After a brief pause, Dollar and Yen are both extending rally in European session today. Stocks are clearly lacking momentum for even a small recovery. More surprisingly, the selloff in oil prices accelerate with WTI now pressing 35 handle. Euro is currently is the weakest one for today, after ECB explicitly said it’s ready to “recalibrate” its instruments in December. Sterling and Canadian are the next weakest.

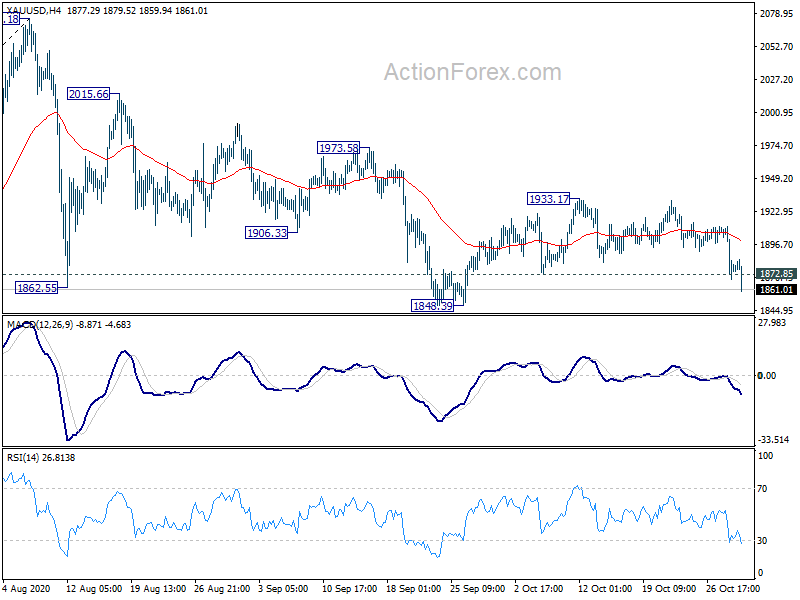

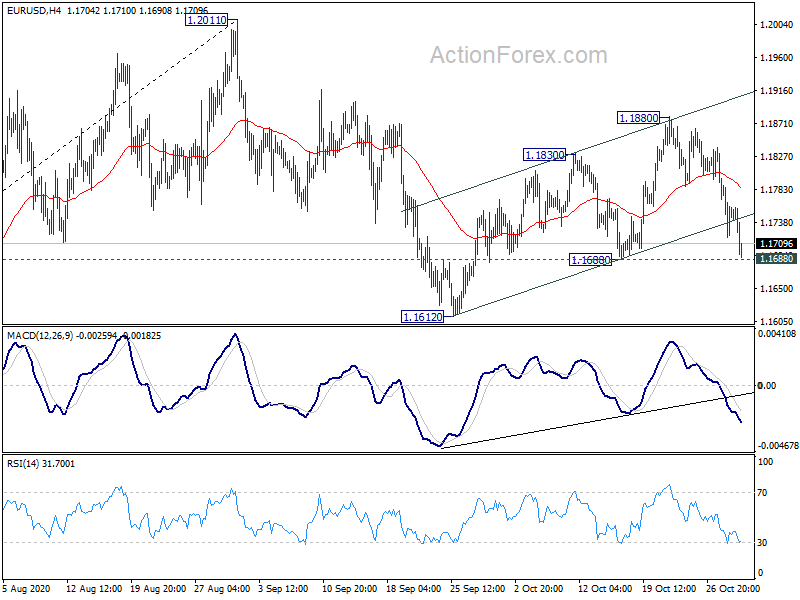

Technically, AUD/USD breaks 0.7020 support to resume the decline from 0.7413. Gold has taken out 1872.85 support decisively today, finally. Corrective pattern from 2075.18 should extend through 1848.39 low. Focus is on 1.1688 support in EUR/USD and 1.2910 support in GBP/USD. Break of these level will further affirm the underlying bullishness of the greenback.

WTI crude oil is now a key focus for the rest of the week. At this point, we’re seeing the price actions form 43.50 as a corrective move. Strong support should be seen at 100% projection of 43.50 to 35.98 from 41.62 at 34.10, which is close to 34.36 structural support, to contain downside. However, sustained break there will argue that down trend has already been developed and would pave the way to 161.8% projection at 29.45, which is below 30 handle.

In Europe, currently, FTSE is down -0.17%. DAX is down -0.18%. CAC is down -0.60%. Germany 10-year yield is down -0.0083 at -0.632. Earlier in Asia, Nikkei dropped -0.37%. Hong Kong HSI dropped -0.49%. China Shanghai SSE rose 0.11%. Singapore Strait Times dropped -1.32%. Japan 10-year JGB yield rose 0.0053 to 0.030.

US GDP grew 33.1% annualized in Q3, beat expectations

US GDP grew at annual rate of 33.1% in Q3, above expectation of 32.0%. The increase in real GDP reflected increases in personal consumption expenditures (PCE), private inventory investment, exports, nonresidential fixed investment, and residential fixed investment that were partly offset by decreases in federal government spending and state and local government spending. Imports, which are a subtraction in the calculation of GDP, increased

Initial jobless claims dropped -40k to 751k in the week ending October 24, slightly better than expectation of 763k. Four-week moving average of initial claims dropped -24.5k to 787.8k. Continuing claims dropped -709k to 7756k in the week ending October 17. Four-week moving average of continuing claims dropped -1058k to 9053k.

ECB to recalibrate instructions based on December macroeconomic projections

ECB acknowledged in the monetary policy decision statement that risks are “clearly tilted to the downside” in the current environment. New round of macroeconomic projections tin December will “allow a thorough reassessment of the economic outlook and the balance of risks”. ECB will then “recalibrate its instruments” as appropriate.

For today, main refinancing rate is held at 0.00%, marginal lending facility rate and deposit rate at 0.25% and -0.50% respectively. Forward guidance is unchanged interest rates will “remain at their present or lower levels until it has seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2% within its projection horizon”.

ECB will also continue the PEPP purchases with a total envelope of EUR 1350B “until at least the end of June 2021”. Net purchases under APP will continue at monthly pace of EUR 20B, together with the additional EUR 120B temporary envelop until the end of the year.

Eurozone economic sentiment unchanged at 90.9, but employment expectation turned negative

Eurozone Economic Sentiment Indicator was unchanged at 90.9 in October, slightly above expectation of 89.6. Industrial Confidence rose for the sixth consecutive month, from -11.4 to -9.6. Services Confidence halted the recovery and dropped from -11.2 to -11.8. Consumer Confidence slipped -1.6 pts to -15.5. Retail Trade Confidence continued its recovery and rose 1.7 pts to -6.9. However, Employment Expectations Indicator turned negative, down by -1.8 pts to 89.8.

Germany unemployment dropped -35k in October versus expectation of -5k. Unemployment rate dropped to 6.2%, better than expectation of 6.4%.

UK mortgage approvals rose to 91k in September versus expectation of 75k. M4 money supply rose 0.9% mom versus expectation of 0.3% mom.

BoJ stands pat, revised down fiscal 2020 growth and inflation forecasts

BoJ left monetary policy unchanged at widely expected. Under the yield curve control framework, short term policy interest rate is kept at -0.1%. BoJ will also continue to by JGBs, without upper limit” to keep 10-year yields at around 0%. Goushi Kataoka dissented in the 8-1 vote again, pushing for further strengthening of easing.

In the Outlook for Economic Activity and Prices report, BoJ said the economy is “likely to follow an improving trend with economic activity resuming and the impact of the novel coronavirus (COVID-19) waning gradually”. But, “the pace is expected to be only moderate while vigilance against COVID-19 continues.”

Year-on-year core CPI rate is “likely to be negative for the time being” mainly affected by COVID-19, the past decline in crude oil prices, and the “Go To Travel” campaign. Growth projections for fiscal 2020 was revised lower “mainly due to a delay in recovery in services demand”. But overall outlook is “extremely unclear”, with risks to both activity and prices “skewed to the downside”.

Median GDP forecasts:

- Fiscal 2020 revised down to -5.5% (from -4.7%)

- Fiscal 2021 revised up to 3.6% (from 3.3%).

- Fiscal 2020 revised up to 1.6% (from 1.5%).

Media core CPI forecasts:

- Fiscal 2020 revised down to -0.7% (from -0.6%).

- Fiscal 2021 revised up to (0.4% (from 0.3%).

- Fiscal 2022 unchanged at 0.7%.

Also from Japan, retail sales dropped -8.7% yoy in September versus expectation of -7.7% yoy. Consumer confidence rose to 33.6 in October, up from 32.7, beat expectation of 31.6.

Australia NAB business confidence rose to -10, conditions rose to -4

Australia NAB Business Confidence rose to -10 in Q3, up from Q2’s -15. Business Conditions improved markedly. Current situation rose from -26 to -4. Conditions for next 3 months rose from -22. to -3. Conditions for next 12 months turned positive from -8 to 13. q.

New Zealand ANZ business confidence rose to -15.7, mix of ups and downs

New Zealand ANZ Business Confidence rose to -15.7 in October, up from September’s -28.5. That’s slightly below October’s preliminary reading of -14.5. Confidence was best in construction at 12.5 and worst in agriculture at -50.0. Own Activity outlook turned positive to 4.7, up from -5.4. Activity was positive in all (including retail, manufacturing, construction and services), except agriculture at -4.0.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1712; (P) 1.1753; (R1) 1.1789; More…..

EUR/USD is still holding above 1.1688 support despite today’s decline. Intraday bias stays neutral first. On the downside, firm break of 1.1688 support should resume the corrective pattern from 1.2011 with another leg. Intraday bias will be turned to the downside for 1.1612 support first. Break will target 38.2% retracement of 1.0635 to 1.2011 at 1.1485. On the upside, though, above 1.1880 will extend the rebound from 1.1612 to retest 1.2011 high.

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally could be seen to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). This will remain the favored case as long as 1.1422 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Retail Trade Y/Y Sep | -8.70% | -7.70% | -1.90% | |

| 00:00 | NZD | ANZ Business Confidence Oct | -15.7 | -14.5 | ||

| 00:30 | AUD | NAB Business Confidence Q3 | -10 | -15 | ||

| 00:30 | AUD | Import Price Index Q/Q Q3 | -3.50% | -2.30% | -1.90% | |

| 03:00 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 05:00 | JPY | Consumer Confidence Oct | 33.6 | 31.6 | 32.7 | |

| 08:55 | EUR | Germany Unemployment Change Oct | -35K | -5K | -8K | |

| 08:55 | EUR | Germany Unemployment Rate Oct | 6.20% | 6.40% | 6.30% | |

| 09:30 | GBP | M4 Money Supply M/M Sep | 0.90% | 0.30% | -0.40% | -0.50% |

| 09:30 | GBP | Mortgage Approvals Sep | 91K | 75K | 85K | 86K |

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Oct | 90.9 | 89.6 | 91.1 | 90.9 |

| 10:00 | EUR | Eurozone Industrial Confidence Oct | -9.6 | -11.5 | -11.1 | -11.4 |

| 10:00 | EUR | Eurozone Services Sentiment Oct | -11.8 | -15 | -11.1 | -11.2 |

| 10:00 | EUR | Eurozone Consumer Confidence Oct | -15.5 | -15.5 | -15.5 | |

| 10:00 | EUR | Eurozone Business Climate Oct | -0.74 | -2 | -1.2 | -1.19 |

| 12:30 | USD | Initial Jobless Claims (Oct 23) | 751K | 763K | 787K | 791K |

| 12:30 | USD | GDP Annualized Q3 P | 33.1% | 32.0% | -31.4% | |

| 12:30 | USD | GDP Price Index Q3 P | 3.60% | 2.90% | -2.10% | -1.80% |

| 12:45 | EUR | ECB Interest Rate Decision | 0.00% | 0.00% | 0.00% | |

| 13:00 | EUR | Germany CPI M/M Sep P | 0.10% | 0.00% | -0.20% | |

| 13:00 | EUR | Germany CPI Y/Y Sep P | -0.20% | -0.30% | -0.20% | |

| 13:30 | EUR | ECB Press Conference | ||||

| 14:00 | USD | Pending Home Sales M/M Sep | 3.60% | 8.80% | ||

| 14:30 | USD | Natural Gas Storage | 35B | 49B |

{kind=link}