Fed chair Jerome Powell inspired a fresh round of Dollar selloff which his Jackson Hole speech, which carries on to today. Stronger than expected personal income and spending, as well as core inflation reading provide little support. Though, for now, the decline appears to be mainly centered against commodity currencies, in particular Aussie and Kiwi. Yen is following closely as the third strongest, rebounding on Prime Minister Shinzo Abe’s resignation. European majors are mixed for the moment,.

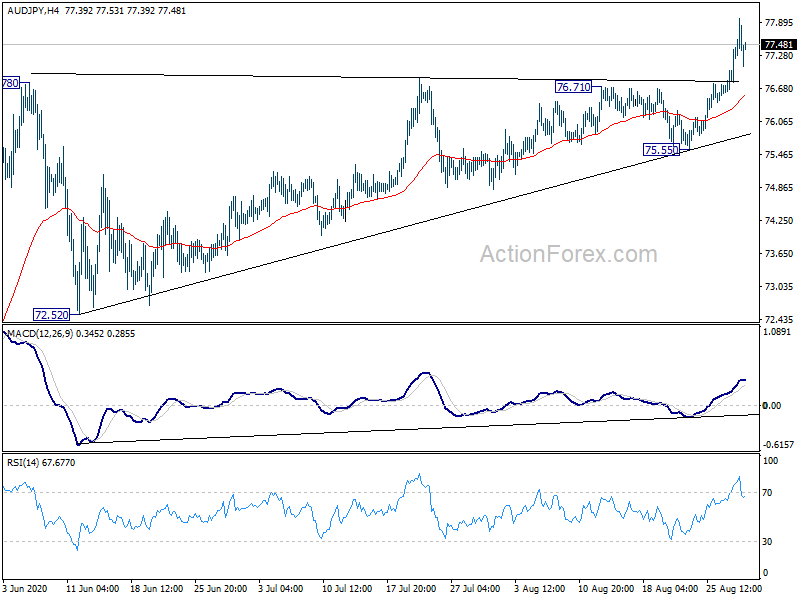

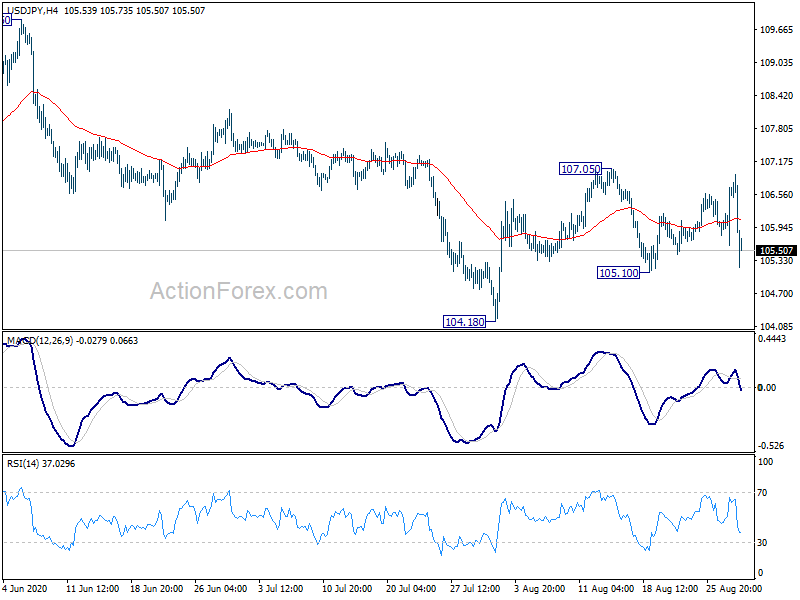

Technically, 105.10 support in USD/JPY is now in focus with today’s sharp reversal. Break will bring retest of 104.18 low. Both EUR/JPY and GBP/JPY are held above 124.31 and 138.24 support respectively, keeping near term outlook bullish despite today’s retreats. AUD/JPY also dips back notably after this week’s triangle break out. We’d maintain that 76.78 support in AUD/JPY is the first line of defense. The bull run is safe as long as this level holds.

In Europe, currently, FTSE is up 0.01%. DAX is down -0.22%. CAC is up 0.05%. German 10-year yield is down -0.004 at -0.407. Earlier in Asia, Nikkei dropped -1.41%. Hong Kong HSI rose 0.56%. China Shanghai SSE rose 1.60%. Singapore Strait Times rose 0.79%. Japan 10-year JGB yield rose 0.015 to 0.059.

US PCE price index rose to 1.0%, core PCE accelerated to 1.3%

US personal income rose 0.4%, or USD 70.5B in July, much better than expectation of -0.2% decline. Spending rose 1.9% or USD 267.6B, also above expectation of 1.5% mom. Headline PCE price index rose to 1.0% yoy, up from 0.8% yoy, but missed expectation of 1.2% yoy. On the other hand, Core PCE price index accelerated to 1.3% yoy, up from 1.1% yoy, beat expectation of 1.3% yoy.

Also released, goods trade deficit rose 11.7% mom to USD 79.3B

Canada GDP grew 6.5% mom in Jun, highest on record since 1961

Canada GDP grew 6.5% mom in June, above expectation of 5.2% mom. That’s the largest monthly increase since the series started in 1961. Still, economic activity remained about -9% below February’s pre-pandemic level. Both goods-producing (+7.5%) and services-producing (+6.1%) industries were up as 19 of 20 industrial sectors posted increases in June.

Eurozone economic sentiment rose to 87.7, recovered 60% of losses in Mar and Apr

Eurozone Economic Sentiment Indicator rose to 87.7 in August, up form 82.4, above expectation of 84.9. EU ESI rose 5 pts to 86.9. The ESIs in both regions have so far recovered around 60% of the combined losses of March and April.

As for Eurozone, industrial confidence rose from -16.2 to -12.7. Services confidence rose from -26.2 to -17.2. Consumer confidence rose slightly from -15.0 to -14.7. Retail trade confidence rose from -15.1 to -10.5. Construction confidence, however, dropped from -11.4 to -11.8. Employment Expectations also rose from 86.7 to 89.6.

France GDP -13.8% in Q2, low point reached in April

According to first estimate, French GDP dropped -13.8% qoq in Q2. It’s -19% down lower than GDP back in Q2 2019. INSEE said, “the gradual ending of restrictions led to a gradual recovery of economic activity in May and June, after the low point reached in April.”

Looking at some details, household consumption expenditures dropped (–11.0% after –5.8%), as did total gross fixed capital formation in a more pronounced manner (GFCF: –17.8% after –10.3%). General government expenditure also stepped back (–8.0% after –3.5%). Overall, final domestic demand excluding inventory changes fell sharply: it contributed to –12.0 points to GDP growth.

Exports fell this quarter (–25.5% after –6.1%) more strongly than imports (–17.3% after –5.5%). All in all, the foreign trade balance contributed negatively to GDP growth: –2.3 points, after –0.1 points the previous quarter. Conversely, changes in inventories contributed positively to GDP growth (+0.6 points).

Also from France, CPI slowed to 0.2% yoy in August, down form 0.9% yoy, well below expectation of 0.2% yoy. consumer spending rose just 0.5% mom in July, worse than expectation of 3.2% mom.

German Gfk consumer climate dropped to -1.8, coronavirus creates uncertainty again

German Gfk consumer climate for September dropped -1.8, down from -0.2, missed expectation of 2.0. Economic expectations improved to 11.7, up from 10.6. However, income expectations dropped sharply to 12.8, down form 18.6.

Rolf Bürkl, consumer expert at GfK, “an increase in the number of infections and the fear that coronavirus-related restrictions will be further tightened are creating uncertainty and consequently dampening the mood… Whether or not this is just a temporary slowdown will depend primarily on what infection rates look like in future and the necessary measures to be put in place by policy makers.”

Swiss KOF rose to 110.2, upswing phase of V-shaped recession

Swiss KOF Economic Barometer rose to 110.2 in August, up from 86.0, well above expectation of 90.0. It’s the third straight month of rise, and it’s now well above long-term average. KOF also said, “the Swiss economy is in the upswing phase of what appears for the time being a V-shaped recession.”

The indicator groups for manufacturing, the hospitality sector and foreign demand are primarily responsible for the current increase. To a lesser extent, the indicators relating to financial and insurance services as well as other services contributed to the improvement. The construction sector, on the other hand, recorded a slight deterioration.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 105.89; (P) 106.29; (R1) 106.98; More...

USD/JPY is still holding in range of 105.10/107.05 and intraday bias remains neutral first. On the upside, break of 107.05 will revive the case of near term reversal and bring stronger rally. On the downside, break of 105.10 will target a test on 104.18. Break there will resume whole decline from 111.71.

In the bigger picture, USD/JPY is still staying in long term falling channel that started back in 118.65 (Dec. 2016). Hence, there is no clear indication of trend reversal yet. The down trend could still extend through 101.18 low. However, sustained break of 112.22 should confirm completion of the down trend and turn outlook bullish for 118.65 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Aug | -0.30% | 0.30% | 0.40% | |

| 06:00 | EUR | Germany Gfk Consumer Confidence Sep | -1.8 | 2 | -0.3 | -0.2 |

| 06:45 | EUR | France CPI M/M Aug P | -0.10% | 0.40% | ||

| 06:45 | EUR | France CPI Y/Y Aug P | 0.20% | 0.70% | 0.90% | |

| 06:45 | EUR | France Consumer Spending M/M Jul | 0.50% | 3.20% | 9.00% | 10.30% |

| 06:45 | EUR | France GDP Q/Q Q2 | -13.80% | -13.80% | -13.80% | |

| 07:00 | CHF | KOF Economic Barometer Aug | 110.2 | 90 | 85.7 | 86 |

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Aug | 87.7 | 84.9 | 82.3 | 82.4 |

| 09:00 | EUR | Eurozone Services Sentiment Aug | -17.2 | -26.1 | -26.2 | |

| 09:00 | EUR | Eurozone Consumer Confidence Aug | -14.7 | -15 | -14.7 | -15 |

| 09:00 | EUR | Eurozone Industrial Confidence Aug | -12.7 | -13 | -16.2 | |

| 09:00 | EUR | Business Climate Aug | -1.33 | -1.8 | ||

| 12:30 | CAD | GDP M/M Jun | 6.50% | 5.20% | 4.50% | 4.80% |

| 12:30 | USD | Personal Income M/M Jul | 0.40% | -0.20% | -1.10% | -1.00% |

| 12:30 | USD | Personal Spending Jul | 1.90% | 1.50% | 5.60% | 6.20% |

| 12:30 | USD | PCE Price Index M/M Jul | 0.30% | 0.10% | 0.40% | 0.50% |

| 12:30 | USD | PCE Price Index Y/Y Jul | 1.00% | 1.20% | 0.80% | |

| 12:30 | USD | PCE Core Price Index M/M Jul | 0.30% | 0.40% | 0.20% | 0.30% |

| 12:30 | USD | PCE Core Price Index Y/Y Jul | 1.30% | 1.20% | 0.90% | 1.10% |

| 12:30 | USD | Wholesale Inventories Jul P | -0.10% | -1.00% | -1.40% | |

| 12:30 | USD | Goods Trade Balance (USD) Jul | -79.3B | -70.6B | -71.0B | |

| 13:45 | USD | Chicago PMI Aug | 51 | 51.9 | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Aug | 72.8 | 72.8 |

{kind=link}