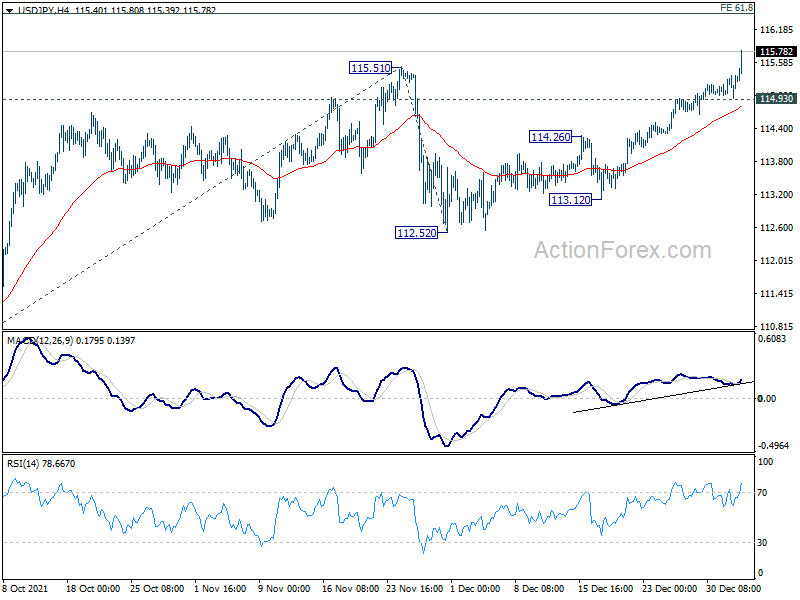

Yen selloff is the main theme in the Asian markets today, in particular as USD/JPY breaks out on the upside with acceleration. The move was fueled by strong rally in US treasury yields overnight, as well as rally in Nikkei and benchmark JGB yield. Dollar is currently the strongest one for the, reversing much of the pre-holiday decline. Commodity currencies are also slightly firmer, but we’ll see if Europeans could outperform them.

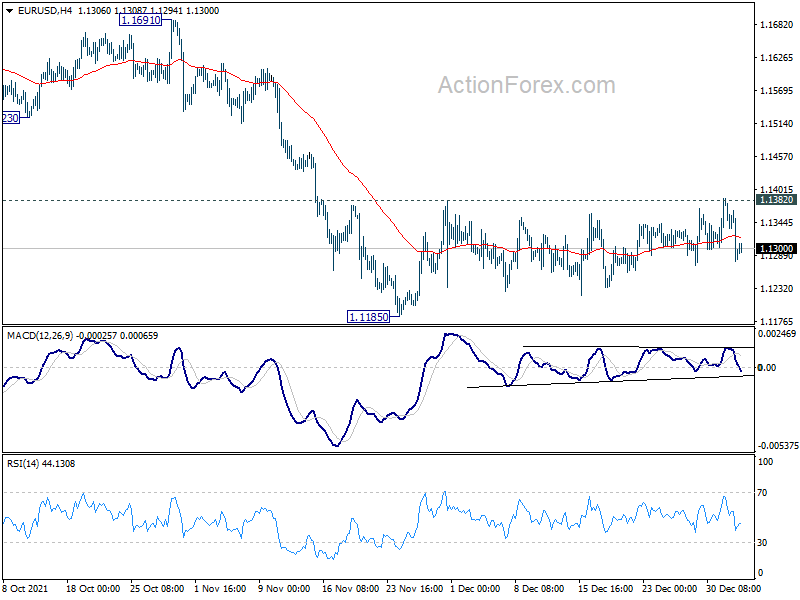

Technically, in addition to Yen crosses, we’d also pay attention to EUR/USD. It was knocked off by 1.1382 resistance despite a very brief breach during illiquid holiday markets. EUR/USD could be heading back to retest 1.1185 support and break will resume larger down trend. Such development, if happens, could affirm the case that Dollar is really on the move.

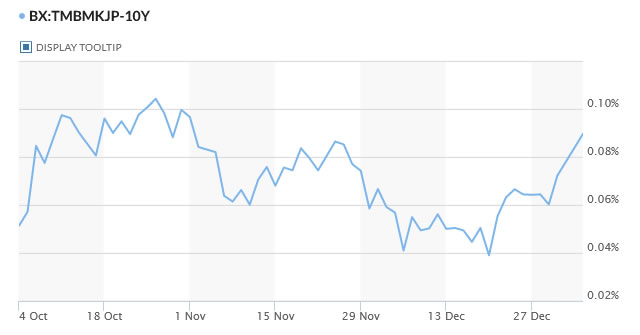

In Asia, at the time of writing, Nikkei is up 1.71%. Hong Kong HSI is down -0.29%. China Shanghai SSE is down -0.35%. Singapore Strait Times is up 1.22%. Japan 10-year JGB yield is up 0.0174 at 0.090. Overnight, DOW rose 0.68%. S&P 500 rose 0.64%. NASDAQ rose 1.20%. 10-year yield rose 0.116 to 1.628.

US 10-yr yield back above 1.6, 30-yr yield above 2.0

US treasury yields surged sharply overnight as investors continued to adjust themselves “living with the virus”. Omicron is now generally taken as being much less harmful to the global economy as initially feared, despite record infection numbers.

10-year yield closed up 0.116 to 1.628, back above 1.6 handle for the first time since November. We’re holding on to the view that consolidation pattern from 1.765 has complete with three waves at 1.343. TNX could accelerate upwards in the near term to 1.693 resistance. Firm break there would send TNX through 1.765 to resume larger up trend from 0.398 (2020 low).

The picture in 30-year yield is similar. It’s now back above 2.0 handle after yesterday’s rise. Corrective pattern from 2.505 should have completed with three waves down to 1.678. Further rally should be seen to 2.177 in the near term. Sustained break there will raise the chance that it’s already resuming the up trend from 0.837 (2020 low) through 2.505 high.

China Caixin PMI manufacturing rose to 50.9, improving demand and supply

China Caixin PMI Manufacturing rose to 50.9 in December, up from November’s 49.9, above expectation of 50.0. The data signaled a renewed improvement in the sector with best reading since June. Caixin said rise in output was stronger amid renewed upturn in sales. Input cost inflation eased to 19-month low. Business confidence weakened amid pandemic and supply chain worries.

Wang Zhe, Senior Economist at Caixin Insight Group said: “To sum up, manufacturing demand and supply improved in December with easing inflationary pressure. But the job market was still under pressure and businesses were less optimistic, indicating unstable economic recovery. The repeated Covid-19 flare-ups and sluggish overseas demand were factors of instability.”

Japan PMI manufacturing finalized at 54.3 in Dec, confidence dipped

Japan PMI Manufacturing was finalized at 54.3 in December, slightly lower than November’s 54.5. But that was well above 2021’s average of 52.7. Markit said output and new orders increased at slower rates. Employment level rose at fastest pace in nearly four years. Business optimism eased to four-month low.

Usamah Bhatti, Economist at IHS Markit, said: “Domestic markets were buoyed by a gradual recovery from the COVID-19 pandemic however a sharp rise in cases, particularly in South Korea hindered international demand and continued to disrupt supply chains across the sector… Delivery delays and material shortages remained a dampener on production and sales… Average lead times across the final quarter of 2021 deteriorated further… Though still optimistic, Japanese goods producers were wary of the continued impact of the pandemic and supply chain disruption, which resulted in confidence dipping to the softest since August.”

Looking ahead

Germany retail sales, and unemployment will be released in European session. Swiss will release CPI while UK will release mortgage approvals, M4 money supply and PMI manufacturing final.

Later in the day, Canada will release IPPI and RMPU. US will release ISM manufacturing.

FOMC minutes, ISMs and NFP to return to focus

Minutes of the December FOMC meeting will be a major focus this week. At the meeting, Fed announced that it would speed up tapering and end it in March instead of June. Also, the new projections saw three rate hikes this year. The markets would like to see more in-depth information an related discussion.

Meanwhile, US will also release ISM indexes and non-farm payrolls, Eurozone CPI flash and Canada employment, China Caixin PMIs will be among most anticipated data release.

Here are some highlights for the week:

- Tuesday: Japan PMI Manufacturing final; China Caixin PMI manufacturing; Germany retail sales, unemployment; Swiss CPI; UK PMI manufacturing final, mortgage approvals, M4 money supply; Canada IPPI and RMPI; US ISM manufacturing.

- Wednesday: Japan monetary base, consumer confidence; Eurozone PMI services final; US ADP employment, FOMC minutes; Canada building permits.

- Thursday: China Caixin PMI services; Germany factory orders, CPI flash; UK PMI services final; Eurozone PPI; Canada trade balance; US Challenger job cuts, jobless claims, trade balance; ISM services, factory orders.

- Friday: Japan average cash earnings, household spending, Tokyo CPI core; Swiss unemployment rate, retail sales, currency reserves; Germany industrial production, trade balance; France consumer spending, industrial production, trade balance; UK PMI construction; Eurozone PMI flash, retail sales; Canada employment, Ivey PMI US non-farm payrolls.

USD/JPY Daily Outlook

Daily Pivots: (S1) 115.08; (P) 115.22; (R1) 115.50; More…

USD/JPY rises to as high as 115.80 so far today and the strong break of 115.51 resistance confirms resumption of whole up trend from 102.58. Intraday bias stays on the upside for 61.8% projection of 109.11 to 115.51 from 112.52 at 116.47. Firm break there will target 100% projection at 118.90, which is close to 118.65 long term resistance. On the downside, break of 114.93 will turn intraday bias neutral and bring some consolidations, before staging another rally.

In the bigger picture, no change in the view that rise from 102.58 is the third leg of the up trend from 101.18 (2020 low). Such rally should target a test on 118.65 (2016 high). Sustained break there will pave the way to 112.85 (2015 high) and raise the chance of long term up trend resumption. For now, this will remain the favored case as long as 112.52 support holds, in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:01 | GBP | BRC Shop Price Index Y/Y Nov | 0.80% | 0.30% | ||

| 00:30 | JPY | Manufacturing PMI Dec F | 54.3 | 54.2 | 54.2 | |

| 01:45 | CNY | Caixin Manufacturing PMI Dec | 50.9 | 50.5 | 49.9 | |

| 07:00 | EUR | Germany Retail Sales M/M Nov | -0.50% | -0.30% | ||

| 07:30 | CHF | CPI M/M Dec | -0.10% | 0.00% | ||

| 07:30 | CHF | CPI Y/Y Dec | 1.60% | 1.50% | ||

| 08:55 | EUR | Germany Unemployment Change Dec | -15K | -34K | ||

| 08:55 | EUR | Germany Unemployment Rate Dec | 5.30% | 5.30% | ||

| 09:30 | GBP | Mortgage Approvals Nov | 66K | 67K | ||

| 09:30 | GBP | M4 Money Supply M/M Nov | 0.50% | 0.60% | ||

| 09:30 | GBP | Manufacturing PMI Dec F | 57.6 | 57.6 | ||

| 13:30 | CAD | Industrial Product Price M/M Nov | 0.90% | 1.30% | ||

| 13:30 | CAD | Raw Material Price Index Nov | 0.00% | 4.80% | ||

| 14:30 | CAD | Manufacturing PMI Dec | 57.2 | |||

| 15:00 | USD | ISM Manufacturing PMI Dec | 60.2 | 61.1 | ||

| 15:00 | USD | ISM Manufacturing Prices Paid Dec | 79.5 | 82.4 | ||

| 15:00 | USD | ISM Manufacturing Employment Dec | 53.3 |

{kind=link}