Yen dropped notably overnight and stays pressured in Asian session with markets back in risk-on mode. NASDAQ closed at new record high while DOW and S&P 500 also gained. Major Asian indexes follow with solid gains in Hong Kong. Dollar also extended this week’s retreat but losses are so far limited. Meanwhile, commodity currencies are extending recovery too.

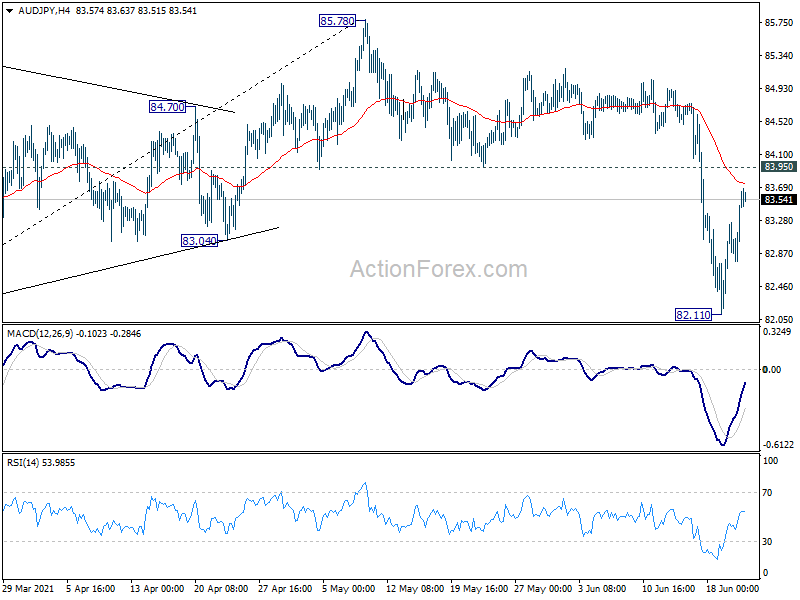

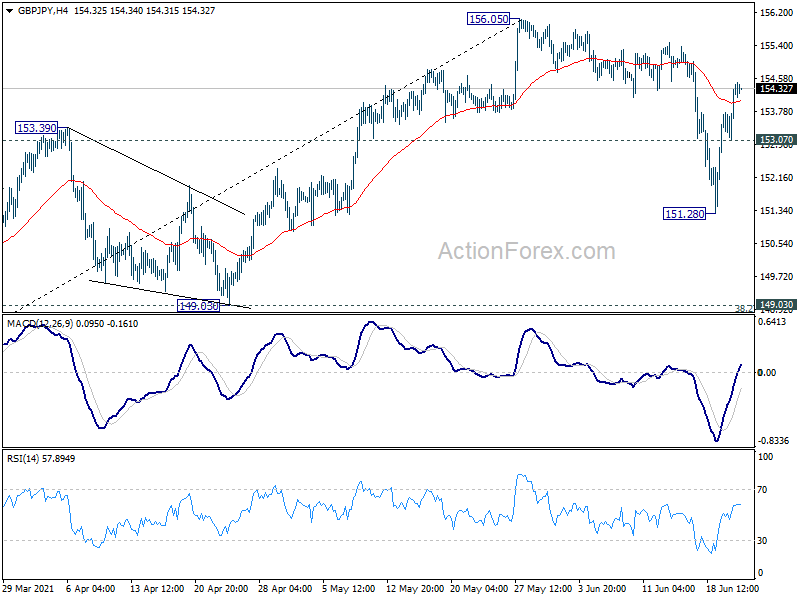

Technically, USD/JPY’s breach of 110.81 resistance suggests resumption of the choppy rise from 107.47 towards 110.95 high. GBP/JPY’s break of 154.10 resistance suggests that correction from 156.05 has completed at 151.28 already. Similarly, EUR/JPY is heading back towards 132.63 resistance and break will align the outlook with GBP/JPY. Also, break of 83.95 resistance in AUD/JPY will also suggest completion of correction from 85.78.

In Asia, Nikkei is up 0.03%. Hong Kong HSI is up 1.46%. China Shanghai SSE is up 0.46%. Singapore Strait Times is up 0.56%. Japan 10-year JGB yield is down -0.0007 at 0.054. Overnight, DOW rose 0.20%. S&P 500 rose 0.51%. NASDAQ rose 0.79% to 14253, new record. 10-year yield dropped -0.012 to 1.472.

Fed Powell not expecting 1970s style inflation to happen

Fed Chair Jerome Powell insisted in a House panel hearing that “we will not raise interest rates preemptively because we fear the possible onset of inflation.” Instead, “we will wait for evidence of actual inflation or other imbalances.” He reiterated that the transitory factors that pushed up inflation should “resolve themselves” in the coming months. And, “they don’t speak to a broadly tight economy and to the kinds of things that have led to higher inflation over time.”

“I will say that these effects have been larger than we expected, and they may turn out to be more persistent than we have expected,” he explained. “But the incoming data are very consistent with the view that these are factors that will wane over time, and inflation will then move down toward our goals and we’ll be monitoring that carefully.”

“You have a central bank that’s committed to price stability and has defined what price stability is and is strongly prepared to use its tools to keep us around 2% inflation,” he said. “All of these things suggest to me that an episode like what we saw in the 1970s … I don’t expect anything like that to happen.”

Australia goods export hits new record, led by China and Hong Kong

According to preliminary estimate, Australia exports of goods rose 11.0% mom to AUD 39.2B in May. Imports of goods rose 1.0% mom to AUD 25.9B. Goods trade surplus widened to AUD 13.3B, from AUD 9.7B. That’s a record trade surplus as iron ore, together with strong coal and meat exports, has helped boost total exports to a new record high

Exports to China jumped AUD 2271m or 16%, to Hong Kong by AUD 622m or 69%, to Singapore by 133m or 9%. Exports to Japan dropped AUD 160m or -4%, to South Korea by AUD 280m or -11%.

Australia PMI composite dropped to 56.1, growth momentum eased by remained strong

Australia PMI Manufacturing dropped back to 58.4 in June, down from may’s 60.4. PMI Services dropped to 56.0, down from 58.0. PMI Composite dropped to 56.1, down from 58.0.

Jingyi Pan, Economics Associate Director at IHS Markit, said: “Australia’s private sector growth momentum further eased in June but remained at a strong level to indicate continued improvement in economic conditions during the recovery from the COVID-19 pandemic. Renewed movement restrictions in the Victorian state and supply constraints stood out as two key reasons weighing on the growth momentum for Australia in the June flash PMI data, which is worth scrutinising. Meanwhile private sector firms were also slightly less optimistic with regards to output in the next 12 months amid the uncertain virus and supply situation.”

Japan PMI manufacturing dropped to 51.5, output back in contraction

Japan PMI Manufacturing dropped to 51.5 in June, down from May’s 53.0. Manufacturing Output dropped to 49.1, down from 53.7, back in contraction for the first time since January. PMI Services rose slightly to 47.2, up from 46.5. PMI Composite dropped to 47.8, down from 48.8.

Usamah Bhatti, Economist at IHS Markit, said: “Activity at Japanese private sector businesses remained in contraction territory… Panel members commonly associated disruption to operating conditions to ongoing COVID-19 restrictions, coupled with severe supply chain pressures, notably for manufacturers.

“That said, one bright note was private sector firms in Japan continued to expand employment levels despite subdued demand conditions… Despite the ongoing pandemic-related restrictions on the Japanese economy, private sector businesses were optimistic that business conditions would improve in the year ahead, and to a greater extent than that seen in May.”

Looking ahead

Eurozone and UK PMIs will be the main focus in European session. Later in the day, Canada will release retail sales; US will release PMIs, new home sales and current account.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 153.48; (P) 153.98; (R1) 154.85; More…

GBP/JPY’s break of 154.10 support turned resistance suggests that correction from 156.05 has completed at 151.28 already. Intraday bias is back on the upside for retesting 156.05 high. Firm break there will resume larger up trend from 123.94. Nevertheless, consolidation from 156.05 could still extend with another falling leg. Break of 153.07 minor support will turn bias back to the downside for 151.28 again.

In the bigger picture, rise from 123.94 is seen as the third leg of the pattern from 122.75 (2016 low). Focus is now on 156.59 resistance (2018 high). Sustained break there should confirm long term bullish trend reversal. Next target is 61.8% retracement of 195.86 (2015 high) to 122.75 at 167.93. On the downside, break of 149.03 support is needed to be the first sign of completion of the rise from 123.94. Otherwise, outlook will remain bullish even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:00 | AUD | CBA Manufacturing PMI Jun P | 58.4 | 60.4 | ||

| 23:00 | AUD | CBA Services PMI Jun P | 56 | 58 | ||

| 23:50 | JPY | BoJ Minutes | ||||

| 0:30 | JPY | Manufacturing PMI Jun P | 51.5 | 53.2 | 53 | |

| 7:15 | EUR | France Manufacturing PMI Jun P | 59 | 59.4 | ||

| 7:15 | EUR | France Services PMI Jun P | 59.4 | 56.6 | ||

| 7:30 | EUR | Germany Manufacturing PMI Jun P | 63 | 64.4 | ||

| 7:30 | EUR | Germany Services PMI Jun P | 55.5 | 52.8 | ||

| 8:00 | EUR | Eurozone Manufacturing PMI Jun P | 62.1 | 63.1 | ||

| 8:00 | EUR | Eurozone Services PMI Jun P | 57.6 | 55.2 | ||

| 8:30 | GBP | Manufacturing PMI Jun P | 64 | 65.6 | ||

| 8:30 | GBP | Services PMI Jun P | 63 | 62.9 | ||

| 12:30 | CAD | Retail Sales M/M Apr | -5.10% | 3.60% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Apr | 2.20% | 4.30% | ||

| 12:30 | USD | Current Account (USD) Q1 | -205B | -188B | ||

| 13:00 | CHF | SNB Quarterly Bulletin Q2 | ||||

| 13:45 | USD | Manufacturing PMI Jun P | 61.5 | 62.1 | ||

| 13:45 | USD | Services PMI Jun P | 70 | 70.4 | ||

| 14:00 | USD | New Home Sales M/M May | 876K | 863K | ||

| 14:30 | USD | Crude Oil Inventories | -7.4M |

{kind=link}