong, China continued to express strong objections to the passage of the Hong Kong Human Rights and Democracy Act. Geng Shuang, spokesman at Foreign Ministry, said “we urge the U.S. side to cease this activity, stop before it’s too late and take measures to prevent these measures from becoming law, stop meddling in Hong Kong’s affairs and China’s affairs”. He added, “If they must insist on going down this wrong path China will take strong counter-measures.”

US initial jobless claims unchanged at 227k, Philadelphia Fed manufacturing index rose to 10.4

US initial jobless claims were unchanged at 227k in the week ending November 16, above expectation of 217k. Four-week moving average of initial claims rose 3.5k to 221k. Continuing claims rose 3k to 1.695m in the week ending November 9. Four-week moving average of continuing claims rose 3k to 1.693m.

Philadelphia Fed Manufacturing Business Outlook Survey diffusion index rose to 10.4 in November, up from 5.6, beat expectation of 7.0. The percentage of firms reporting increases (30 percent) this month exceeded the percentage reporting decreases (20 percent). While the general activity index showed improvement, indicators for new orders, shipments, and employment decreased from last month’s readings.

ECB accounts: Stimulus measures should be allowed more time to unfold effects

In the accounts of ECB’s October 23-24 meeting, it’s noted that incoming information confirmed “the pronounced slowdown in euro area economic growth and a continued shortfall of inflation”. That vindicated the new monetary stimulus package announced back in September’s meeting. “Confidence” was expressed that the package would provide “substantial monetary stimulus”. But the measures “should be allowed more time” to fully unfold their effects.

Looking ahead, a strong call was made for unity of the Governing Council” as it’s important to “form a consensus” to unite behind the commitment on inflation target. And there was call on “other policymakers”, in particular fiscal policy”, “notably of governments with fiscal space, had to play a more prominent role to stabilise economic conditions in view of the weakening economic outlook and the continued prominence of downside risks.

OECD downgrades global GDP forecast, but upgrades Eurozone and China

OECD warned that trade conflict, weak business investment and persistent political uncertainty are weighing on the world economy and raising the risk of long-term stagnation. Global GDP growth for 2020 was revised down by 0.1% to 2.9%, same as this year, lowest annual rate since the financial crisis. That’s also a sharp slowdown from 3.5% back in 2018.

OECD Chief Economist Laurence Boone said: “It would be a mistake to consider these changes as temporary factors that can be addressed with monetary or fiscal policy: they are structural. Without coordination for trade and global taxation, clear policy directions for the energy transition, uncertainty will continue to loom large and damage growth prospects.”

OECD Secretary-General Angel Gurría said: “The alarm bells are ringing loud and clear. Unless governments take decisive action to help boost investment, adapt their economies to the challenges of our time and build an open, fair and rules-based trading system, we are heading for a long-term future of low growth and declining living standards.”

Look at some details:

- Global GDP growth is projected at: 2.9% in 2019 (unchanged). 2.9% in 2020 (down from September’s 3.0%). 3.0% in 2021 (new).

- G20 GDP: 3.1% in 2019 (unchanged). 3.2% in 2020 (unchanged). 3.3% in 2021 (new).

- US GDP: 2.3% in 2019 (down from 2.4%). 2.0% in 2020 (unchanged). 2.0% in 2021 (new).

- Eurozone GDP: 1.2% in 2019 (up from 1.1%). 1.1% in 2020 (up from 1.0%). 1.2% in 2021 (new).

- China GDP: 6.2% in 2019 (up from 6.1%). 5.7% in 2020 (unchanged). 5.5% in 2021 (new).

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2897; (P) 1.2914; (R1) 1.2940; More….

GBP/USD drew support form 4 hour 55 EMA and recovered but stays below 1.3012 resistance. Intraday bias remains neutral first. Decisive break of 1.3012 will resume the whole rise from 1.1958. Further rally should be seen to 61.8% projection of 1.2195 to 1.3012 from 1.2768 at 1.3273 next. For now, outlook will remain bullish as long as 1.2768 support in case of retreat. However, break of 1.2768 will bring deeper fall back to 1.2582 resistance turned support.

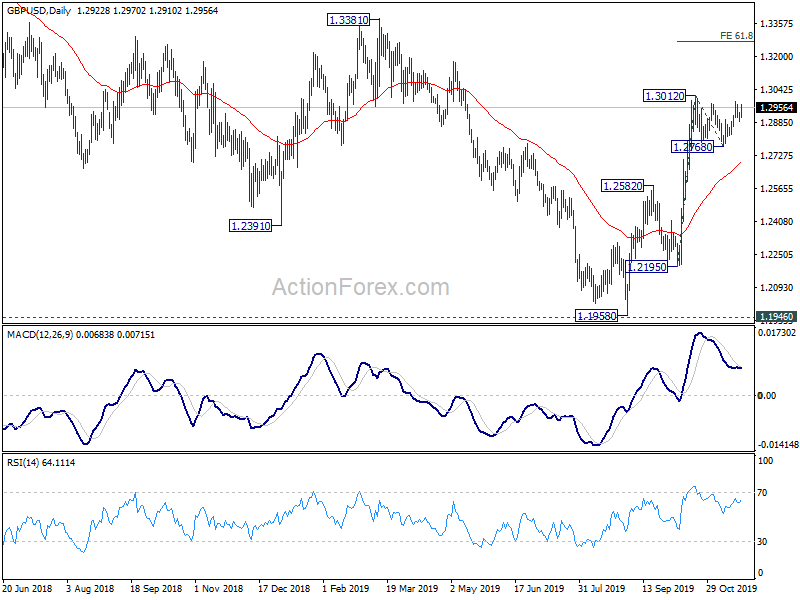

In the bigger picture, a medium term bottom was formed at 1.1958, ahead of 1.1946 (2016 low). At this point, rise from 1.1958 is seen as the third leg of consolidation from 1.1946. Further rise would be seen back towards 1.4376 resistance. For now, this will remain the favored case as long as 1.2582 resistance turned support holds. However, firm break of 1.2582 will turn focus back to 1.1946 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 04:30 | JPY | All Industry Activity Index M/M Sep | 1.50% | 1.50% | 0.00% | |

| 09:30 | GBP | Public Sector Net Borrowing (GBP) Oct | 10.5B | 8.5B | 8.7B | |

| 12:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 13:30 | CAD | ADP Employment Change Oct | -22.6K | 53.3K | 28.2K | |

| 13:30 | USD | Initial Jobless Claims (Nov 15) | 227K | 217K | 225K | 227K |

| 13:30 | USD | Philly Fed Manufacturing Index Nov | 10.4 | 7 | 5.6 | |

| 15:00 | USD | Existing Home Sales Oct | 5.50M | 5.38M | ||

| 15:00 | EUR | Eurozone Consumer Confidence Nov P | -7 | -8 | ||

| 15:30 | USD | Natural Gas Storage | -86B | 3B |

{kind=link}