Dollar’s broad based rally continues into US session. The unexpected contraction of Q1 US GDP might give the greenback a little jitter. But it’s unlikely to alter the up trend for now. As for today, Canadian Dollar is the second strongest Yen is the worst performing one on post-BoJ selloff. But Kiwi and Sterling also also weak. Euro and Swiss Fran are mixed together with Aussie.

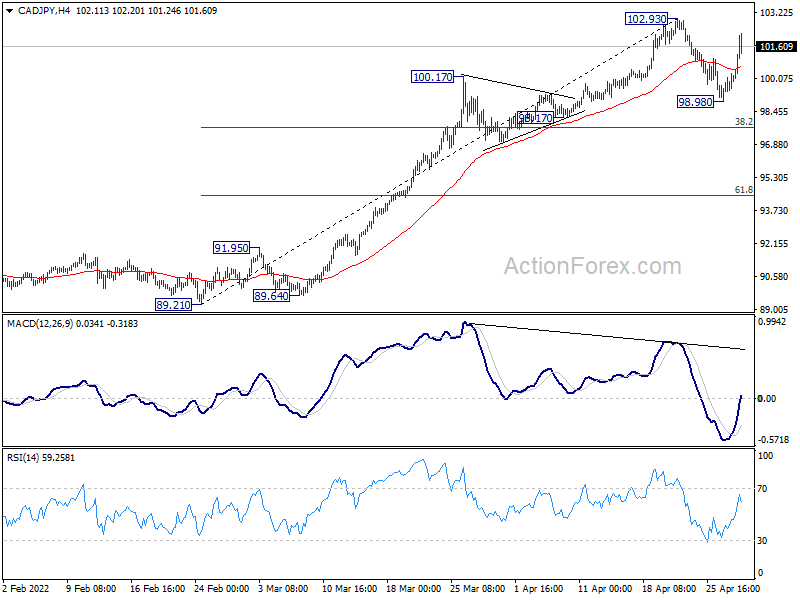

Technically, as Yen is back under pressure, some focus will be on CAD/JPY. The pull back from 102.93 should have completed at 98.98 already. Retest of 102.93 should be seen next and break will resume larger up trend. That could be a sign of more broad based selling in Yen, the should be followed by break of 95.73 high in AUD/JPY and 139.99 high in EUR/JPY.

In Europe, at the time of writing, FTSE is up 0.85%. DAX is up 1.38%. CAC is up 1.22%. Germany 10-year yield is up 0.079 at 0.883. Earlier in Asia, Nikkei rose 1.75%. Hong Kong HSI rose 1.65%. China Shanghai SSE rose 0.58%. Singapore Strait Times rose 0.43%. Japan 10-year JGB yield dropped -0.0307 to 0.219.

US GDP dropped -1.4% annualized in Q1, first contraction since Q2 2020

US GDP unexpectedly contracted -1.4% annualized in Q1, much worse than expectation of 1.1% growth. That’s also the first contraction reading since Q2 2020.

The decrease in real GDP reflected decreases in private inventory investment, exports, federal government spending, and state and local government spending, while imports, which are a subtraction in the calculation of GDP, increased. Personal consumption expenditures (PCE), nonresidential fixed investment, and residential fixed investment increased.

US initial jobless claims dropped to 180k, continuing claims down to 1.408m

US initial jobless claims dropped -5k to 180k in the week ending April 23, slightly above expectation of 178k. Four-week moving average of initial claims rose 2k to 180k.

Continuing claims dropped -1k to 1408k in the week ending April 16. That’s the lowest level since February 7, 1970, when it was 1397k. Four-week moving average of continuing claims dropped -24.5k to 1455k, lowest since March 14, 1970 when it was 1435k.

ECB de Guindos: Russia invasion casts a dark shadow over Europe

In remarks to a Committee of the European Parliament, ECB Vice President Luis de Guindos said, Russian invasion of Ukraine has “cast a dark shadow over” Europe, as a human tragedy and affecting the economy. Economic activity is expected to continue to growth this year, “albeit at a slower pace than was expected “. The war has “amplified the impact on consumer energy prices”.

The surge in energy prices is “reducing demand and raising production costs” while the war is “weighing heavily on business and consumer confidence and has created new bottlenecks.” These developments point to slower growth in the period ahead.

Prices increased will “most likely remain high over the coming months”. Medium term inflation expectations indicates inflation ares around the 2% target. But, ” inflation expectations have been rising in recent months though and initial signs of above-target revisions in those measures warrant close monitoring.”

He reiterated that the APP will be concluded in Q3 and changes to interest rates will follow “some time after” the end of the net purchases, and will be “gradual”.

BoJ stands pat, maintains dovish bias

BoJ left monetary policy unchanged as widely expected, by 8-1 vote, with dove Goushi Kataoka dissented again. Under the yield curve control framework, short-term policy interest rate is held at -0.10%. 10-year JGB yield target is kept at around 0%, without upper limit on JGB purchases. BoJ also clarified that it will offer to purchase 10-year JGBs at 0.25$ every business day through fixed-rate purchase operations.

The central bank also reiterated that it will “expanding the monetary base until the year-on-year rate of increase in the observed consumer price index (CPI, all items less fresh food) exceeds 2 percent and stays above the target in a stable manner.”

It also pledged that it “will not hesitate to take additional easing measures if necessary; it also expects short- and long-term policy interest rates to remain at their present or lower levels.”

In the new economic projections, GDP is forecast to grow:

- 2.9% in fiscal 2022 (revised down from 3.8%)

- 1.9% in fiscal 2023 (revised up from 1.1%)

- 1.1% in fiscal 2024 (new).

CPI (all items less fresh food) is expected to be at:

- 1.9% in fiscal 2022 (revised up from 1.1%).

- 1.1% in fiscal 2023 (unchanged).

- 1.1% in fiscal 2024 (new).

Also released from Japan, industrial production rose 0.3% mom in March, below expectation of 0.5% mom. Retail sales rose 0.9% yoy in march, below expectation of 0.4% yoy.

New Zealand ANZ business confidence ticked down to -42 in Apr

New Zealand ANZ business confidence dropped slightly from -41.9 to -42.0 in April. Own activity outlook rose from 3.3 to 8.0. Export intentions rose from 7.9 to 9.5. Investment intentions dropped from 5.2 to 3.1. Employment intentions dropped from 12.3 to 9.4. Cost expectations dropped from 95.9 to 95.5. Inflation expectations rose further from 5.51 to 5.92.

ANZ said: “With plenty of wage and other cost inflation in the pipeline, it’ll be some time before the RBNZ can conclude that they’re getting ahead of the inflation game. We continue to expect another 50bp hike in May, and steady 25bp increases thereafter taking the OCR to a peak of 3.5%.”

NZ goods exports rose 17% yoy in Mar, imports rose 25% yoy

New Zealand goods exports rose 17% yoy to NZD 6.7B in March. Goods imports rose 25% yoy to NZD 7.1B. Trade balance was a deficit of NZD -392m, versus expectation of NZD -648m.

As a result of the monthly deficit in March 2022, the annual goods trade deficit has further widened to reach NZD -9.1B for the March 2022 year.

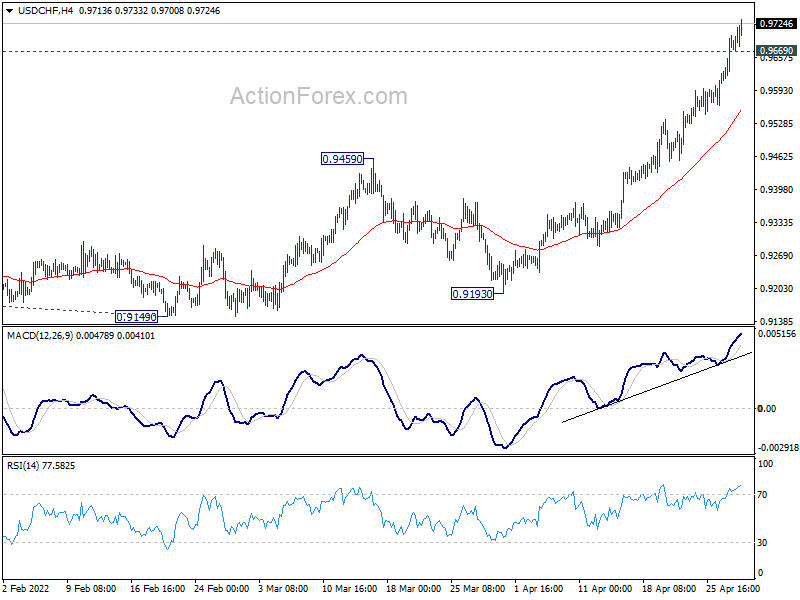

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9635; (P) 0.9669; (R1) 0.9722; More….

USD/CHF’s rally continues today and intraday bias remains on the upside. Current up trend should target next medium term projection level at 0.9864. On the downside, below 0.9669 minor support will turn intraday bias neutral and bring consolidations. But downside of retreat should be contained above 0.9459 resistance turned support to bring another rally.

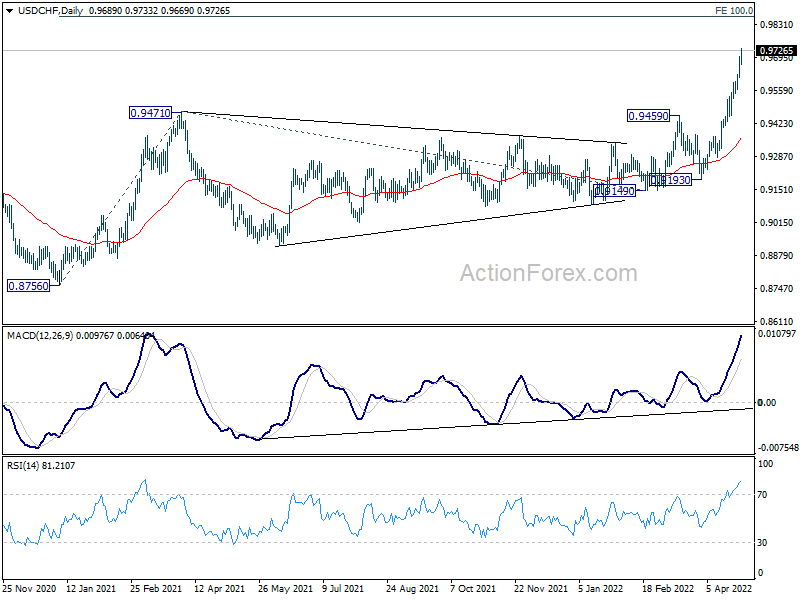

In the bigger picture, down trend from 1.0342 (2016 high) should have completed with three waves down to 0.8756 (2021 low) already. Rise from 0.8756 is likely a medium term up trend of its own. Next target is 100% projection of 0.8756 to 0.9471 from 0.9149 at 0.9864. This will now remain the favored case as long as 0.9459 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Mar | -392M | -648M | -385M | -691M |

| 23:50 | JPY | Industrial Production M/M Mar P | 0.30% | 0.50% | 2.00% | |

| 23:50 | JPY | Retail Trade Y/Y Mar | 0.90% | 0.40% | -0.80% | -0.90% |

| 01:00 | NZD | ANZ Business Confidence Apr | -42 | -41.9 | ||

| 01:30 | AUD | Import Price Index Q/Q Q1 | 5.10% | 7.10% | 5.80% | |

| 03:00 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 05:00 | JPY | Housing Starts Y/Y Mar | 6.00% | -0.50% | 6.30% | |

| 08:00 | EUR | ECB Economic Bulletin | ||||

| 12:00 | EUR | Germany CPI M/M Apr P | 0.80% | 1.70% | 2.50% | |

| 12:00 | EUR | Germany CPI Y/Y Apr P | 7.40% | 7.30% | 7.30% | |

| 12:30 | USD | Initial Jobless Claims (Apr 22) | 180K | 178K | 184K | 185K |

| 12:30 | USD | GDP Annualized Q1 P | -1.40% | 1.00% | 6.90% | |

| 12:30 | USD | GDP Price Index Q1 P | 8.00% | 6.00% | 7.10% | |

| 14:30 | USD | Natural Gas Storage | 39B | 53B |

{kind=link}