European majors turn generally softer today, in particular, with Sterling paring some gains after strong but lower than expected consumer inflation data. Dollar also weakens with treasury yield dipping slightly while Yen is trying to recover. But overall, Kiwi and Aussie maintain their position as the best performer. US futures are pointing to a flat open but buyers could jump in again later in the day. Development in the stock markets should continue to lead currencies.

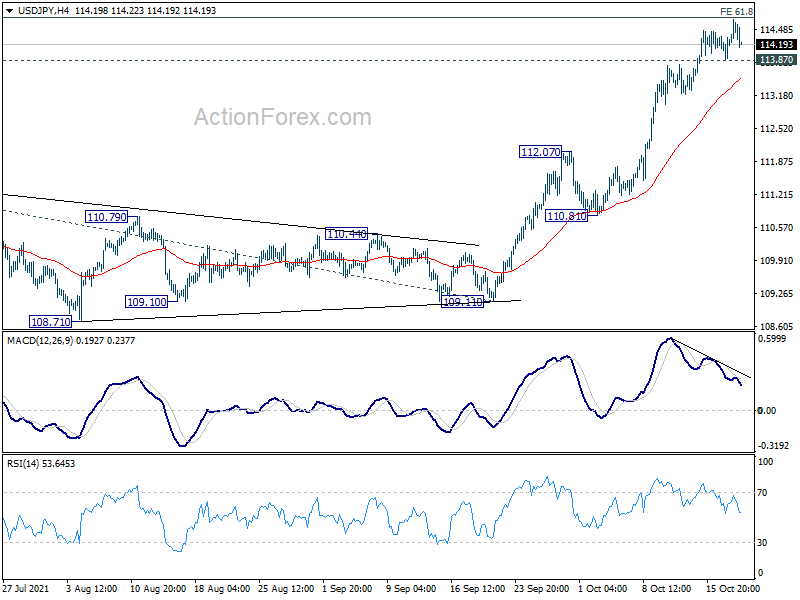

Technically, USD/JPY continues to lose upside momentum just ahead of 114.71 fibonacci projection level. Break of 113.87 minor support should indicate short term topping and bring deeper pull back to 4 hour 55 EMA (now at 113.49) and below. If that happens, we’ll see if EUR/JPY and GBP/JPY would break 132.13 and 156.58 support levels together. Together, they would signal that Yen crosses are generally turning into near term consolidations after recent strong rallies.

In Europe, at the time of writing, FTSE is down -0.07%. DAX is down -0.11%. CAC is down -0.01%. Germany 10-year yield is down -0.0205 at -0.123. Earlier in Asia, Nikkei rose 0.14%. Hong Kong HSI rose 1.35%. China Shanghai SSE dropped -0.17%. Singapore Strait Times dropped -0.03%. Japan 10-year JGB yield rose 0.0048 to 0.095.

Canada CPI rose to 4.4% yoy in Sep, highest since 2003

Canada CPI accelerated to 4.4% yoy in September, up from August’s 4.1% yoy, above expectation of 4.3% yoy. That’s the fastest pace since 2003. Excluding gasoline CPI rose 0.3% yoy.

CPI common was unchanged at 1.8% yoy, below expectation of 1.9% yoy. CPI median rose to 2.8% yoy, up from 2.6% yoy, above expectation of 2.6% yoy. CPI trimmed rose to 3.4% yoy, up from 3.3% yoy, above expectation of 3.3% yoy.

Bundesbank Weidmann: It’s crucial not to lose sign of prospective inflationary dangers

Bundesbank President Jens Weidmann warned, “it will be crucial not to look one-sidedly at deflationary risks, but not to lose sight of prospective inflationary dangers either.” The comment came as Weidmann announced he’s stepping down from the post on December 31, as “more than 10 years is a good measure of time to turn over a new leaf – for the Bundesbank, but also for me personally.”

ECB President Christine Lagarde said in statement, “I respect Jens Weidmann`s decision to step down from his position as President of Deutsche Bundesbank at the end of this year after more than 10 years of service, but I also immensely regret it.”

Eurozone CPI finalized at 3.4% yoy in Sep, EU at 3.6% yoy

Eurozone CPI was finalized at 3.4% yoy in September, up from August’s 3.0% yoy. The highest contribution to the annual euro area inflation rate came from energy (+1.63 percentage points, pp), followed by services (+0.72 pp), non-energy industrial goods (+0.57 pp) and food, alcohol & tobacco (+0.44 pp).

EU CPI was finalized at 3.6% yoy, up from August’s 3.2% yoy. The lowest annual rates were registered in Malta (0.7%), Portugal (1.3%) and Greece (1.9%). The highest annual rates were recorded in Estonia, Lithuania (both 6.4%) and Poland (5.6%). Compared with August, annual inflation fell in one Member State, remained stable in one and rose in twenty-five.

Also released, Eurozone current account surplus came in at EUR 13.4B, versus expectation of EUR 24.3B. Germany PPI was at 2.3% mom, 14.2% yoy in September, versus expectation of 1.0% mom, 12.7% yoy.

UK CPI slowed to 3.1% in Sep, core CPI dropped to 2.9% yoy

UK CPI slowed to 3.1% yoy in September, down from 3.2% yoy, below expectation of 3.2% yoy. Core CPI also dropped to 2.9% yoy, down from 3.1% yoy, below expectation of 2.9% yoy. RPI, on the other hand rose to 4.9% yoy, up from 4.8% yoy, above expectation of 4.7% yoy.

Also released, PPI input came in at 0.4% mom, 11.4% yoy, versus expectation of 0.8% mom, 11.6% yoy. PPI output was at 0.5% mom, 6.7% yoy, versus expectation of 0.9% mom, 6.8% yoy. PPI output core was at 0.5% mom, 5.9% yoy, versus expectation of 0.9% mom, 5.8% yoy.

Australia Westpac leading index turned negative, but rebound expected ahead

Australia Westpac-MI Leading Index dropped from 0.5% to -0.5% in September. That’s the first negative reading since September 2020, which was the followed by strong surge after the economy moved out of lockdown. Westpac expects another strong rebound in the economy ahead as both Sydney and Melbourne are reopening this time too. It also expects the Australia economy to growth by 1.6% in Q4, building towards a 5.6% growth in H2 of 2022.

Westpac expects RBA to maintain current policy setting at the November 2 meeting, followed by tapering in February. The most important aspect of the November meeting will be whether RBA has lifted its inflation forecasts.

Japan exports rose 13% yoy in Sep, imports rose 38.6% yoy

Japan’s exports rose 13.0% yoy to JPY 6481B in September, above expectation of 11.0% yoy. Imports rose 38.6% yoy to JPY 7464B, above expectation of 34.4% yoy. Trade balance reported JPY -623B deficit, versus expectation of JPY -519B.

The weakening in exports could be partly attributed to the -40.3% yoy decline in car shipments, first in seven months. But the situation is expected to improve as supply bottlenecks are solved. Shipment to China grew 10.3% yoy, led by semiconductors and plastic materials. Shipment to the US dropped -3.3% yoy, on cars and airplanes.

In seasonally adjusted terms, exports dropped -3.9% mom to JPY 6750B. Imports rose 0.2% mom to JPY 7375B. Trade deficit came in at JPY -625B.

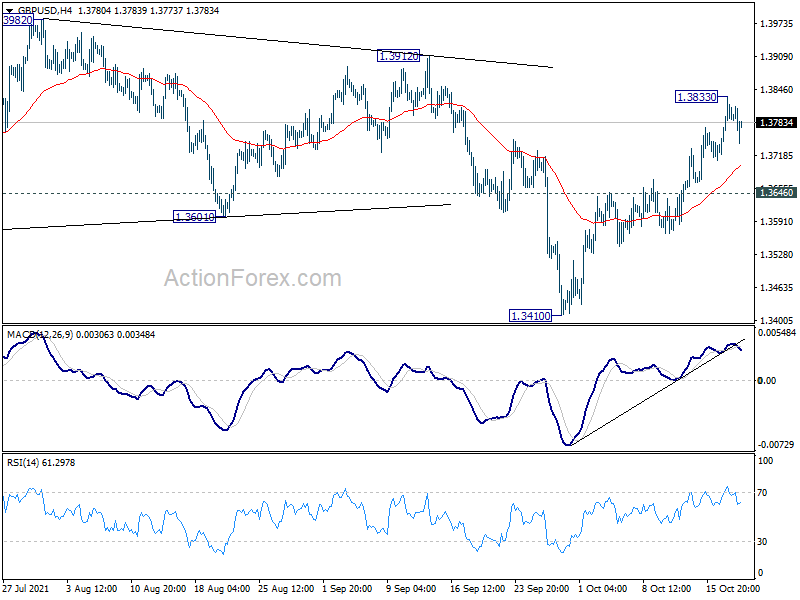

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3733; (P) 1.3783; (R1) 1.3842; More…

A temporary top is formed at 1.3833 in GBP/USD with current retreat and intraday bias is turned neutral first. Some consolidations could be seen. But further rise is in favor as long as 1.3646 support holds. Above 1.3833 will resume the rebound from 1.3410 to 1.3912 key structural resistance. Firm break there will indicate that the correction from 1.4248 is complete with three waves down to 1.3410. Further rally would then be seen to retest 1.4248 high. However, break of 1.3646 will turn bias to the downside for retesting 1.3410 low.

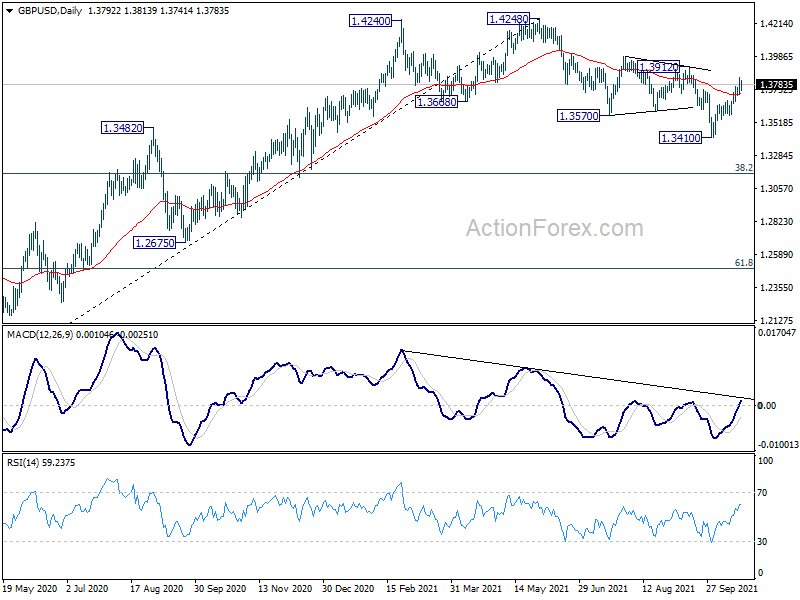

In the bigger picture, the structure of the fall from 1.4248 suggests that it’s a correction to the up trend from 1.1409 (2020 low) only. While deeper fall cannot be ruled out yet, downside should be contained by 38.2% retracement of 1.1409 to 1.4248 at 1.3164, at least on first attempt, to bring rebound. On the upside, firm break of 1.4376 key resistance (2018 high) will add to the case of long term bullish reversal. However, sustained trading below 1.3164 will revive some medium term bearishness and target 61.8% retracement at 1.2493.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Leading Index M/M Sep | 0.00% | -0.30% | ||

| 23:50 | JPY | Trade Balance (JPY) Sep | -0.62T | -0.53T | -0.27T | -0.34T |

| 06:00 | EUR | Germany PPI M/M Sep | 2.30% | 1.00% | 1.50% | |

| 06:00 | EUR | Germany PPI Y/Y Sep | 14.20% | 12.70% | 12.00% | |

| 06:00 | GBP | CPI M/M Sep | 0.30% | 0.40% | 0.70% | |

| 06:00 | GBP | CPI Y/Y Sep | 3.10% | 3.20% | 3.20% | |

| 06:00 | GBP | Core CPI Y/Y Sep | 2.90% | 3.10% | 3.10% | |

| 06:00 | GBP | RPI M/M Sep | 0.40% | 0.20% | 0.60% | |

| 06:00 | GBP | RPI Y/Y Sep | 4.90% | 4.70% | 4.80% | |

| 06:00 | GBP | PPI Input M/M Sep | 0.40% | 0.80% | 0.40% | 0.50% |

| 06:00 | GBP | PPI Input Y/Y Sep | 11.40% | 11.60% | 11.00% | 11.20% |

| 06:00 | GBP | PPI Output M/M Sep | 0.50% | 0.90% | 0.70% | |

| 06:00 | GBP | PPI Output Y/Y Sep | 6.70% | 6.80% | 5.90% | 6.00% |

| 06:00 | GBP | PPI Core Output M/M Sep | 0.50% | 0.90% | 1.00% | 0.90% |

| 06:00 | GBP | PPI Core Output Y/Y Sep | 5.90% | 5.80% | 5.30% | 5.40% |

| 08:00 | EUR | Eurozone Current Account (EUR) Aug | 13.4B | 24.3B | 21.6B | |

| 09:00 | EUR | Eurozone CPI Y/Y Sep F | 3.40% | 3.40% | 3.40% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Sep F | 1.90% | 1.90% | 1.90% | |

| 12:30 | CAD | CPI M/M Sep | 0.20% | 0.10% | 0.20% | |

| 12:30 | CAD | CPI Y/Y Sep | 4.40% | 4.30% | 4.10% | |

| 12:30 | CAD | CPI Common Y/Y Sep | 1.80% | 1.90% | 1.80% | |

| 12:30 | CAD | CPI Median Y/Y Sep | 2.80% | 2.60% | 2.60% | |

| 12:30 | CAD | CPI Trimmed Y/Y Sep | 3.40% | 3.30% | 3.30% | |

| 14:30 | USD | Crude Oil Inventories | 2.1M | 6.1M | ||

| 18:00 | USD | Fed’s Beige Book |

{kind=link}