Dollar trades generally higher today as supported by better than expected economic data, in particular, durable goods orders. Though, Sterling is so far even stronger, as consolidations extend. On the other hand, Euro is the worst performing one, followed by Swiss Franc. For the week so far, the Pound is also the strongest while Yen is the weakest on strong risk appetite.

Technically, the bullish outlook in USD/CHF remains unchanged. Consolidation from 1.0027 should have completed at 0.9868 and further rise should be seen back to 1.0027. Meanwhile, EUR/USD edges lower and is eyeing 1.0989 support. Break will resume the fall from 1.1175 to retest 1.0879 low. While Sterling strengthen’s today, GBP/USD, EUR/GBP and GBP/JPY are staying in sideway trading, awaiting breakout.

In Europe, FTSE is currently up 0.48%. DAX is up 0.27%. CAC is down -0.04%. German 10-year yield is up 0.0068 at -0.364. Earlier in Asia, Nikkei rose 0.28%. Hong Kong HSI rose 0.15%. China Shanghai SSE dropped -0.13%. Singapore Strait Times rose 0.24%. Japan 10-year JGB yield dropped -0.0115 to -0.110.

US durable goods orders rose 0.6%, ex-transport orders rose 0.6%

US durable goods orders rose 0.6% to USD 248.7b in October, well above expectation of -0.5% contraction. ex-transport orders rose 0.6%, also above expectation of 0.2%. Excluding defense, new orders increased 0.1%.

Initial jobless claims dropped -15k to 213k in the week ending November 23, better than expectation of 223k. Four-week moving average of initial claims dropped -1.5k to 219.75k. Continuing claims dropped -57k to 1.640m in the week ending November 16. Four-week moving average of continuing claims dropped -13k to 1.681m.

According to the second estimate, GDP grew 2.1% annualized, revised up from first estimate of 1.9%. With the second estimate for the third quarter, upward revisions to private inventory investment, nonresidential fixed investment, and personal consumption expenditures (PCE) were partially offset by a downward revision to state and local government spending.

Lagarde: ECB tasked to ensure Euro is safe and stable

ECB President Christine Lagarde said in a speech that the existence of Euro is to secure that trust in money so that people can focus on what really matters to them. And that’s the reason why ECB’s mandate and objectives reflect the well-known “functions of money”. Policy makers are tasked to “ensure that euro is safe and stable”.

The Euro also serves as the “most tangible symbol of European integration”, and “bears witness to the degree of integration we have achieved.” Support in the Euro is there with “76% of our citizens are now in favour of the single currency”. Though, she also warned that “trust takes years to build, seconds to break and forever to repair”.

BoJ Sakurai: Increasing need to be mindful of side-effect of low-rate policy

BoJ board member Makoto Sakurai, warned in a speech, “in guiding monetary policy, there’s an increasing need to be mindful of the side-effect of continuing our low-rate policy such as that on Japan’s banking system.”

“If there’s a crisis that could disrupt Japan’s financial system,” he noted, “a bold policy response is necessary”. However, “if the overseas slowdown driven by trade woes is moderate, and the speed at which it affects Japan’s economy is slow, we have room to scrutinise economic indicators in deciding on policy”.

He added, “the next half-year is when we need to carefully scrutinise economic developments”, including the impact of sales tax hike and global slowdown.

New Zealand trade deficit narrowed slightly to NZD 1B

New Zealand goods exports rose 4.3% yoy to NZD 5.0B in October. Goods exports dropped -1.4% yoy to NZD 6.0B. Trade deficit narrowed slightly to NZD 1.013B, down from NZD -1.319B, in line with expectations.

Exports to China rose NZD 279m to NZD 1.5B, led by rises in milk powder, lamb and beef. Exports to Australia was little changed at NZD 791m. Imports from China dropped NZD -100m to NZD 1.4B. Imports from EU dropped slightly by NZD-9.9m to NZD 965m.

From Australia, construction work done dropped -0.4% in Q3, better than expectation of -1.0%.

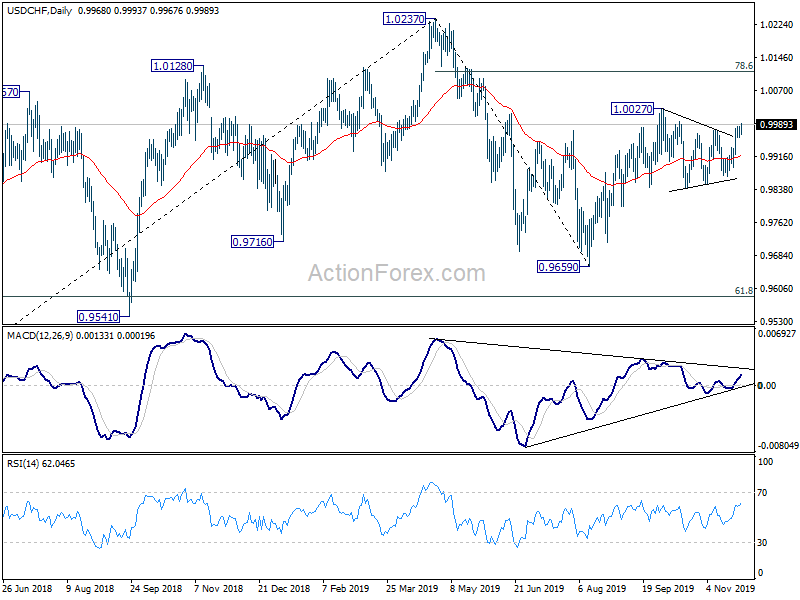

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9962; (P) 0.9975; (R1) 0.9986; More…

USD/CHF’s rise continues today and intraday bias remains on the upside at this point. Consolidation from 1.0027 should have completed at 0.9869. Further rise should be seen to retest 1.0027 first. Break will resume whole rise from 0.9659 to 78.6% retracement of 1.0237 to 0.9659 at 1.0113. On the downside, however, break of 0.9960 minor support will turn bias to the downside to extend the consolidation with another falling leg.

In the bigger picture, medium term outlook remains neutral as USD/CHF is staying in range of 0.9659/1.0237. In any case, decisive break of 1.0237 is needed to indicate up trend resumption. Otherwise, more sideway trading would be seen with risk of another fall. Meanwhile, break of 0.9695 support will target 0.9541 support instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 20:00 | NZD | RBNZ Financial Stability Report | ||||

| 21:45 | NZD | Trade Balance (NZD) Oct | -1013M | -1000M | -1242M | -1319M |

| 00:01 | GBP | BRC Shop Price Index Y/Y Oct | -0.50% | -0.40% | ||

| 00:30 | AUD | Construction Work Done Q3 | -0.40% | -1.00% | -3.80% | -2.80% |

| 07:00 | EUR | Germany Import Price Index M/M Oct | -0.10% | -0.20% | 0.60% | |

| 09:00 | CHF | ZEW Expectations Nov | -3.9 | -30.5 | ||

| 13:30 | USD | Initial Jobless Claims (Nov 22) | 213 K | 223K | 227K | 228 K |

| 13:30 | USD | GDP Annualized Q3 P | 2.10% | 1.90% | 1.90% | |

| 13:30 | USD | GDP Price Index Q3 P | 1.80% | 1.70% | 1.70% | |

| 13:30 | USD | Durable Goods Orders Oct | 0.60% | -0.50% | -1.20% | |

| 13:30 | USD | Durable Goods Orders ex Transportation Oct | 0.60% | 0.20% | -0.40% | |

| 15:00 | USD | Personal Income M/M Oct | 0.30% | 0.30% | ||

| 15:00 | USD | Personal Spending Oct | 0.30% | 0.20% | ||

| 15:00 | USD | PCE – Price Index M/M Oct | 0.10% | 0.00% | ||

| 15:00 | USD | PCE – Price Index Y/Y Oct | 1.20% | 1.30% | ||

| 15:00 | USD | Core PCE – Price Index M/M Oct | 0.20% | 0.00% | ||

| 15:00 | USD | Core PCE – Price Index Y/Y Oct | 1.70% | 1.70% | ||

| 15:00 | USD | Pending Home Sales M/M Oct | 0.20% | 1.50% | ||

| 15:30 | USD | Natural Gas Storage | -94B | |||

| 16:00 | USD | Crude Oil Inventories | 1.4M | |||

| 19:00 | USD | Fed’s Beige Book |

{kind=link}