The markets are lacking a clear direction for the moment as traders await the highly anticipated Jackson Hole symposium of global central bankers. Sterling is the notably weaker one this week but there is no follow through selling seen today. The pound is trying to recovery against Dollar, Euro as well as Yen. EUR/USD is still staying in range below 1.1908 as recent consolidation extends. Some strength is seen in Canadian Dollar today as USD/CAD dips through 1.2525 temporary low. That could be thanks to WTI oil’s recovery back above 48. Gold is also hovering in tight range below 1300.

Draghi not expected to deliver anything special

The Jackson hole symposium, titled "Fostering a Dynamic Global Economy," is hosted by the Kansas City Federal Reserve Bank. It kicks off later day and runs through Saturday. Main focus in on European Central Bank President Mario Draghi and Federal Reserve chair Janet Yellen. Both will deliver a speech on Friday. There were already talks that Draghi will not deliver a policy shift in the occasion. And it’s understandable as he already indicated that ECB will discuss the composition of stimulus in September. Some analysts noted that Draghi’s silence on monetary policy would clear up the risks of a dovish message. And in that case, Euro could finally gather the momentum to complete the near term consolidation from 1.1908 against Dollar.

Yellen won’t neither

At the same time, Fed chair Janet Yellen is also unlikely to deliver anything new regarding Fed’s policies. Fed has already indicated in the July FOMC minutes that "participants generally agreed that, in light of their current assessment of economic conditions and the outlook, it was appropriate to signal that implementation of the program likely would begin relatively soon, absent significant adverse developments in the economy or in financial markets". Fed is generally expected to announce the program to unwind its balance sheet in September. And we argue that Fed will still do it in spite of the uncertainties on raising the debt limit by Congress (more in US Debts Approach Limit. How Will It Affect Fed’s Policy?) And for the moment, it’s too early for Yellen to indicate whether Fed will hike again in December.

Fitch warns of rating review with negative implications

Raising of debt ceiling will be a key focus in the US in September. Credit ratings agency Fitch warned that failure to raise the debt ceiling would prompt a review on US AAA sovereign rating "with potentially negative implications". Fitch warned that "brinkmanship over the debt limit could ultimately have rating consequences, as failure to raise it would jeopardize the Treasury’s ability to meet debt service and other obligations." It noted that "republican fiscal conservatives are likely to make support for lifting the debt limit conditional on measures to aggressively reduce the budget deficit. A ‘clean’ debt limit increase, unattached to other policy measures, appears possible, although it may require support from Democrats." And, "in Fitch’s view, the economic impact of stopping other spending to prioritize debt repayment, and potential damage to investor confidence in the full faith and credit of the U.S., which enables its ‘AAA’ rating to tolerate such high public debt, would be negative for U.S. sovereign creditworthiness."

Trump blames Paul Ryan and Mitch McConnell

US President Donald Trump tweeted that "I requested that Mitch M & Paul R tie the Debt Ceiling legislation into the popular V.A. Bill (which just passed) for easy approval. They didn’t do it so now we have a big deal with Dems holding them up (as usual) on Debt Ceiling approval. Could have been so easy-now a mess!" But it’s generally perceived by the analysts that risks of government shutdown and debt payment defaults surged after Trumps’ threat that "if we have to close down our government, we’re building that wall" of US-Mexico border. He has requested USD 1.6b for building the US-Mexico border wall but that is widely rejected by Democrats. And, even though the House has passed a spending package with the wall funding, Trump doesn’t have enough support to pass in the Senate by September 30. And he could in the end veto the spending bill if wall funding is not included. At the same time, some Republicans are working on a bipartisan bill with Democrats on raising debt ceiling. But the Democrats are clear on their rejection of attaching any condition to the debt bill.

ECB Hansson not concerned with Euro strength

Separately, ECB governing council member Ardo Hansson talked down the concern of strength in Euro as ECB might taper the asset purchase program. He noted that "it’s not surprising that markets might react and say, on balance, we’re more upbeat about Europe than we were a while ago, which will cause the currency to be a bit stronger." Hansson said he doesn’t have a view on what the packaged will be after the current EUR 60b per month asset purchase program ends by the end of the year. Regarding stimulus exit Hansson emphasized to split the "degree of accommodation" and "how you deliver it". And ECB may still want to maintain an "easing bias" but deliver it in "somewhat difference combination."

On the data front.

US initial jobless claims rose 2k to 234k in the week ended August 19, below expectation of 236k. Continuing claims were unchanged at 1.95m in the week ended August 12. UK Q2 GDP growth was unrevised at 0.3% qoq. UK index of services rose 0.5% 3mo3m in June, BBA mortgage approvals rose to 41.6k in July, CBI realized sales dropped to -10 in August. New Zealand trade surplus narrowed to NZD 85b in July but was better than expectation of NZD -200m deficit.

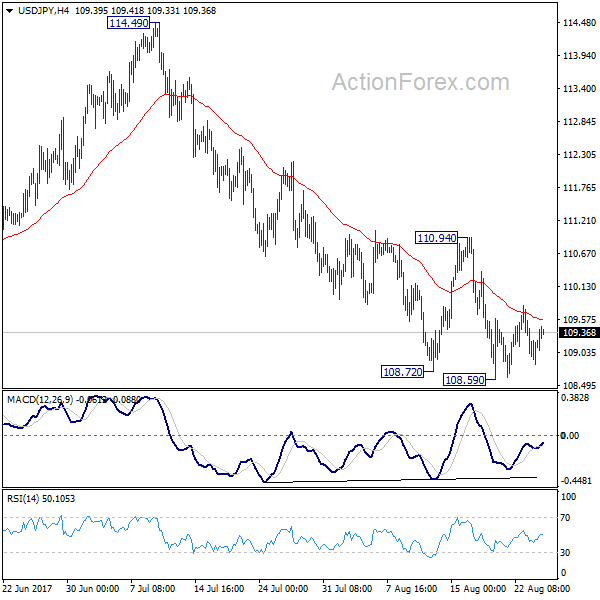

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.69; (P) 109.26; (R1) 109.59; More…

USD/JPY continues to engage in consolidative trading above 108.59 temporary low. Intraday bias remains neutral for the moment. Near term outlook stays bearish with 110.94 resistance intact and deeper decline is expected. Break of 108.59 will target a test on 108.12 low. Whole corrective decline from 118.65 is possibly resuming and break of 108.12 will target 61.8% retracement of 98.97 to 118.65 at 106.48. Nonetheless, firm break of 110.94 will indicate short term bottoming and turn bias back to the upside.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it’s uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it’s a leg in the consolidation from 125.85. Hence, we’ll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, downside should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Jul | 85M | -200M | 242M | 246M |

| 08:30 | GBP | BBA Mortgage Approvals Jul | 41.6K | 40.2K | 40.4K | |

| 08:30 | GBP | GDP Q/Q Q2 P | 0.30% | 0.30% | 0.30% | |

| 08:30 | GBP | Index of Services 3M/3M Jun | 0.50% | 0.50% | 0.40% | 0.30% |

| 08:30 | GBP | Total Business Investment Q/Q Q2 P | 0.00% | -0.10% | 0.60% | |

| 10:00 | GBP | CBI Realized Sales Aug | -10 | 14 | 22 | |

| 12:30 | USD | Initial Jobless Claims (AUG 19) | 234K | 236K | 232K | |

| 14:00 | USD | Existing Home Sales Jul | 5.57M | 5.52M | ||

| 14:30 | USD | Natural Gas Storage | 53B | |||

| Jackson Hole Symposium |