Even though the US markets were in deep selloff overnight, Asian markets are just mixed. Investors are still waiting for come clarity on the Russia-Ukraine situation before taking a committed move. Trading is also subdued ahead of a long weekend in the US, with a holiday on Monday. In the currency markets, Aussie and Kiwi are currently the strongest ones for the week. Dollar, Euro and Yen are the worst performing. But the picture could easily change if something dramatic happens.

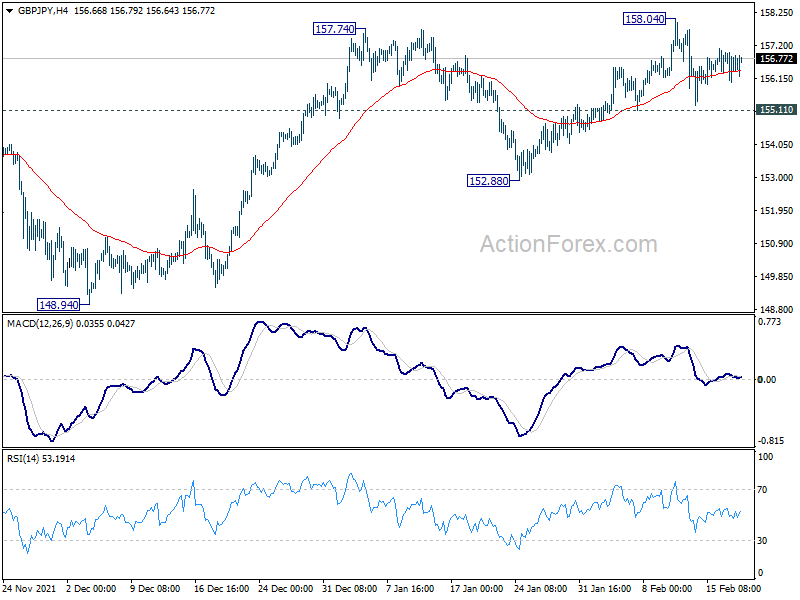

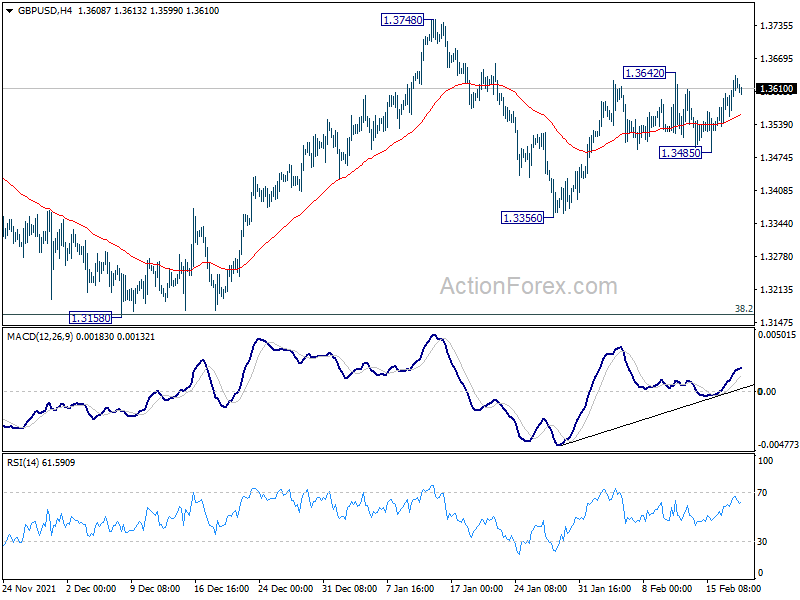

Technically, GBP/USD would be a focus today, with retail sales data featured. Break of 1.3642 will resume the rise from 1.3356 to 1.3748 resistance further break there will revive the case of bullish reversal, and could set the stage for retesting 1.4248 high at a later stage. Meanwhile, GBP/JPY is also rather resilient in spite of geopolitical uncertainties. Break of 158.04/19 resistance zone will confirm even confirm resumption of medium term up trend for next.

In Asia, at the time of writing, Nikkei is down -0.18%. Hong Kong HSI is down -0.48%. China Shanghai SSE is up 0.02%. Singapore Strait Times is up 0.05%. Japan 10-year JGB yield is down -0.0016 at 0.222. Overnight, DOW dropped -1.78%. S&P 500 dropped -2.12%. NASDAQ dropped -2.88%. 10-year yield dropped -0.075 to 1.972.

Fed Bullard: We’re at risk that inflation won’t dissipate

St. Louis Federal Reserve President James Bullard warned during a panel talk at Columbia University, “we’re at more risk now than we’ve been in a generation that this (inflation) could get out of control.”

One scenario would be, “a new surprise that hits us that we can’t anticipate right now, but we would have even more inflation,” he said. “That’s the kind of situation that we want to … make sure it doesn’t occur.”

“Overall, I’d say there’s been too much emphasis and too much mindshare devoted to the idea that inflation will dissipate at some point in the future,” Bullard said. “We’re at risk that inflation won’t dissipate, and 2022 will be the second year in a row of quite high inflation. So that’s why given this situation, the Fed should move faster and more aggressively than we would have in other circumstances.”

Fed Mester: Appropriate to hike in March, and follow with further increases in coming months

Cleveland Fed President Loretta Mester said yesterday, “I believe it will be appropriate to move the funds rate up in March and follow with further increases in the coming months.”

“If by mid-year, I assess that inflation is not going to moderate as expected, then I would support removing accommodation at a faster pace over the second half of the year,” she added.

Mester still expects inflation to remain above 2% this year and next. Moderation in inflation is “conditioned on the FOMC taking appropriate action to transition away from the current emergency levels of accommodation.”

“We will need to convey the overall trajectory of policy and give the rationale for our policy decisions based on our assessment of the outlook and risks around the outlook, which are informed by economic and financial developments,” Mester said. “This change in communications will provide a better sense of the FOMC’s policy reaction function and should not be interpreted as the FOMC backing away from transparency.”

Japan CPI core slowed to 0.2% yoy in Jan, CPI core core dropped to -1.1% yoy

Japan all item CPI slowed from 0.8% yoy to 0.5% yoy in January, below expectation of 0.6% yoy. CPI core (all item less fresh food) dropped from 0.5% yoy to 0.2% yoy, below expectation of 0.3% yoy. CPI core-core (all item less fresh food and energy), dropped from -0.7% yoy to -1.1% yoy, below expectation of -0.7% yoy.

Finance Minister Shunichi Suzuki said recent prices rises were “driven mostly by increases in energy costs”, though forex moves also has had some impact. He added, “if inflation rises before improvement in job market, wage hikes kick in, that could affect consumption.”

Elsewhere

New Zealand PPI input rose 1.1% qoq in Q4, below expectation of 1.6% qoq. PPI output rose 1.4% qoq, below expectation of 2.3% qoq.

UK retail sales and Eurozone current account will be featured in European session. Later in the day, Canada will release retail sales and new housing price index. US will release existing home sales.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3567; (P) 1.3603; (R1) 1.3649; More…

Intraday bias in GBP/USD remains neutral for the moment, and focus stays on 1.3642 resistance. Break there will resume the rebound from 1.3356 to 1.3748 resistance. Firm break there will revive the bullish case that correction from 1.4248 has completed with three waves down to 1.3158. Further rally should then be seen to retest 1.4248 high. On the downside, though, break of 1.3485 will turn bias to the downside for 1.3356 support instead.

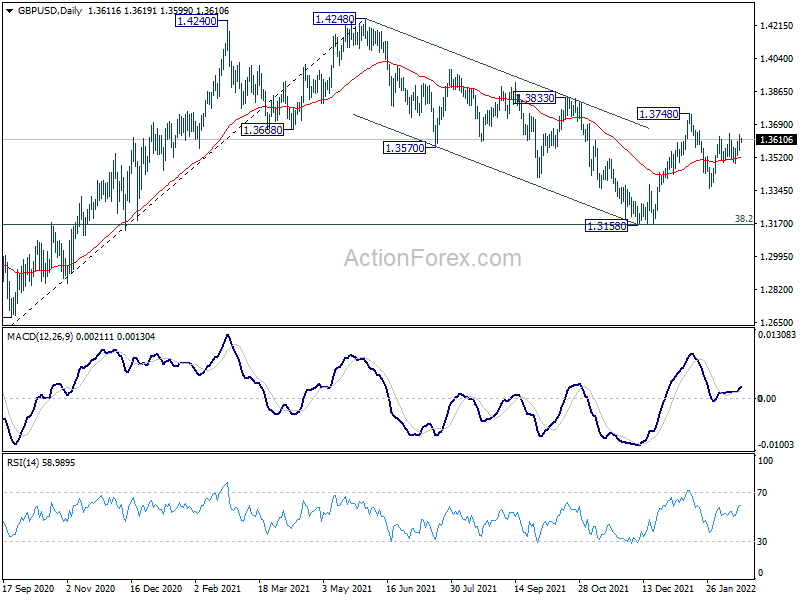

In the bigger picture, as long as 38.2% retracement of 1.1409 to 1.4248 at 1.3164 holds, up trend from 1.1409 (2020 low) is still in progress. On resumption, next target will be 38.2% retracement of 2.1161 to 1.1409 at 1.5134. Nevertheless sustained break of 1.3164 will argue that whole rise from 1.1409 has completed and bring deeper fall to 61.8% retracement at 1.2493.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | PPI Input Q/Q Q4 | 1.10% | 1.60% | 1.60% | |

| 21:45 | NZD | PPI Output Q/Q Q4 | 1.40% | 2.30% | 1.80% | |

| 23:30 | JPY | National CPI Core Y/Y Jan | 0.20% | 0.30% | 0.50% | |

| 07:00 | GBP | Retail Sales M/M Jan | 1.00% | -3.70% | ||

| 07:00 | GBP | Retail Sales Y/Y Jan | 8.70% | -0.90% | ||

| 07:00 | GBP | Retail Sales ex-Fuel M/M Jan | 1.20% | -3.60% | ||

| 07:00 | GBP | Retail Sales ex-Fuel Y/Y Jan | 7.90% | -3.00% | ||

| 09:00 | EUR | Eurozone Current Account (EUR) Dec | 24.3B | 23.6B | ||

| 13:30 | CAD | New Housing Price Index M/M Jan | 0.50% | 0.20% | ||

| 13:30 | CAD | Retail Sales M/M Dec | -2.10% | 0.70% | ||

| 13:30 | CAD | Retail Sales ex Autos M/M Dec | -2.10% | 1.10% | ||

| 15:00 | USD | Existing Home Sales Jan | 6.12M | 6.18M | ||

| 15:00 | EUR | Eurozone Consumer Confidence Feb P | -8 | -9 |

{kind=link}