Markets continue to trade in rather subdued manner today, awaiting the key events ahead, including three central bank meetings, trade deal and UK elections. Meanwhile, Euro is trading generally higher, slightly, as supported by improvement in investor confidence. Sterling is also firm but fails to extend earlier gains. On the other hand, Australian and New Zealand Dollars are mildly lower, followed by the greenback.

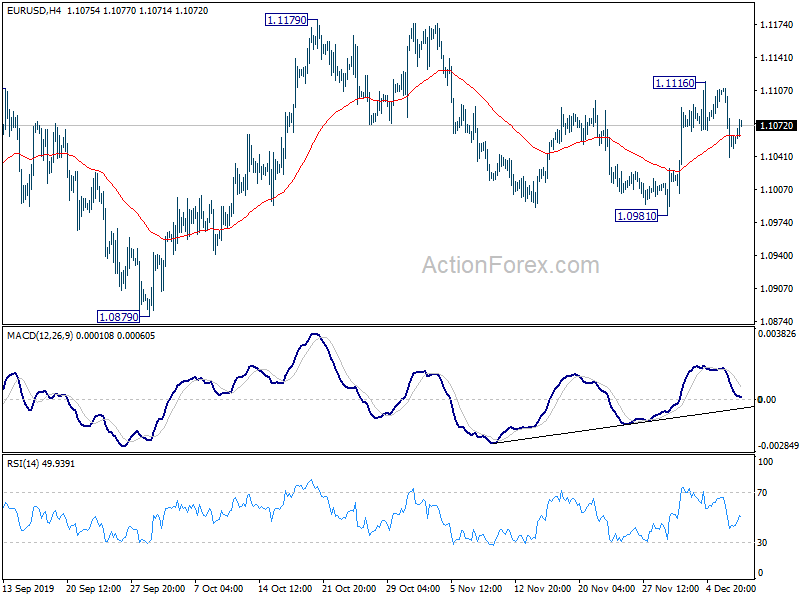

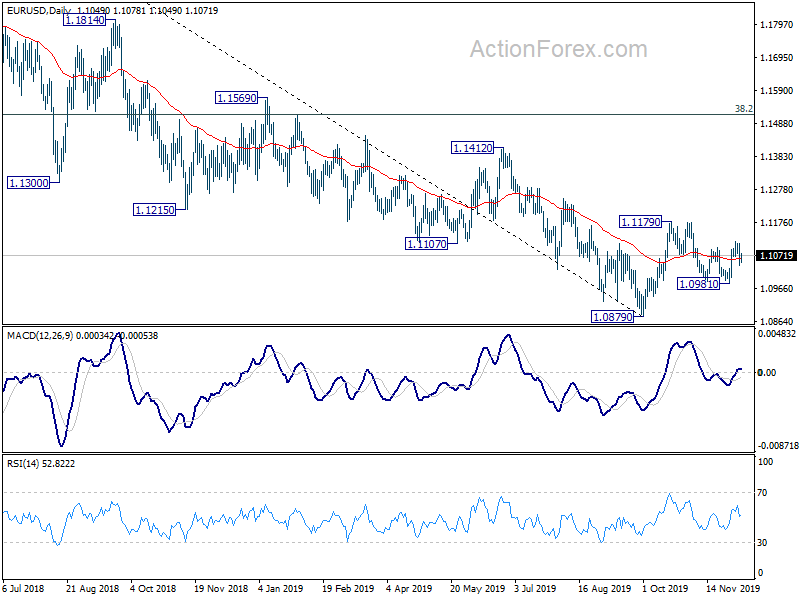

Technically, after last week’s rebound attempt, there is so far no follow through buying in the greenback. USD/CHF, USD/JPY, USD/CAD and AUD/USD are staying in established range. EUR/USD’s pull back is so far contained well above 1.0981 support. Further rise is mildly in favor for the near term. Break of 1.1116 will target a test on 1.1179 resistance next.

In Europe, currently, FTSE is down -0.07%. DAX is down -0.24%. CAC is down -0.49%. German 10-year yield is down -0.0238 at -0.309. Earlier in Asia, Nikkei rose 0.33%. Hong Kong HSI dropped -0.01%. China Shanghai SSE rose 0.08%. Singapore Strait Times dropped -0.47%. Japan 10-year JGB yield rose 0.0121 to -0.005.

Eurozone Sentix confidence rose to 0.7, spectre of recession dispelled

Eurozone Sentix Investor Confidence rose to 0.7 in December, up from -4.5 an beat expectation of -5.4. That’s the highest level since May this year. Current Situation Index rose from -5.5 to -5.0, highest since July. Expectations Index rose from -3.5 to 2.5, highest since March 2018.

Sentix said, “the second improvement in a row may be taken as an indication that the spectre of recession has been dispelled in the Euro zone”. And, more and more investors are convinced that “the worst is over” for the economy. Investors are pinning their hops on an “increase in government spending on government investment.

For Germany, the overall Investor Confidence Index rose from -6.5 to -1.4, highest since June. Current Situation Index rose from -8.3 to -3.3, highest since July. Expectations Index rose from -4.8 to 0.5, highest since February 2018. Sentix said, “As a former world export champion, the country has recently been particularly affected by problems in world trade. Now that a trend reversal has been confirmed – starting with the region Asia ex Japan – this automatically means an easing for the German economy.”

German trade surplus widened to EUR 20.6B, imports stagnate

German expects rose 1.9% yoy to EUR 119.5B in October while imports dropped -0.6% yoy to EUR 98.0. Trade surplus came in at EUR 21.56B. On calendar and seasonally adjusted terms, exports rose 1.2% mom while imports was flat. Trade surplus widened to EUR 20.6B, beat expectation of EUR 19.0B.

According to provisional results of the Deutsche Bundesbank, the current account of the balance of payments showed a surplus of EUR 22.7B. That takes into account the balances of trade in goods including supplementary trade items (EUR 22.5B), services (EUR -4.3B), primary income (EUR 9.0B) and secondary income (EUR -4.5B).

Japan Q3 GDP revised up to 1.8% annualized on capital spending

Japan’s Q3 GDP growth was finalized at 0.4% qoq, revised up from preliminary reading of 0.1% qoq. Annualized rate was revised sharply higher to 1.8%, up from 0.2%. That’s the fourth consecutive quarter of growth despite persistent global headwinds.

Looking at some details, capital spending rose 1.8% qoq, revised up from 0.9% qoq. Private consumption rose 0.5% qoq, revised up from 0.4% qoq. Domestic demanded contributed to 0.6% qoq GDP growth while net exports subtracted -0.2% qoq.

Also from Japan, bank lending rose 2.1% yoy in November, above expectation of 1.9% mom. Current account surplus widened to JPY 1.73T, slightly below expectation of JPY 1.74T.

China’s export shrank for 4th straight month in Nov, trade surplus narrowed to USD 38.7B

In November, in USD terms, China’s exports dropped -1.1% yoy, below expectation of 1.0% yoy growth. Imports rose 0.3% yoy versus expectation of -1.8% yoy fall. Trade surplus narrowed to USD 38.7B, down from USD 42.8B and missed expectation of USD 44.5B.

As the 17-month trade war with US drags on, it was indeed the fourth consecutive of contraction in exports. On the other hand, the surprised growth in imports argued that the government’s stimulus might be in play in supporting domestic demand.

The upcoming Sunday, is the “natural deadline” for the phase one US-China trade deal. If nothing happens between now an then, a new round of tariffs on USD 156B of essentially all untaxed Chinese imports will take effect. US President Donald Trump said last week that talks were “moving right along”. Yet, he didn’t object to the idea of waiting until after 2020 election to seal the deal.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1030; (P) 1.1070; (R1) 1.1100; More…

EUR/USD recovers mildly today but stays in range of 1.0981/1116. Intraday bias remains neutral first. On the upside, above 1.1116 will resume the rise from 1.0981 to 1.1179 resistance. That will also revive the case that correction from 1.1179 has completed and rise from 1.0879 is ready to resume. On the downside, break of 1.0981 will resume the decline from 1.1179 for retesting 1.0879 low instead.

In the bigger picture, rebound from 1.0879 is seen as a corrective move first. In case of another rise, upside should be limited by 38.2% retracement of 1.2555 to 1.0879 at 1.1519. And, down trend from 1.2555 (2018 high) would resume at a later stage. However, sustained break of 1.1519 will dampen this bearish view and bring stronger rise to 61.8% retracement at 1.1915 next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 07:00 | CNY | Trade Balance (USD) Nov | 38.7B | 44.5B | 42.8B | |

| 07:00 | CNY | Exports (USD) Y/Y Nov | -1.10% | 1.00% | -0.90% | |

| 07:00 | CNY | Imports (USD) Y/Y Nov | 0.30% | -1.80% | -6.40% | |

| 07:00 | CNY | Trade Balance (CNY) Nov | 274B | 300B | 301B | |

| 07:00 | CNY | Exports (CNY) Y/Y Nov | 1.30% | 3.10% | 2.10% | |

| 07:00 | CNY | Imports (CNY) Y/Y Nov | 2.50% | -0.90% | -3.50% | -3.30% |

| 21:45 | NZD | Manufacturing Sales Q3 | 0.90% | -0.80% | -0.70% | -0.50% |

| 23:50 | JPY | Bank Lending Y/Y Nov | 2.10% | 1.90% | 2.00% | |

| 23:50 | JPY | GDP Q/Q Q3 | 0.40% | 0.20% | 0.10% | |

| 23:50 | JPY | GDP Deflator Y/Y Q3 | 0.60% | 0.60% | 0.60% | |

| 23:50 | JPY | GDP Annualized Q3 | 1.80% | 0.70% | 0.20% | |

| 23:50 | JPY | Current Account (JPY) Oct | 1.73T | 1.74T | 1.49T | |

| 06:45 | CHF | Unemployment Rate Nov | 2.30% | 2.30% | 2.30% | |

| 07:00 | EUR | Germany Trade Balance (EUR) Oct | 20.6B | 19.0B | 19.2B | |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Dec | 0.7 | -5.4 | -4.5 | |

| 13:15 | CAD | Housing Starts Nov | 201K | 200K | 202K | 201K |

| 13:30 | CAD | Building Permits M/M Oct | -1.50% | 3.50% | -6.50% | -5.90% |

{kind=link}