Dollar retreats mildly in Asian session today as overall market sentiments improved some what. Major Asian indices, except China, recovered notably, following DOW’s rally. But weakness in US tech is keeping upside capped. Selloff in Yen and Swiss Franc, and to a lesser extend Kiwi, is still the main theme, on resilience in global treasury yields. Sterling is attempting to take over Dollar’s top spot, while Aussie could catch up any time.

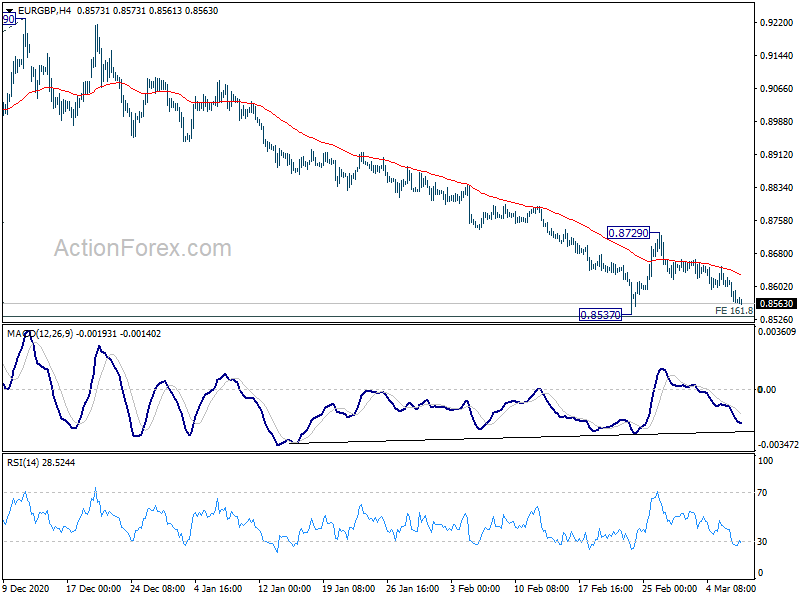

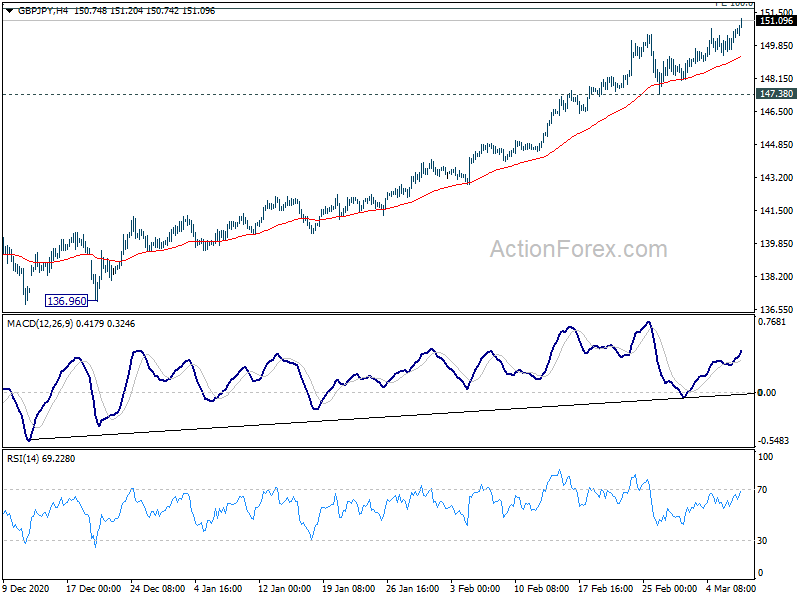

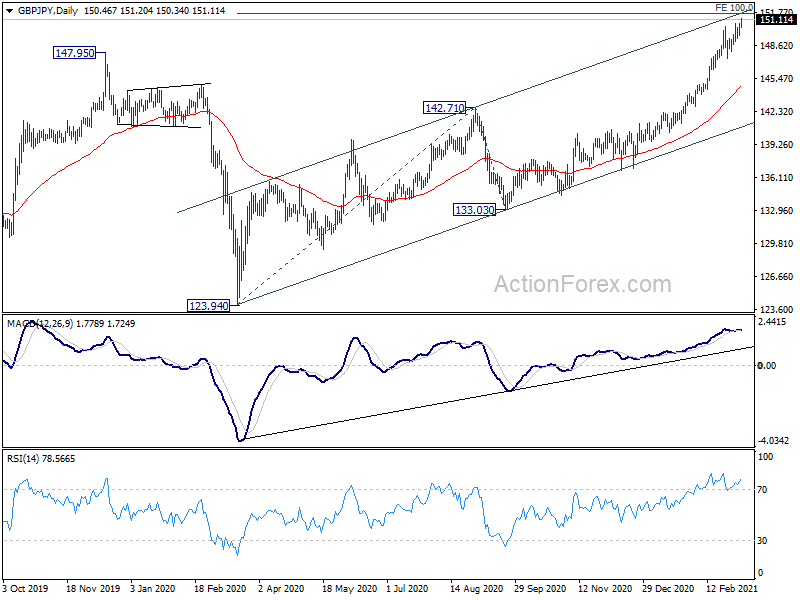

Technically, GBP/JPY’s rally picks up momentum again and it’s on track to 151.80 projection level. But this cold be a tough one to take out as it coincides with medium term channel resistance. The cross will likely need simultaneous strength in the Pound as well as weakness in Yen to push through this resistance. With that in mind, we’ll pay special attention to 0.8537 support in EUR/GBP to gauge the upside potential in GBP/JPY beyond 151.80.

In Asia, currently, Nikkei is up 0.91%. Hong Kong HSI is up 1.44%. China Shanghai SSE is up 0.13%. Singapore Strait Times is up 1.16%. Japan 10-year JGB yield is up 0.0128 at 0.135. Overnight, DOW rose 0.97%. S&P 500 dropped -0.54%> NASDAQ dropped -2.41%. 10-year yield rose 0.042 to 1.596.

Japan household spending dropped -6.1% yoy in Jan

Japan household spending dropped -6.1% yoy in January, much worse than expectation of -2.1% yoy. That’s also the second straight month of decrease, as spending was dragged down by a second state of emergency. “With people refraining from going out under the state of emergency, outlays for items such as suits and dresses fell,” a Ministry of Internal Affairs and Communications official told reporters. Also released, nominal total cash earnings dropped -0.8% yoy in January, down for a 10th straight month.

In Q4, GDP growth was finalized at 2.8% qoq, 11.7% yoy. The figures were revised down form 3.0% qoq, 22.9% annualized. Capital expenditure grew 4.3% qoq. External demand rose 1.1% qoq. Private consumption rose 2.2% qoq. Price index rose 0.3% yoy.

The economy is expected to shrink in Q1 as it returned to pandemic restrictions. Prime Minister Yoshihide Suga last week extended the emergency through March 21 for the Tokyo region.

Australian NAB business confidence rose to 16, highest since early 2010

Australia NAB business confidence rose from 12 to 16 in February. That’s the highest level since early 2010, as all states and industries reported gains, except for retail. Business conditions rose from 9 to 15, also a multi-year high. Looking at some details, trading conditions rose from 13 to 21. Profitability conditions rose from 13 to 17. Employment conditions rose from 3 to 8.

“Businesses are the most optimistic they’ve been since 2010. This says the economy recovery has very strong momentum and even though government support is tapering, businesses are increasingly confident the economy will continue to improve,” said Alan Oster, NAB Group Chief Economist.

“Business conditions have rebounded to the very strong levels we saw in December and, importantly, employment conditions remain strong. Businesses are again expanding their workforce, which is key for supporting the labour market recovery.”

New Zealand ANZ business confidence dropped to 0, gains will be harder won

In the preliminary reading, New Zealand ANZ business confidence dropped from 7 to 0 in March. Own activity outlook also dropped from 21.3 to 17.4. Looking at some more details, export intensions rose form 5.1 to 6.0. Investment intentions dropped slightly from 15.6 to 14.4. Employment intentions jumped from 10.6 to 16.0. Pricing intentions rose from 46.2 to 48.9. Inflation expectations rose from 1.76 to 1.95.

ANZ said: “The economy is entering a phase in which gains will be harder won. The tourism sector pain is becoming more palpable, and booming sectors such as construction are running up against constraints in terms of the availability of labour and, increasingly, imported materials.”

DOW hit intraday record high, NASDAQ underwhelmed again

US stocks ended mixed overnight, probably on sector rotation. DOW closed up 306.14 pts or 0.97% at 31802.44. That came after hitting intraday record high at 32148.04. However, S&P 500 dropped -20.59 pts or -0.54% to close at 3821.35. NASDAQ dropped deeply by 310.98 pts or -2.41% to close at 12609.16.

DOW draw strong support from 55 day EMA to extend recent up trend. Though, upside momentum is still relatively weak, as seen in daily MACD. It’s also capped below near term channel resistance. Nevertheless, outlook will stay bullish as long as 30547.53 support holds. We’d still expect DOW to crawl towards 61.8% projection of 18213.65 to 29199.35 from 26143.77 at 32932.93, which is close to 33k handle.

While NASDAQ dropped notably overnight, it’s actually still contained above last week’s low at 12397.05. Our view is unchanged that fall from 14175.11 is seen as correcting the rise from 10822.57 only. Strong support is expected at 12074.06 (61.8% retracement of 10822.57 to 14175.11 at 12103.24) to bring rebound. That should set the base for up trend resumption later.

However, sustained break of 12074.06 will argue that NASDAQ is already correcting the whole up trend from 6631.42. In this case, deeper, medium-term, correction, could be seen through 10822.57 support.

Looking ahead

Eurozone GDP revision will be a focus in European session. Germany will release trade balance while industrial will release industrial output. Later in the day, US will release NFIB business optimism index.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 149.89; (P) 150.30; (R1) 150.92; More…

GBP/JPY reaches as high as 151.20 so far today as recent rally continues. Intraday bias stays on the upside for 100% projection of 123.94 to 142.71 from 133.03 at 151.80 next. That would be close to channel resistance (from 123.94 low) at 151.77. We’d be cautious on topping from there. But decisive break of this level will indicate upside acceleration for next key resistance at 156.59. Though, break of 147.38 support will indicate short term topping and bring deeper correction.

In the bigger picture, rise from 123.94 is seen as the third leg of the sideway pattern from 122.75 (2016 low). With 147.95 resistance taken out, further rally would now be seen to 156.59 resistance (2018 high), Sustained break there should confirm long term bullish trend reversal. On the downside, break of 142.71 resistance turned support is needed to be the first sign of completion of the rise from 123.94. Otherwise, outlook will remain bullish even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Manufacturing Sales Q4 | -0.60% | 10.00% | 10.40% | |

| 23:30 | JPY | Labor Cash Earnings Y/Y Jan | -0.80% | -1.70% | -3.00% | |

| 23:30 | JPY | Overall Household Spending Y/Y Jan | -6.10% | -2.10% | -0.60% | |

| 23:50 | JPY | GDP Q/Q Q4 F | 2.80% | 3.00% | 3.00% | |

| 23:50 | JPY | GDP Deflator Y/Y Q4 | 0.30% | 0.20% | 0.20% | |

| 23:50 | JPY | Money Supply M2+CD Y/Y Feb | 9.60% | 9.50% | 9.40% | |

| 00:00 | NZD | ANZ Business Confidence Mar P | 0 | 7 | ||

| 00:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Feb | 9.50% | 7.10% | ||

| 00:30 | AUD | NAB Business Confidence Feb | 16 | 10 | 12 | |

| 06:00 | JPY | Machine Tool Orders Y/Y Feb P | 9.70% | |||

| 07:00 | EUR | Germany Trade Balance (EUR) Jan | 17.9B | 16.1B | ||

| 09:00 | EUR | Italy Industrial Output M/M Jan | 0.70% | -0.20% | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q4 | -0.60% | -0.60% | ||

| 10:00 | EUR | Eurozone Employment Change Q/Q Q4 F | 0.30% | 0.30% | ||

| 11:00 | USD | NFIB Business Optimism Index Feb | 96.2 | 95 |

{kind=link}