Dollar and Yen remain the overwhelmingly weakest ones for the week even though risk appetite seems to be taking a breather again. In particular, the greenback suffered steep selling after Euro bulls cheered ECB’s PEPP expansion. The common currency is one of the strongest one this week, just next to Kiwi and Aussie. Non-farm payroll report from the US is the next focus. But it’s unlikely to give Dollar any strength for a rebound.

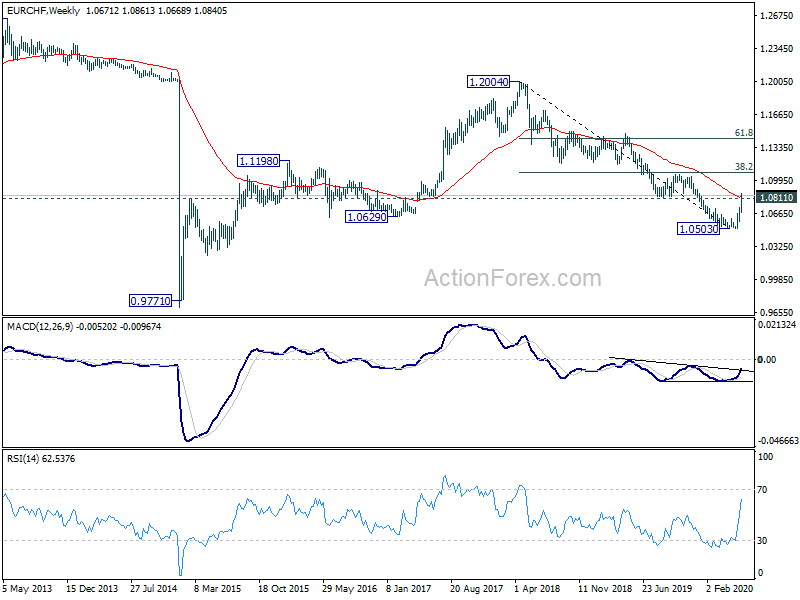

Technically, EUR/CHF’s break of 1.0811 key resistance again is worth a mention. A weekly close above the level, as well 55 week EMA, would be another solid sign of medium term strength in Euro. Further rally in EUR/CHF, towards 1.1059 key cluster resistance, could take Euro higher elsewhere. While commodity currencies have been strong, both Aussie and Canadian are losing some momentum. 0.6856 minor support in AUD/USD and 1.3572 minor resistance in USD/CAD would be watched for sign of a near term pull back

In Asia, currently, Nikkei is up 0.08%. Hong Kong HSI is down -0.03%. China Shanghai SSE is down -0.26%. Singapore Strait Times is up 0.34%. Japan 10-year JGB yield is up 0.009 at 0.039. Overnight, DOW rose 0.05%. S&P 500 dropped -0.34%. NASDAQ dropped -0.69%. 10-year yield rose 0.059 to 0.820.

Dollar index accelerating downward ahead of NFP

US non-farm payrolls report will be a major focus for today. Markets are expecting NFP to show another -8m job less in May. Unemployment rate is expected to jump further up from 14.7% to 19.6%. Other employment data were not too promising. ADP report showed -2.76m contraction in private sector jobs. ISM manufacturing employment improved to 31.8 while non-manufacturing employment rose to 32.1. But both were deep in contraction region. Four-week moving average of initial jobless claims also stayed huge at 2.28m.

Dollar index suffered another round of steep decline this week. Selling accelerated further after ECB announced to expand the PEPP yesterday. Technically, the strong break of 55 week EMA in DXY further affirm the case that whole rise form 88.2 (2018 low) has already completed at 102.99, ahead of 103.82 high (2016 high). Next defend zone is between 94.65 support and long term trend line at around 95.5. We’d look for support from there to bring a near term recovery.

Australia performance of services rose to 31.6, muted optimism from easing restrictions

Australia AiG Performance of Services Index rose to 31.6 in May, up from 27.1. While the data indicates slower pace of contraction, it’s still the second lowest result on record. In trend term, the index dropped -3.4 pts to 30.8, with declines across all services sectors.

AiG also noted, “heavy restrictions on activity in response to the COVID-19 pandemic have taken a large toll on most of Australia’s services industries… The recent easing of restrictions in some locations led to “muted optimism for businesses who responded later in May.”

UK GfK consumer confidence dropped to -36, lowest since 2009

UK GfK Consumer Confidence dropped to -36 in May, down from -34. That’s the lowest level since January 2009, and not far from record low of -39 touched in July 2008.

GfK’s client strategy director Joe Staton said: “with no sign of a rapid V-shaped bounce-back on the cards, consumers remain pessimistic about the state of their finances and the wider economic picture for the year to come”. Meanwhile, “as the lockdown eases, it will be interesting to see just how the consumer appetite for spending returns in a world of socially-distanced shopping and the seismic shift to online retailing.”

Elsewhere

Japan household spending dropped -11.1% yoy in April, versus expectation of -12.8% yoy. Germany factor orders, Swiss foreign currency reserves and Italy retail sales will be released in European session. In addition to US NFP, Canada will also release job data and Ivey PMI.

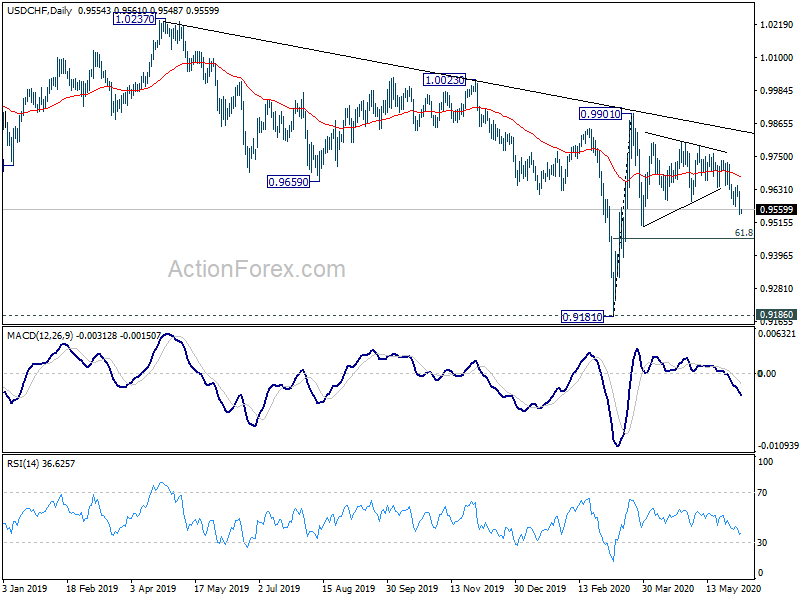

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9525; (P) 0.9575; (R1) 0.9605; More…

USD/CHF’s decline resumed after recovery was rejected by 4 hour 55 EMA. Intraday bias is back on the downside for 0.9502 support and below. Though, we’d still expect strong support from 61.8% retracement of 0.9181 to 0.9901 at 0.9456 to complete the consolidation pattern from 0.9901. On the upside, break of 0.9647 resistance should turn bias back to the upside for rebound. However, sustained trading below 0.9456 could pave the way to 0.9181 low.

In the bigger picture, decline from 1.0237 is seen as the third leg of the pattern from 1.0342 (2016 low). It could have completed at 0.9181 after hitting 0.9186 key support (2018 low). Break of 0.9901 will extend the rebound form 0.9181 through 1.0023 resistance. After all, medium term range trading will likely continue between 0.9181/1.0237 for some more time.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Services Index May | 31.6 | 27.1 | ||

| 23:01 | GBP | GfK Consumer Confidence May P | -36 | -40 | -34 | |

| 23:30 | JPY | Overall Household Spending Y/Y Apr | -11.10% | -12.80% | -6.00% | |

| 05:00 | JPY | Leading Economic Index Apr P | 80.5 | 84.7 | ||

| 06:00 | EUR | Germany Factory Orders M/M Apr | -20.00% | -15.60% | ||

| 07:00 | CHF | Foreign Currency Reserves (CHF) May | 800B | |||

| 08:00 | EUR | Italy Retail Sales M/M Apr | -10.00% | -20.50% | ||

| 12:30 | USD | Nonfarm Payrolls May | -8000K | -20537K | ||

| 12:30 | USD | Unemployment Rate May | 19.60% | 14.70% | ||

| 12:30 | USD | Average Hourly Earnings M/M May | 0.70% | 4.70% | ||

| 12:30 | CAD | Net Change in Employment May | -500.0K | -1993.8K | ||

| 12:30 | CAD | Unemployment Rate May | 15.00% | 13.00% | ||

| 15:00 | CAD | Ivey PMI May | 22.8 |

{kind=link}