Yen trades broadly lower while Australian and New Zealand Dollars strengthen in Asia. Stock markets are cheering better than expected manufacturing data from China. Nikkei leads the way higher but gains in Hong Kong and Shanghai are limited. Yen is also additionally pressured by extended rebound in JGB yields. More manufacturing data will be featured today, in particular US ISM manufacturing index, which could further shape risk sentiments for December.

Technically, USD/JPY’s rally resumed after brief consolidations and is on track to 110.50 projection level. GBP/JPY also stays firm as rise form 126.54 is targeting trend line resistance at 143.65. A question for the today is whether EUR/JPY would break 121.46 resistance to align the bullish outlook with other Yen crosses. Meanwhile, Dollar’s rally attempt somewhat lost momentum, as seen in EUR/UAD and AUD/USD. Both pair would be watched to gauge underlying strength of the greenback.

In Asia, Nikkei is currently up 1.11%. Hong Kong HSI is up 0.48%. China Shanghai SSE is up 0.35%. Singapore Strait Times is up 0.19%. Japan 10-year JGB yield is up 0.0214 at -0.060.

China Caixin Manufacturing PMI rose to 51.8, manufacturing investment lingering near a recent bottom

China Caixin Manufacturing PMI rose slightly to 51.8 in November, up from 51.7 and beat expectation of 51.4. Markit noted there were solid increases in output and new business. Employment was broadly stable while inflationary pressures remained weak.

Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group said: “Currently, manufacturing investment may be lingering near a recent bottom. A low inventory level has lasted for a long time. If trade negotiations between China and the U.S. can progress in the next phase and business confidence can be repaired effectively, manufacturing production and investment is likely to see a solid improvement.”

Released over the weekend, the official PMI Manufacturing rose to 50.2 in November, up from 49.3 and beat expectation of 49.5. PMI Non-Manufacturing rose to 54.4, up from 52.8 and beat expectation of 53.1.

Japan PMI manufacturing finalized 48.9, seventh month of contraction

Japan PMI Manufacturing was finalized at 48.9 in November, up from 48.4 in October. That’s the seven straight month of sub-50 reading, signalling a continuation of the downturn in the manufacturing sector. Jibun Bank noted that solid decline in new orders led to further output cutbacks. Economic weakness across Asia hit exports. Selling charges also decreased for the sixth month running.

Joe Hayes, Economist at IHS Markit, said Japan’s manufacturing sector “remains firmly stuck in contraction”. In particular, “export orders dropped at the fastest rate since mid-year amid reports of demand weakness at key trade destinations, namely China.” Also, signs of how deeply-rooted this manufacturing downturn in Japan has become were seen in other survey data.

Also fro Japan, capital spending rose 7.1% in Q3, better than expectation of 5.1%.

Australia AiG manufacturing index dropped to 48.1, lowest since 2016

Economic data released from Australia are generally disappointing. AiG Performance Index dropped to 48.1 in November, down from 51.6. That’s also the lowest level since August 2016, and indicates contraction in the sector. AiG said: “. The faster rate of contraction of the new orders index in November suggests a weak Christmas period ahead for Australian manufacturers. However, some manufacturing sectors are reporting better conditions than others, with manufacturers in the large food and beverage sector continuing to report buoyant conditions.”

Also released, company gross operating profits dropped -0.8% qoq in Q3 versus expectation of 1.0% qoq rise. Building permits dropped -8.1% mom in October, versus expectation of -1.0% mom. TD securities inflation rose 0.0% mom in November.

New Zealand Treasury: GDP growth likely falls below budget forecasts

In its Monthly Economic Indicators report, New Zealand Treasury Department noted that November data were “fair mixed” with some pointing to “further slowing in GDP growth”. Others indicated growth may be “levelling out”. On balance, “weaker-than-forecast investment and services exports are likely to see overall New Zealand GDP growth fall below Budget forecasts”

It’s also noted that news flow surrounding trade tensions “continues to seesaw”. But “prospects of a US-China trade agreement have generally supported sentiment over the last month”.

Also from New Zealand, terms of trade index rose 1.9% in Q3, above expectation of 1.1%.

A big week ahead for USD, CAD and AUD

It’s a big week ahead with lots of important events. Two central banks will meet, RBA and BoC and both are widely expected to stand pat. Focuses will be on their guidance on future policy changes. In particular, RBA is generally expected to cut interest rates against in February. BoC is also edging closer to policy easing after last dovish statement.

Economic data from both countries are also heavy weight, including GDP, retail sales and trade balance from Australia. Canada employment and trade balance will also be featured.

In the US, major focuses will be on ISM indices and non-farm payrolls. There is practically no chance of any policy adjustment by Fed again in December. But next year’s rate path will be heavily dependent on incoming data and trade negotiations with China.

Here are some highlights for the week:

- Monday: Australia AiG manufacturing index, building approvals, company operating profits; New Zealand terms of trade index; Japan capital spending, PMI manufacturing final; China Caixin PMI manufacturing; Swiss retail sales, PMI manufacturing; Eurozone PMI manufacturing final; UK PMI manufacturing final; Canada PMI manufacturing; US ISM manufacturing, construction spending.

- Tuesday: Japan monetary base; Australia current account, RBA rate decision; Swiss CPI; UK PMI construction; Eurozone PPI.

- Wednesday: Australia GDP, AiG services index; Eurozone PMI services final; UK PMI services final; US ADP employment, ISM non-manufacturing; BoC rate decision.

- Thursday: Australia retail sales, trade balance; Germany factory orders; Eurozone GDP revision, retail sales, employment change; Canada trade balance, Ivey PMI; US trade balance, factory orders.

- Friday: Australia AiG construction index; Japan average cash earnings, household spending, leading indicators; Germany industrial production; Swiss foreign currency reserves. Canada employment; US non-farm payroll.

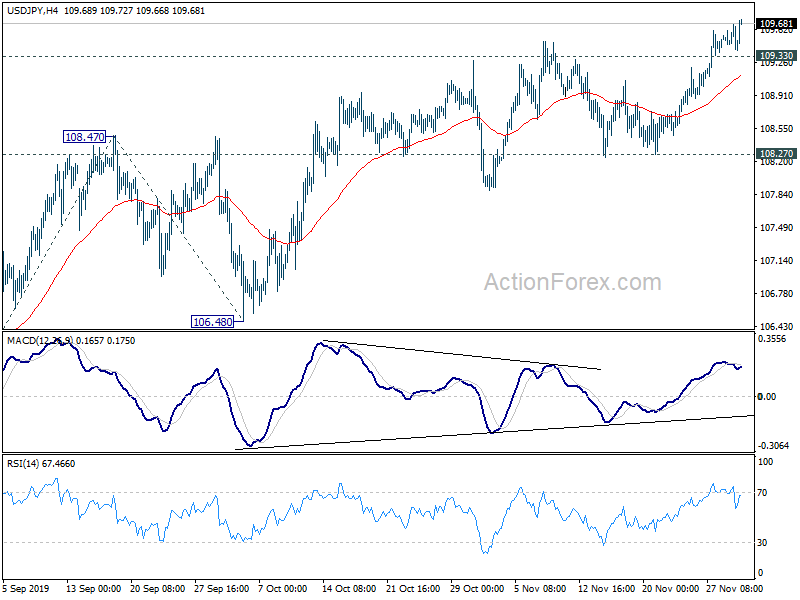

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.38; (P) 109.53; (R1) 109.65; More..

USD/JPY’s rally resumed after brief consolidations and intraday bias is back on the upside. Current rise from 104.45 is in progress for 100% projection of 104.45 to 108.47 from 106.48 at 110.50. Break will target long term channel resistance at 111.78 next. On the downside, below 109.33 minor support will turn intraday bias neutral and bring consolidations first. In this case, downside of retreat should be contained above 108.27 support to bring rise resumption.

In the bigger picture, strong support was seen from 104.62 again. Yet, there is no confirmation of medium term reversal. Corrective decline from 118.65 (Dec. 2016) could still extend lower. But in that case, we’d expect strong support above 98.97 (2016 low) to contain downside to bring rebound. Meanwhile, on the upside, break of 112.40 key resistance will be a strong sign of start of medium term up trend.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Mfg Index Nov | 48.1 | 51.6 | ||

| 21:45 | NZD | Terms of Trade Index Q3 | 1.90% | 1.10% | 1.60% | 1.40% |

| 23:50 | JPY | Capital Spending Q3 | 7.10% | 5.10% | 1.90% | |

| 00:00 | AUD | TD Securities Inflation M/M Nov | 0.00% | 0.10% | ||

| 00:30 | AUD | Building Permits M/M Oct | -8.10% | -1.00% | 7.60% | 7.20% |

| 00:30 | AUD | Company Gross Operating Profits Q/Q Q3 | -0.80% | 1.00% | 4.50% | 4.80% |

| 00:30 | JPY | Jibun Bank Manufacturing PMI Nov F | 48.9 | 48.6 | 48.6 | |

| 01:45 | CNY | Caixin Manufacturing PMI Nov | 51.8 | 51.4 | 51.7 | |

| 05:30 | AUD | RBA Commodity Index SDR Y/Y Nov | -4.20% | |||

| 07:30 | CHF | Real Retail Sales Y/Y Oct | 0.80% | 0.90% | ||

| 08:30 | CHF | SVME PMI Nov | 48.8 | 49.4 | ||

| 08:45 | EUR | Italy Manufacturing PMI Nov | 47.5 | 47.7 | ||

| 08:50 | EUR | France Manufacturing PMI Nov F | 51.6 | 51.6 | ||

| 08:55 | EUR | Germany Manufacturing PMI Nov F | 43.8 | 43.8 | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Nov F | 46.6 | 46.6 | ||

| 09:30 | GBP | Manufacturing PMI Nov F | 48.3 | 48.3 | ||

| 14:30 | CAD | Manufacturing PMI Nov | 51.2 | |||

| 14:45 | USD | Manufacturing PMI Nov F | 52.2 | 52.2 | ||

| 15:00 | USD | ISM Manufacturing PMI Nov | 49.4 | 48.3 | ||

| 15:00 | USD | ISM Prices Paid Nov | 47 | 45.5 | ||

| 15:00 | USD | Construction Spending M/M Oct | 0.30% | 0.50% |

{kind=link}