Canadian Dollar drops sharply in early US session after much weaker than expected retail sales data. Euro and Swiss Franc are also under some selling pressure. On the other hand, Sterling is paring some losses ahead of weekly close while Australian Dollar is generally firm. Over the week, Swiss Franc remains the strongest one for now, followed by Aussie. Sterling is the weakest, followed by Euro.

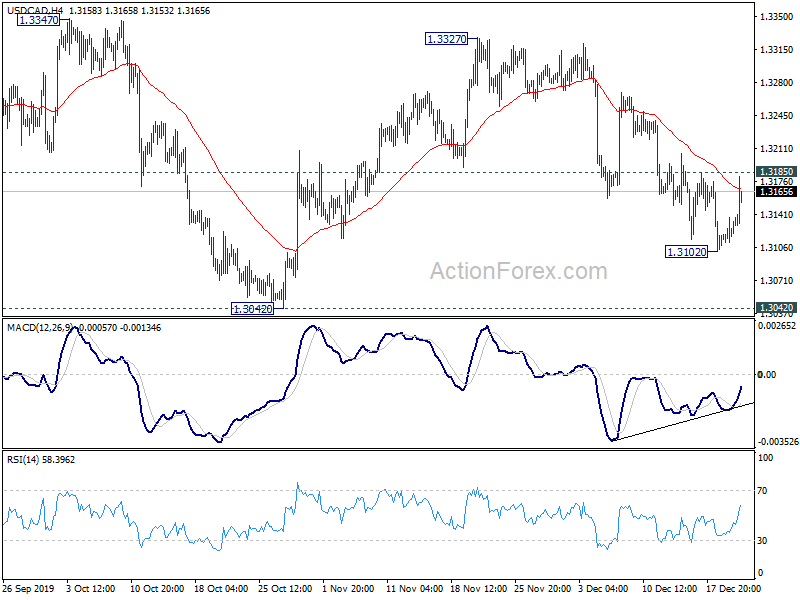

Technically, immediate focus is now on 1.3185 minor resistance in USD/CAD. Break will suggest that the choppy fall from 1.3327 has completed and turn bias back to the upside. EUR/AUD could have a take on 1.6063 support soon. Break will turn focus back to 1.5976, or even further to 1.5894.

In Europe, currently, FTSE is up 0.08%. DAX is up 0.57%. CAC is up 0.61%. German 10-year yield is up -0.0011 at -0.235. Earlier in Asia, Nikkei dropped -0.20%. Hong Kong HSI rose 0.25%. China Shanghai SSE dropped -0.40%. Singapore Strait Times rose 0.15%. Japan 10-year JGB yield rose 0.0173 to 0.012, turned positive.

Canada retail sales dropped -1.2%, ex-auto sales dropped -0.5%

Canada retail sales dropped -1.2% mom to 50.9B in October, well below expectation of 0.1% mom rise. Ex-auto sales dropped -0.5% mom, also missed expectation of 0.2% mom. Lower sales were reported in 8 of 11 subsectors, representing 81% of retail trade. Also, sales were down in six provinces. Retail sales dropped -2.0% in Ontario, -1.7% in Quebec, -0.9% in British Columbia.

US Q3 GDP growth finalized at 2.1%, core PCE at 2.1%

US Q3 GDP growth was finalized at 2.1% annual rate, unrevised, slightly up from Q2’s 2.0%. Current-dollar GDP grew 3.8% annualized. PCE price index was finalized at 1.5% yoy, core PCE at 2.1%.

Former BoE Deputy Governor Bailey named to replace Carney

The UK Government named Andrew Bailey as the next BoE Governor, taking over from Mark Carney starting March 16. Bailey is currently the CEO of the Financial Conduct Authority. He worked at the BoE for 30 years, last serving as Deputy Governor from April 2013 to July 2016. On the appointment, he said he’s honored to take over “particularly at such a critical time for the nation as we leave the European Union.”

Finance Minister Sajid Javid said Bailey would serve an eight-year term. He added, “Andrew was the stand-out candidate in a competitive field. He is the right person to lead the Bank as we forge a new future outside the EU and level-up opportunity across the country.”

UK Q3 GDP finalized at 0.4%, upward revisions to all three main industries

UK Q3 GDP growth was finalized at 0.4% qoq, revised up from 0.3% qoq. There were upward revisions to the output of all three main industries. Services grew 0.37%. Production grew a mere 0.01%. Construction grew 0.07%. Agriculture, forestry and fishing were flat. Also from UK, current account deficit narrowed to GBP -15.9B in Q3. Public sector net borrowing dropped to GBP 4.9B in November.

UK Gfk consumer confidence rose to -11, robust increase in economic confidence

UK Gfk Consumer Confidence rose to -11 in December, up from -14. In particular, index for General Economic Situation over the last 12 months improved 3 pts to -31. Index for General Economic Situation over the next 12 months improved 7 pts to -27.

Joe Staton, Client Strategy Director at GfK, said: “We haven’t seen such a robust increase in confidence about our economic future since the summer of 2016. Despite official warning signs about the flat-lining of Britain’s economy, we know that record high employment and below target levels of inflation are helping to boost consumers’ expectations for the year ahead.

German Gfk consumer confidence dropped to -0.1, economic expectations tumbled

German Gfk consumer confidence dropped -0.1 to 9.6 in January. Economic expectations dropped sharply to -4.4, down from 1.7. Gfk said that ” impression among consumers that the German economy will weaken significantly has been reinforced.”. Also, “The trade conflicts between the US and China, on the one hand, and the US and the EU, on the other, continue to smolder, hanging like a sword of Damocles over Germany, a nation highly dependent on exports”.

Japan national CPI core ticked up to 0.5%

Japan national CPI core (ex-fresh food), accelerated to 0.5% yoy in November, ticked up from 0.4% yoy. However, taking away the effect of sales tax hike, started in October, core inflation came in at just 0.2% yoy. All item CPI rose from 0.2% yoy to 0.5% yoy. CPI core-core (ex-fresh food and energy) rose from 0.7% yoy to 0.8% yoy.

While it’s the 35th straight month of core price increases, it remained well below BoJ’s 2% target. An official from the Ministry of Internal Affairs and Communications said, “although at a slower pace, the index continues to rise, so there is no change in our view that the prices are rising moderately.”

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3109; (P) 1.3123; (R1) 1.3139; More….

A temporary low is formed at 1.3102 in USD/CAD and intraday bias is turned neutral first. On the upside, considering bullish convergence condition in 4 hour MACD, break of 1.3185 resistance will indicate short term bottoming. Fall from 1.3327 could have completed. Intraday bias will be turned back to the upside for 1.3327 resistance. on the downside, break of 1.3102 will target 1.3042 key support next.

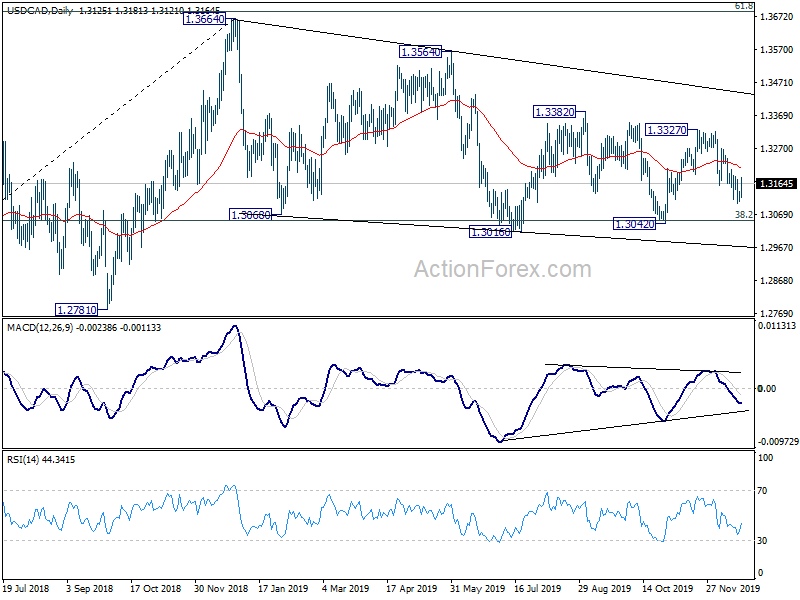

In the bigger picture, 38.2% retracement of 1.2061 to 1.364 at 1.3052 remains intact. Medium term rise from 1.2061 low is in favor to resume sooner or later. Firm break of 61.8% retracement of 1.4689 (2016 high) to 1.2061 at 1.3685 will confirm and target 1.4689 high. However, sustained break of 1.3052 will confirm completion of up trend from 1.2061 (2017 low). Further fall should be seen to 61.8% retracement at 1.2673 next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Nov | 0.50% | 0.50% | 0.40% | |

| 00:01 | GBP | GfK Consumer Confidence Dec | -11 | -14 | -14 | |

| 07:00 | EUR | Germany Gfk Consumer Confidence Jan | 9.6 | 9.7 | 9.7 | |

| 07:45 | EUR | France Consumer Spending M/M Nov | 0.10% | 0.30% | 0.20% | |

| 09:00 | EUR | Current Account (EUR) Oct | 32.4B | 23.6B | 28.2B | |

| 09:30 | GBP | GDP Q/Q Q3 F | 0.40% | 0.30% | 0.30% | |

| 09:30 | GBP | Current Account (GBP) Q3 | -15.9B | -15.5B | -25.2B | -24.2B |

| 09:30 | GBP | Public Sector Net Borrowing (GBP) Nov | 4.9B | 5.2B | 10.5B | |

| 12:00 | GBP | BoE Quarterly Bulletin Q4 | ||||

| 13:30 | CAD | New Housing Price Index M/M Oct | -0.10% | 0.00% | 0.20% | |

| 13:30 | CAD | Retail Sales M/M Oct | -1.20% | 0.10% | -0.10% | |

| 13:30 | CAD | Retail Sales ex Autos M/M Oct | -0.50% | 0.20% | 0.20% | |

| 13:30 | USD | GDP Annualized Q3 F | 2.10% | 2.10% | 2.10% | |

| 13:30 | USD | GDP Price Index Q3 F | 1.80% | 1.70% | 1.70% | |

| 15:00 | USD | Personal Income M/M Nov | 0.30% | 0.00% | ||

| 15:00 | USD | Personal Spending M/M Nov | 0.40% | 0.30% | ||

| 15:00 | USD | PCE Price Index M/M Nov | 0.10% | 0.20% | ||

| 15:00 | USD | PCE Price Index Y/Y Nov | 1.30% | 1.30% | ||

| 15:00 | USD | Core PCE Price Index M/M Nov | 0.10% | 0.10% | ||

| 15:00 | USD | Core PCE Price Index Y/Y Nov | 1.60% | 1.60% | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Dec F | 99.2 | 99.2 | ||

| 15:00 | EUR | Eurozone Consumer Confidence Dec P | -7 | -7 |

{kind=link}