Yen’s selloff is a dominant theme in the markets today as major global treasury yields strengthen. In particular, Germany 10-year bund year is back at around -0.18, above -0.2 handle. US 10-year yield is trading at 1.675 at the time of writing, with a take on 1.7 handle before weekend a possibility. Dollar recovers mildly after solid GDP and better than expected jobless claims. But it’s merely in consolidation against others except Yen. Canadian Dollar continues to be the strongest one, but Aussie and Kiwi retreat.

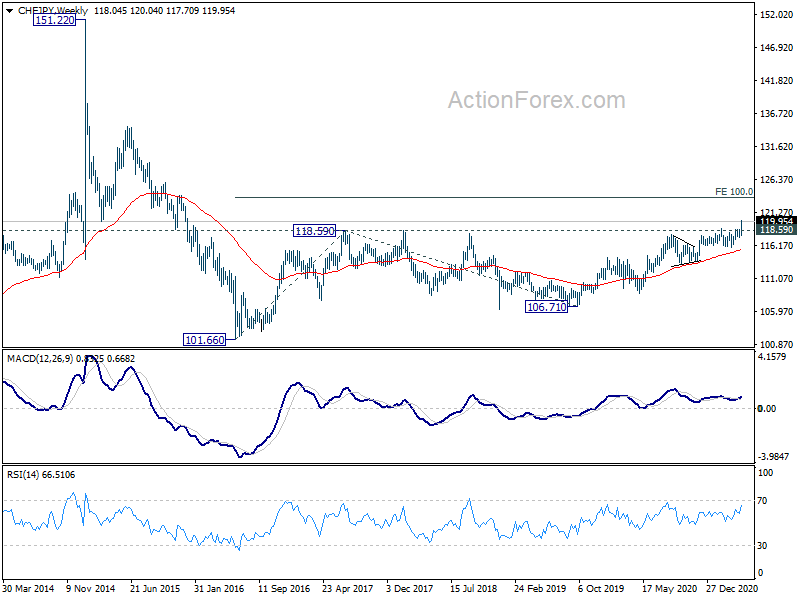

Technically, the strong rally in CHF/JPY in the past two days is worth a special mention. Key long term resistance level at 118.59 is finally taken out decisively. It’s now extending the whole pattern from 101.66 (2016 low), and should target 100% projection of 101.66 to 118.59 from 106.71 at 123.64 in the medium term. If that’s the case, we’d more likely seen other Yen crosses climb faster ahead.

In Europe, currently, FTSE is up 0.60%. DAX is down -0.42%. CAC is up 0.42%. German 10-year yield is up 0.040 at -0.186. Earlier in Asia, Nikkei rose 0.21%. Hong Kong HSI rose 0.80%. China Shanghai SSE rose 0.52%. Singapore Strait Times rose 0.06%. Japan 10-year JGB yield rose 0.0098 to 0.095.

US GDP grew 6.4% annualized in Q1, initial jobless claims dropped to 553k

US GDP grew 6.4% annualized in Q1, slightly below expectation of 6.5%. BEA said: “The increase in real GDP in the first quarter reflected increases in personal consumption expenditures (PCE), nonresidential fixed investment, federal government spending, residential fixed investment, and state and local government spending that were partly offset by decreases in private inventory investment and exports. Imports, which are a subtraction in the calculation of GDP, increased.”

Initial jobless claims dropped -13k to 553k in the week ending April 24, below expectation of 560k. Four-week moving average of initial claims dropped -44k to 612k, lowest since March 14, 2020. Continuing claims rose 9k to 3660k in the week ending April 17. Four-week moving average of continuing claims dropped -23k to 3684k, lowest since March 28, 2020.

Eurozone economic sentiment rose to 110.3, back above pre-pandemic levels

Eurozone Economic Sentiment Indicator rose strongly by 9.4 to 110.3 in April, above expectation of 103.0. It also scored markedly above its long term average and pre-pandemic level for the first time since the coronavirus outbreak in Europe. Employment Expectations Indicator also jumped 9.3 pts to 107.1), lifting it above long-term average and pre-pandemic level too.

Looking at some details, Eurozone industrial confidence rose from 1.1 to 9.4. Services confidence rose from -9.4 to 2.8. Consumer confidence rose from -12.1 to -9.0. Retail trade confidence rose from -11.0 to -1.5. Construction confidence rose from -5.0 to 0.8.

EU ESI rose 9.8 pts to 109.7. The ESI rose markedly in all of the six largest EU economies, most so in Poland (+11.3), followed by the Netherlands (+10.7), Spain (+9.1), France (+8.5), Germany (+5.7) and Italy (+5.3). Thanks to the latest increases, sentiment in all six countries is above its long-term average of 100.

Also released, Eurozone M3 money supply rose 10.1% yoy in March, below expectation of 10.2% yoy. Germany unemployment rose 9k in April versus expectation of -10k. Unemployment rate was unchanged at 6%. Germany CPI accelerated to 2.0% yoy in April, up from 1.7% yoy, above expectation of 1.8% yoy.

New Zealand goods exports dropped -2.3% yoy, imports rose 11.0% yoy in March

New Zealand goods exports dropped -2.3% yoy to NZD 5.7B in March. Imports rose 11.0% yoy to NZD 5.6B. Trade surplus narrowed to NZD 33m, down from NZD 201m, matched expectations.

Exports to China was up NZD 423m to NZD 1.8B. But exports to all other top trading partners were down, with USA down NZD -52m, EU down NZD -49m, AU down NZD -105m, Japan down NZD -25m.

Imports from China was up NZD 624m to NZD 1.3B, from EU was up NZD 132m, from AU was up NZD 65m, from Japan was up NZD 19m. But imports from USA was down NZD -74m.

New Zealand ANZ business confidence rose to -2 in Apr, a pretty inflationary soup cooking

New Zealand ANZ Business Confidence rose to -2.0 in April, up from March’s -4.1, much better than preliminary reading of -8.4. Own Activity Outlook rose to 22.2, up from 16.6, versus prelim 16.4. Exports intentions rose to 9.1, up from 4.5. Investment intentions rose to 17.1, up from 11.9. Cost expectations rose to 76.1, up from 73.3. Employment intentions rose to 16.4, up from 14.4. Pricing intentions rose to 55.8, up form 47.3.

ANZ said: “Given supply-side constraints are biting so hard, the confidence and robust employment intentions of firms may represent greater upside to wages and prices than to actual growth. It’s looking like a pretty inflationary soup. The RBNZ will be keen to look through cost-push inflation as far as possible, because it’s temporary…. But there’s clearly plenty of demand and risk-taking out there. The notion that the RBNZ might be overcooking things may well gain some traction in the months ahead, especially with headline inflation expected to rise above 2% in mid-2021.”

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.43; (P) 108.76; (R1) 108.94; More…

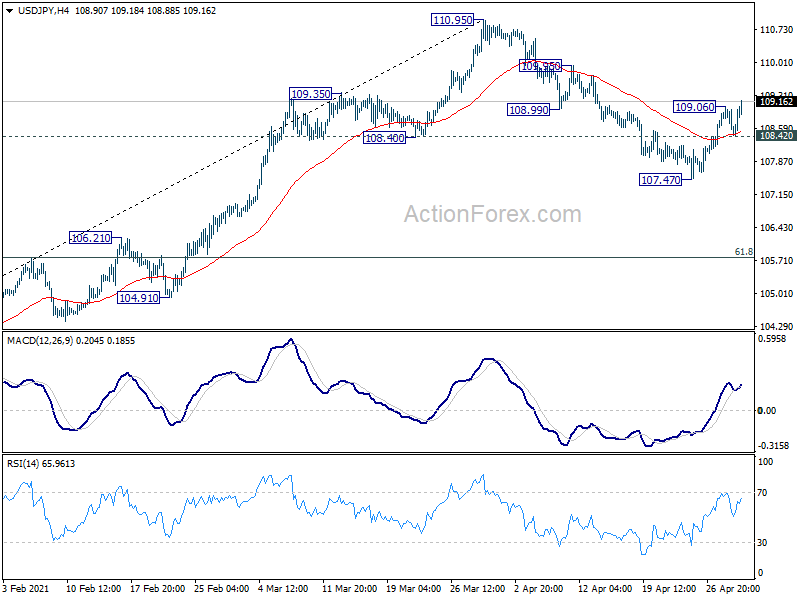

USD/JPY’s rebound from 107.47 resumed after brief retreat. Intraday bias is back on the upside for 109.95 resistance first. Break till bring retest of 110.95 high. On the downside, break of 108.42 minor support will turn bias to the downside for 107.47 support again.

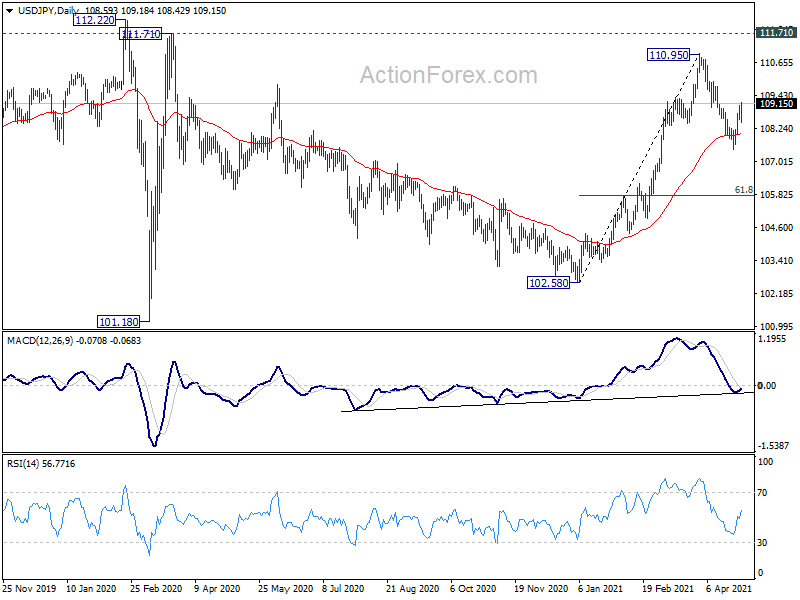

In the bigger picture, rise from 102.58 might have completed at 110.95, as the third leg of the pattern from 101.18 low. Medium term outlook is neutral first, as the pair could have turned into sideway trading between 101.18/111.71. We’d look at the structure and momentum of the price actions from 110.95 to gauge the chance of upside breakout at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Mar | 33M | 33M | 181M | 201M |

| 00:00 | NZD | ANZ Business Confidence Apr F | -2 | -8.4 | ||

| 01:30 | AUD | Import Price Index Q/Q Q1 | 0.20% | -1.10% | -1.00% | |

| 07:55 | EUR | Germany Unemployment Change Apr | 9K | -10K | -8K | -6K |

| 07:55 | EUR | Germany Unemployment Rate Apr | 6% | 6% | 6% | |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Mar | 10.10% | 10.20% | 12.30% | 12.20% |

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Apr | 110.3 | 103 | 101 | 100.9 |

| 09:00 | EUR | Eurozone Consumer Confidence Apr F | -8.1 | -8.1 | -8.1 | -10.8 |

| 09:00 | EUR | Eurozone Services Sentiment Apr | 2.1 | -8 | -9.3 | -9.6 |

| 09:00 | EUR | Eurozone Industrial Confidence Apr | 10.7 | 4.3 | 2 | 2.1 |

| 09:00 | EUR | Eurozone Business Climate Apr | 1.13 | 0.3 | 0.31 | |

| 12:00 | EUR | Germany CPI M/M Apr P | 0.70% | 0.50% | 0.50% | |

| 12:00 | EUR | Germany CPI Y/Y Apr P | 2.00% | 1.80% | 1.70% | |

| 12:30 | USD | Initial Jobless Claims (Apr 23) | 553 K | 560K | 547K | 566 K |

| 12:30 | USD | GDP Annualized Q1 P | 6.40% | 6.50% | 4.30% | |

| 12:30 | USD | GDP Price Index Q1 P | 4.10% | 2.60% | 1.90% | |

| 14:00 | USD | Pending Home Sales M/M Mar | 3.50% | -10.60% | ||

| 14:30 | USD | Natural Gas Storage | 8B | 38B |

{kind=link}