Markets have turned quiet today as focus is shifted to FOMC policy decisions. While a tapering announcement is highly unlikely, there are still prospects of hawkish surprises in the dot plot and the economic projections. In the currency markets, Sterling is currently the worst performing one for the week, followed by Kiwi and then Aussie. Swiss Franc is the strongest, followed by Yen and Dollar. The picture could solidify itself if overall risk sentiments turn sour again after FOMC.

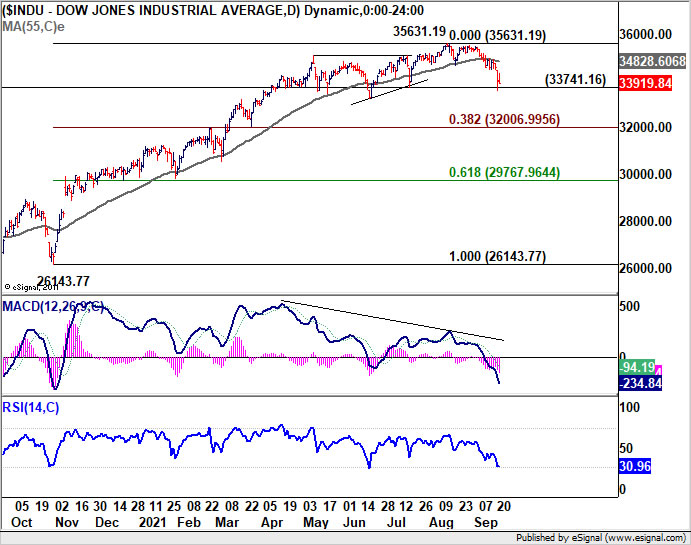

Technically, we’d continue to look at the development in US stocks to gauge overall market direction. DOW breached 33741.16 structural support briefly earlier in the week. Subsequent recovery has been rather weak so far. Another take on the support level and a firm break there would confirm that DOW is already in correction to whole medium term up trend from 26143.77 at least. In this case, 38.2% retracement at 32006.99 will be the next target. Such development, if happens, would likely be accompanied by buying in Yen, Swiss Franc and Dollar, and upside breakouts in respective pairs.

In Asia, at the time of writing, Nikkei is down -0.74%. China Shanghai SSE is down -0.29%. Singapore Strait Times is down -0.66%. Japan 10-year JGB yield is down -0.0048 at 0.035. Hong Kong is on holiday. Overnight, DOW dropped -0.15%. S&P 500 dropped -0.08%. NASDAQ rose 0.22%. 10-year year rose 0.015 to 1.324.

BoJ stands pat, notes supply side constraints

BoJ left monetary policy unchanged today. Under the yield curve control framework, short term policy interest rate is held at -0.10%. 10-year JGB yield target is kept at around 0%, without upper limit on bond purchases. The decision was made by 8-1 vote, with Goushi Kataoka dissenting as usual, pushing for strengthening easing. It also pledged to closely monitor the pandemic impact and “will not hesitate to take additional easing measures if necessary”.

Overall assessment on the economy was maintained as its has “picked up as a trend” but “remained in a severe situation” due to the pandemic home and abroad. But it noted that some exports and production have been “affected by supply-side constraints”. Weakness has been seen in some industries on business fixed investment. Employment and income “remained weak” while private consumption remained “stagnant”. Core CPI has been at around 0% and inflation expectations have been “more or less unchanged”.

Australia leading index dropped to -0.5% in Aug, more weakness on the way

Australia Westpac-MI leading index dropped from 1.4% to -0.5% in August. Westpac said “the Leading Index has held up surprisingly well during this downturn but it seems likely that there is more weakness on the way.” For example, commodity prices and equities are likely to drag the index down further based on the developments in September.

Westpac doesn’t expect RBA to make any change to policy settings until February next year. It expects asset purchases to be fully wound back by May/August next year.

Fed not ready for tapering yet, some previews

No change in policy is expected from FOMC today and Fed is likely not ready to announce tapering yet. Chair Jerome Powell would just reiterate that “substantial further progress” has been “met for inflation”, and there has also been “clear progress toward maximum employment”. Also, it’s appropriate to start tapering “if the economy evolved broadly as anticipated

A major focus in the median dot plot, where two rate hikes were penciled in by 20223. For 2022, there were 7 out of 18 participants anticipating one or two hikes. The overall picture could tilt towards the hawkish side if just one or two members bring forward their rate forecasts to 2022. Meanwhile, the new staff economic projections will catch some attention too.

Here are some suggested readings on Fed:

- FOMC Preview: Fed to Affirm Tapering Could Come This Year. Focus Turns to Dot Plot

- Fed Meeting: Forget the Slow Crawl to Tapering, it’s the Dot Plot that Matters

- FOMC Meeting Preview: Will We Get A Taper Hint?

- Fed Research – Preview: What to Do in a Bad Trade-Off?

- Musical Chairs at the Fed: Powell or Brainard?

On the data front

Eurozone consumer confidence and existing home sales will also be released.

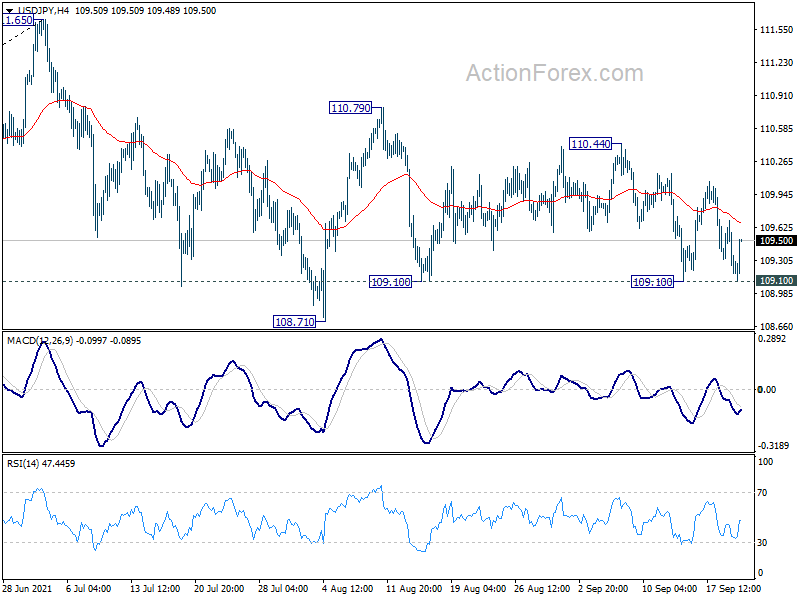

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.04; (P) 109.37; (R1) 109.56; More…

Once again, USD/JPY drew support from 109.10 and recovered. Intraday bias remains neutral first as range trading could continue. On the downside, break of 109.10 will argue that larger fall from 111.65 is resuming. Deeper decline should then be seen to 108.71 support first, and then 38.2% retracement of 102.58 to 111.65 at 108.18 next. On the upside, above 110.44 will turn bias back to the upside for 110.79, and then 111.65 high.

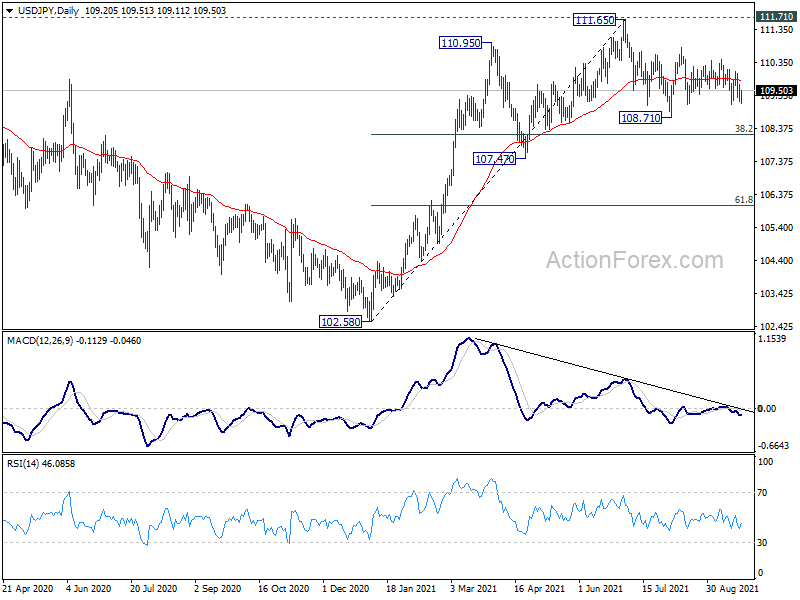

In the bigger picture, medium term outlook is staying neutral with 111.71 resistance intact. The pattern from 101.18 could still extend with another falling leg. Sustained trading below 55 day EMA will bring deeper fall to 107.47 support and below. Nevertheless, strong break of 111.71 resistance will confirm completion of the corrective decline from 118.65 (2016 high). Further rise should then be seen to 114.54 and then 118.65 resistance.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:30 | AUD | Westpac Leading Index M/M Aug | -0.30% | -0.10% | ||

| 3:00 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 13:00 | CHF | SNB Quarterly Bulletin Q3 | ||||

| 14:00 | EUR | Eurozone Consumer Confidence Sep P | -6 | -5 | ||

| 14:00 | USD | Existing Home Sales Aug | 5.89M | 5.99M | ||

| 14:30 | USD | Crude Oil Inventories | -6.4M | |||

| 18:00 | USD | Fed Interest Rate Decision | 0.25% | 0.25% |

{kind=link}