Yen’s selloff continues to look unstoppable as global markets are set to end the week on a strong note. Asian stocks are trading broadly higher following the solid rebound in the US overnight. Dollar is also weak, partly weighed down by the extended retreat in treasury yields, but Euro is not too far away. Commodity currencies are set to end the week as the strongest, and it’s just a matter of who’s among Loonie, Aussie and Kiwi would be the eventual winner.

Technically, NASDAQ’s break above 55 day EMA affirms the case that correction from 15403.43 has completed at 14181.69, after drawing support from 14175.11. A strong close today would help set the stage for further rally to retest 15403.43 high later in the month. Such development could continue to pressure Yen ahead, while capping Dollar’s rally elsewhere.

In Asia, at the time of writing, Nikkei is up 1.36%. Hong Kong HSI is up 0.83%. China Shanghai SSE is up 0.29%. Singapore Strait Times is up 0.39%. Japan 10-year JGB yield is down -0.0010 at 0.084. Overnight, DOW rose 1.56%. S&P 500 rose 1.71%. NASDAQ rose 1.73%. 10-year year dropped -0.030 to 1.519.

Fed Harker not expecting rate hike until late 2022 or early 2023

Philadelphia Fed President Patrick Harker said yesterday he’s in the camp that believes it will “soon be time” to start tapering asset purchases “begin slowly and methodically — frankly, boringly”.

He added that FOMC can then evaluate interest rates after tapering is complete. “I wouldn’t expect any hikes to interest rates until late next year or early 2023, unless the inflation picture changes dramatically,” he said.

Harker expects the economy to grow by 5.5% this year and 3.5% next. Inflation is expected to be around 4% for 2021, “a bit over” 2% in 2022, and “right at” 2% in 2023.

BoC Macklem: Inflation probably taking a little longer to come back down

BoC Governor Tiff Macklem said yesterday that supply bottlenecks are “not easing as quickly as expected”. Global inflation is “probably going to take a little longer to come back down”.

But he also added, the central bank’s job is “to make sure that these one-off price increases don’t become ongoing inflation.” He maintained, “there’s good reasons to believe that these are one-off price increases. They won’t create ongoing inflation.”

On the job market, Macklem said returning to the prepandemic employment level “is an important milestone, but it’s not the destination”. He added, “it is still the case though that low-wage workers are well below their prepandemic level, whereas other workers have slowly recovered. So there still is some space there.”

Japan Cabinet Office said exports increasing at a slower pace

In the October Monthly Economic Report, Japan’s Cabinet Office downgraded assessment on exports to “increasing at a slower pace”, from “continue to increase moderate”. That’s the first downgrade in seven months.

Overall, the economy is “picking up although the pace has weakened in a severe situation due to the Novel Coronavirus.” Private consumption “shows weakness further”. Business investment is “picking up”. Industrial production is “picking up”. Corporate profits are “picking up”. Employment situation “shows steady movements in some components”. Consumer prices show “steady movements”.

As the government lifted state emergency, it will “develop a new economic stimulus package” to address the issues of reopening. It expects BoJ to “pay careful attention to the economic impact of the infections and conduct appropriate monetary policy management”.

New Zealand BusinessNZ manufacturing rebounded to 51.4

New Zealand BusinessNZ Performance of Manufacturing rebounded strongly from 39.7 to 51.4 in September. Looking at some more details, production rose from 27.2 to 49.9. Employment ticked up from 54.3 to 54.5. New orders rose from 44.1 to 54.3. Finished stocks rose from 45.9 to 50.1. Deliveries also jumped from 33.1 to 47.8.

BNZ Senior Economist, Craig Ebert stated that “the rebound the PMI experienced in September was encouraging, although the survey is not without some still‐frayed parts. Credit where it’s due though, as the NZ PMI traced much less of a contraction, and quicker stabilisation, compared to what it went through during the initial outbreak of COVID‐19.”

Looking ahead

Eurozone trade balance is the only feature in European session. Main focus will be on US retail sales later in the day. Empire state manufacturing, import price, business inventories will also be released.

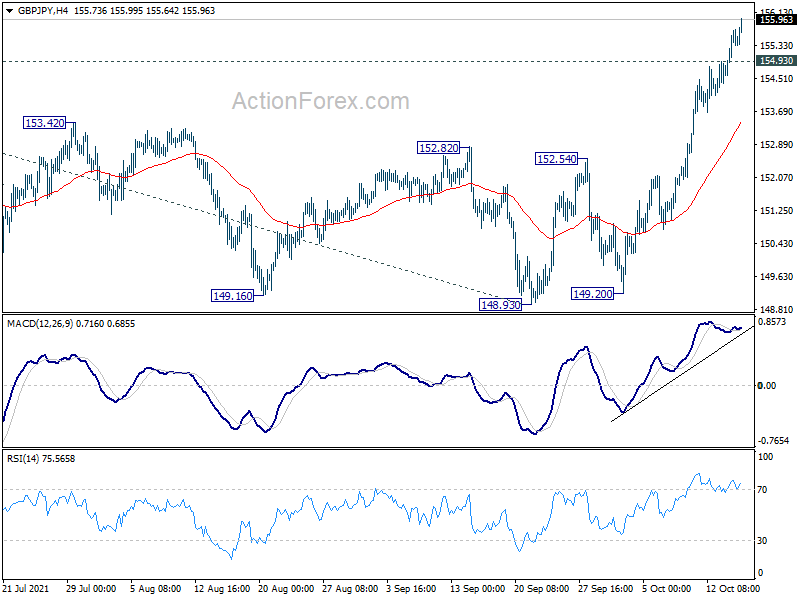

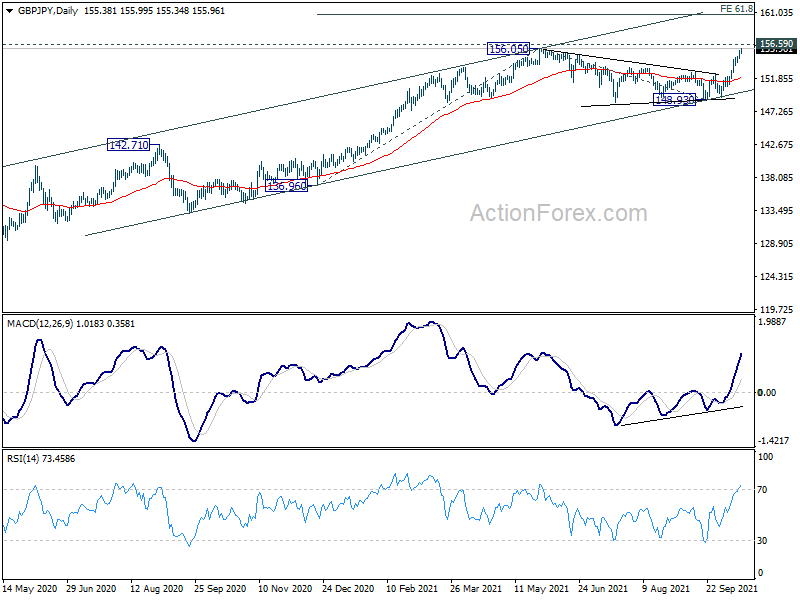

GBP/JPY Daily Outlook

Daily Pivots: (S1) 154.80; (P) 155.27; (R1) 155.91; More…

GBP/JPY rises to as high as 155.98 so far today and intraday bias stays on the upside. Decisive break of 156.05/59 key resistance zone will carry larger bullish implications. Medium term up trend from 123.94 should then target 61.8% projection of 136.96 to 156.05 from 148.93 at 160.72. On the downside, below 154.93 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, rise from 123.94 is seen as the third leg of the pattern from 122.75 (2016 low), which is still in progress. Sustained break of 156.59 (2018 high) would affirm the case of long term bullish reversal, and pave the way to 61.8% retracement 195.86 (2015 high) to 122.75 at 167.93 next. For now, this will be the favored case as long as 148.93 structural support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | BusinessNZ Manufacturing Index Sep | 51.4 | 40.1 | ||

| 04:30 | JPY | Tertiary Industry Index M/M Aug | -1.7% | -0.30% | -0.60% | |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Aug | 15.3B | 13.4B | ||

| 12:30 | USD | Empire State Manufacturing Index Oct | 27.8 | 34.3 | ||

| 12:30 | USD | Retail Sales M/M Sep | -0.20% | 0.70% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Sep | 0.40% | 1.80% | ||

| 12:30 | USD | Import Price Index M/M Sep | 0.50% | -0.30% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Oct F | 73.5 | 72.8 | ||

| 14:00 | USD | Business Inventories Aug | 0.70% | 0.50% |

{kind=link}