Yen and Dollar trade mildly lower in Asian session today. Hong Kong stocks lead Asian markets higher, as the landslide pro-democracy victory in Sunday’s election would give China more pressure to end the city’s unrest. Meanwhile, New Zealand and Australian Dollars are trading higher on easing risk aversion. Sterling is also lifted by Prime Minister Boris Johnson’s pledged to get Brexit done.

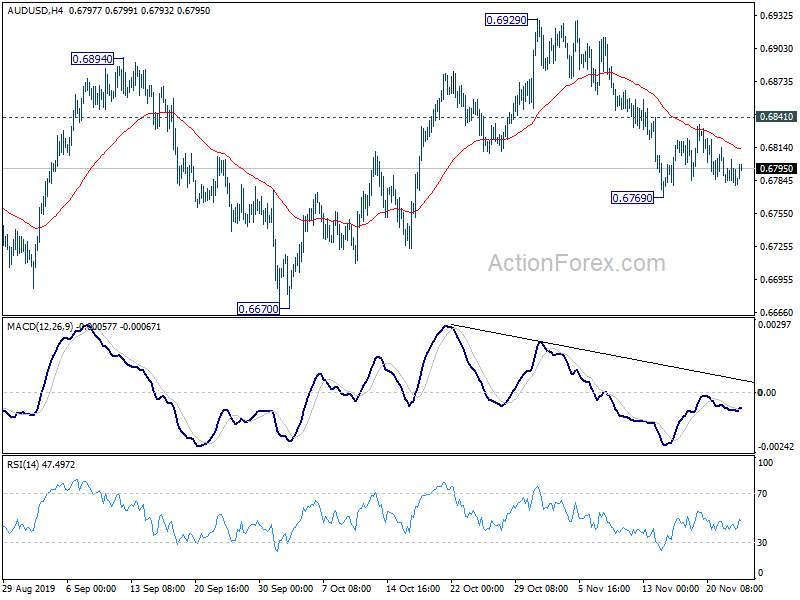

Though, technically, there is no change in overall outlook despite the moves. EUR/USD is on track to take on 1.0989 support. Break will resume fall from 1.1175 to retest 1.0879 low. AUD/USD is extending near term consolidation from 0.6769 but held well below 0.6841 resistance. Further decline is still expected through 0.6769 to 0.6670 low at a later stage. GBP/JPY recovers after hitting 139.36 minor support, but remains vulnerable. Firm break of 139.36 will extend the near term correction towards 135.74 resistance turned support.

In Asia, currently, Nikkei is up 0.66%. Hong Kong HSI is up 1.76%. China Shanghai SSE is up 0.35%. Singapore Strait Times is up 0.30%. Japan 10-year JGB yield is down -0.0072 at -0.087.

Hong Kong stocks lead Asia higher after pro-democracy voters score landslide victory

Hong Kong stocks lead Asian markets generally higher in reaction to the results of Sunday’s district council elections. While the district councils have few real powers, the elections are seen as a referendum on the current unrest, and a confidence vote on the government.

The ballot saw record turnout of 71% with 2.94 million people casting their votes. Pro-democracy candidates won 388 of 446 seats, i.e., near 87%. That’s a huge jump from 125 seats they won back in 2015. On the other hand, the pro-Beijing camp won only 58 seats, down from 299 in 2015.

The elections results should put extra pressure on the Chinese and Hong Kong government to answer the five demands of the protesters. The government will have “no excuse” not to appoint a commission of inquiry on all that happened regarding the extradition bill, including police brutality. Such development would offer some hope for ending the near six month unrest in the city.

US still hoping to get phase 1 trade deal with China done by end of year

There are increasing speculations that the completion of the phase one US-China trade deal would slide into next year. China is said to be refraining concrete commitment on farm purchases, while pushing for more extensive tariffs rollbacks. At the same time, tensions between the two countries increased due to unrest in Hong Kong.

US national security adviser Robert O’Brien said over the weekend “We were hoping to have [a phase one] deal done by the end of the year. I still think that’s possible”. Though, he also emphasized, “at the same time, we’re not going to turn a blind eye to what’s happening in Hong Kong or what’s happening in the South China Sea, or other areas of the world where we’re concerned about China’s activity.”

Meanwhile, Reuters reported that the “ambitious” phase two deal looks increasing less likely for now. An unnamed Chinese office was quoted saying that “It’s Trump who wants to sign these deals, not us. We can wait.” China might want to drag on with phase two negotiations to see if Trump could win a second term in next year’s election.

Sterling recovers as Johnson pledges to get Brexit done

Sterling recovers mildly after UK Prime Minister Boris Johnson’s fresh Brexit promise. Launching his election manifesto in the central English town of Telford, he said “Get Brexit done and we shall see a pent up tidal wave of investment into this country. Get Brexit done and we can focus our hearts and our minds on the priorities of the British people.”

UK is heading to snap election on December 12, Johnson is targeting to bring the Brexit deal back to the parliament before Christmas. He also pledged, “we will not extend the implementation period beyond December 2020”.

A relatively light week ahead

US durable goods orders, consumer confidence, GDP revision and PCE inflation will be the major focuses in a relatively light calendar. Eurozone CPI flash will also be watched, with Germany Ifo business climate too. Canadian dollar has been a rather volatile currency recently and will look into GDP data for next move. Down under, New Zealand retail sales, trade balance and Australia private capital expenditure will be the main focuses.

Here are some highlights for the week:

- Monday: German Ifo business climate; UK CBI realized sales; Canada wholesale sales.

- Tuesday: New Zealand retail sales; Japan corporate service price; Germany Gfk consumer climate; UK BBA mortgage approvals; US goods trade balance, house price indices, wholesale inventories, consumer confidence, new home sales.

- Wednesday: New Zealand trade balance; Australia construction work down; Germany import prices; US durable goods orders, GDP, jobless claims, Chicago PMI; personal income and spending. Fed’s Beige Book.

- Thursday: Japan retail sales; New Zealand ANZ business confidence; Australia private capital expenditure; Swiss GDP; Germany CPI; Eurozone M3 money supply; Canada current account.

- Friday: New Zealand building permits; Japan Tokyo CPI core, unemployment rate, industrial production , consumer confidence, housing starts; Germany retail sales, unemployment; Swiss KOF economic barometer; UK M4 money supply; Eurozone CPI flash, unemployment rate; Canada GDP, IPPI and RMPI.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6777; (P) 0.6790; (R1) 0.6799; More…

Intraday bias in AUD/USD remains neutral as consolidation from 0.6769 temporary low is extending. Upside should be limited by 0.6841 resistance to bring fall resumption. As noted before, corrective rise from 0.6670 should have completed at 0.6929. Break of 0.6769 will extend the fall from 0.6929 to retest 0.6670 low. However, break of 0.6841 will turn bias back to the upside for 0.6929 resistance instead.

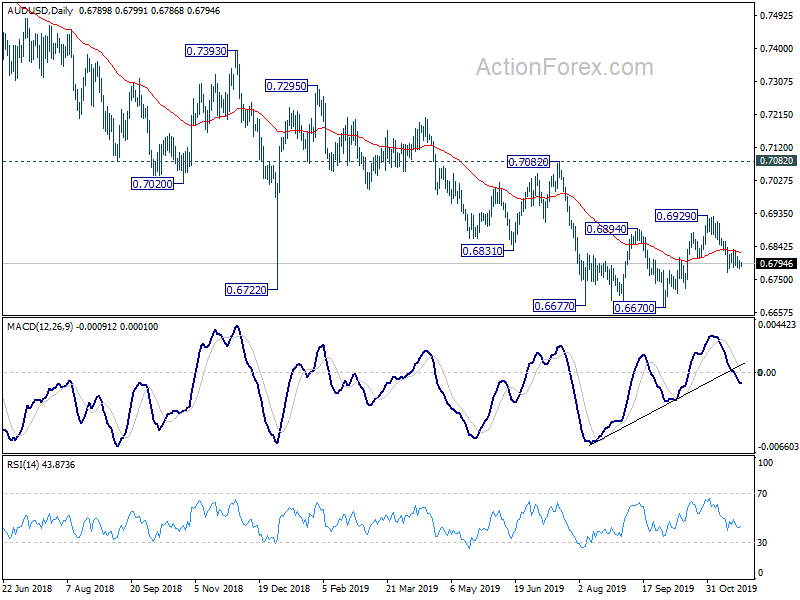

In the bigger picture, with 0.7082 resistance intact, there is no clear confirmation of trend reversal yet. That is, down trend from 0.8135 (2018 high) is still expect to continue to 0.6008 (2008 low). However, decisive break of 0.7082 will confirm medium term bottoming and bring stronger rally back to 55 month EMA (now at 0.7529).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 09:00 | EUR | Germany IFO – Business Climate Nov | 95 | 94.6 | ||

| 09:00 | EUR | Germany IFO – Current Assessment Nov | 98 | 97.8 | ||

| 09:00 | EUR | Germany IFO – Expectations Nov | 92.5 | 91.5 | ||

| 11:00 | GBP | CBI Realized Sales Nov | -10 | -10 | ||

| 13:30 | CAD | Wholesale Sales M/M Sep | -1.20% |

{kind=link}