The forex markets are treading water today. Sentiments were lifted by China’s rate cut. UK retail sales came in stronger than expected. ECB officials continued to talk up the prospect of a July hike. But none of these triggered any meaningful moves in the markets. For the week, Swiss Franc is still the best performer, followed by Sterling and Kiwi. Dollar is the worst performing, finally ending the winning streak. Canadian and Yen are the next weakest.

Technically, focuses will stay on whether EUR/USD could break through 1.0641 resistance to confirm successfully defending 2017 low. But Euro itself is not looking too well in crosses, in particular in EUR/CHF. At the same time, EUR/GBP and EUR/AUD could extend the decline that started from last week’s high, after completing current consolidations. Such development could drag down EUR/USD. Anyway, Euro would probably wait until next week to unveil the next move.

In Europe, at the time of writing, FTSE is up 1.59%. DAX is up 1.66%. CAC is up 1.16%. Germany 10-year yield is down -0.0071 at 0.945. Earlier in Asia, Nikkei rose 1.27%. Hong Kong HSI rose 2.96%. China Shanghai SSE rose 1.60%. Singapore Strait Times rose 1.56%. Japan 10-year JGB yield dropped -0.0025 to 0.240.

ECB Visco: We will move rates perhaps in July

ECB Governing Council member Ignazio Visco said in a BloombergTV interview, “we can move gradually, raising interest rates in the coming months.” June is too early as the central bank will be ending net asset purchase. But, “we will move after that — after that, means perhaps July.”

“Now I think that we can move out of this negative territory,” Visco said, referring to the deposit rate, which has been negative since 2014. “Gradual means in my view that we have to understand that we should move without creating uncertainty in the market.”

Separately, Governing Council member Madis Muller said the focus needs to be on fighting high inflation. Martins Kazaks said he hoped the first hike will “take place in July”.

Released from Germany, PPI came in at 2.8% mom, 33.5% yoy in April, above expectation of 1.4% mom, 31.4% yoy.

BoE Pill: Further work needs to be done to counter inflation

BoE Chief Economist Huw Pill said in a speech,the balance of risk around inflation is “tilted towards inflation proving stronger and more persistent than anticipated in that baseline.”. Underlying developments that point in this direction include reduced contestability of UK labour markets by EU immigrants and workers due to Brexit. Broader globalization process looks to have stalled and maybe in retreat. Impact of aging and longer-term health consequences of the pandemic may have led to a decline in UK labour force participation.

Pill added that in this context, “avoiding any drift towards the embedding of such ‘inflationary psychology’ into the price setting process is crucial”. Thus, the time has now come to withdraw monetary policy accommodation.

“It is the need for a continuation of this transition in monetary policy that led me to support the 25bp hike in Bank Rate at the May MPC meeting,” he said. “And, even after this hike, I still view that necessary transition as incomplete. Further work needs to be done.”

UK retail sales rose 1.4% mom in Apr, ex-fuel sales up 1.4% mom

UK retail sales rose 1.4% mom in April, well above expectation of -0.2% mom decline. That’s also more than enough to recover the -1.2% mom decline in March. Ex-fuel sales also rose 1.4% mom, versus expectation of -0.2% mom, reversing the -0.9% mom decline in March.

However, for the most recent 3 months on previous 3 months, headline sales dropped -0.3% while ex-fuel sales dropped -0.5%.

New Zealand export rose 17% yoy in Apr, imports rose 15% yoy

New Zealand goods exports rose 17% yoy to NZD 6.3B in April. Imports rose 15% yoy to NZD 5.7%B. Monthly trade surplus came in at NZD 584m, versus expectation of NZD -350m deficit.

Exports rose for all top destinations except China, which was down -1.8%. Exports to Australia was up 4.9%, US up 26%, EU up 26%, Japan up 58%.

Import from all top partners rose, including China (up 8.9%), EU (up 18%), Australia (up 44%), US (up 29%), Japan (up 0.5%).

Japan CPI core rose to 2.5% yoy in Apr, CPI core-core rose to 0.8% yoy

Japan headline CPI (all items) rose from 1.2% yoy to 2.5% yoy in April. CPI core (ex-fresh food) rose from 0.8% yoy to 2.1% yoy. CPI core-core (ex-fresh food, energy) rose from -0.7% yoy to 0.8% yoy.

The 2.1% CPI core reading was slightly above expectation of 2.0% yoy. It topped BoJ’s 2% target for the firs time since March 2015. Also, it should be noted that CPI core-core was positive for the first time since July 2020.

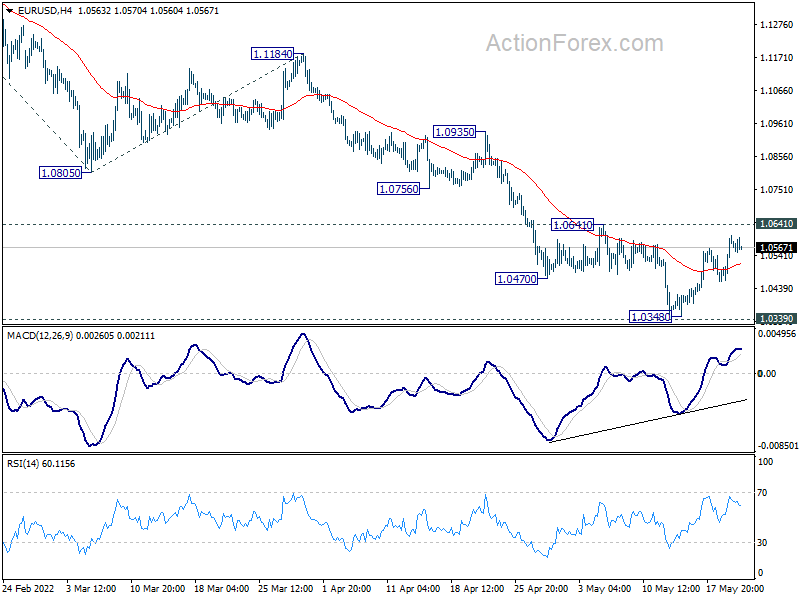

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0496; (P) 1.0551 (R1) 1.0642; More…

Intraday bias in EUR/USD remains neutral for the moment. Considering bullish convergence condition in 4 hour MACD, break of 1.0641 resistance will confirm short term bottoming at 1.0348, ahead of 1.0339 long term support. Intraday bias will be turned back to the upside for 55 day EMA (now at 1.0774). On the downside, however, decisive break of 1.0339 will carry larger bearish implication and target 161.8% projection of 1.1494 to 1.0805 from 1.1184 at 1.0069.

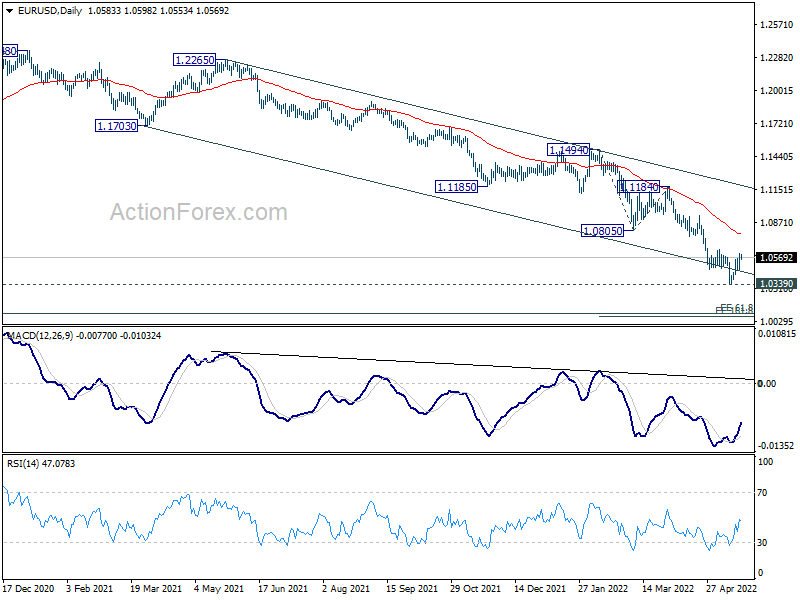

In the bigger picture, break of medium term channel support suggests downside acceleration. Current decline from 1.2348 (2021 high) is probably resuming long term down trend from 1.6039 (2008 high). Decisive break of 1.0339 will confirm this bearish case. Next target is 61.8% projection of 1.3993 to 1.0339 from 1.2348 at 1.0090. This will now remain the favored case as long as 1.0805 support turned resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Apr | 584M | -350M | -392M | |

| 23:01 | GBP | GfK Consumer Confidence May | -40 | -39 | -38 | |

| 23:30 | JPY | National CPI Core Y/Y Apr | 2.10% | 2.00% | 0.80% | |

| 06:00 | GBP | Retail Sales M/M Apr | 1.40% | -0.20% | -1.40% | -1.20% |

| 06:00 | GBP | Retail Sales Y/Y Apr | -4.90% | -7.20% | 0.90% | 1.30% |

| 06:00 | GBP | Retail Sales ex-Fuel M/M Apr | 1.40% | -0.20% | -1.10% | -0.90% |

| 06:00 | GBP | Retail Sales ex-Fuel Y/Y Apr | -6.10% | -8.40% | -0.60% | -0.20% |

| 06:00 | EUR | Germany PPI M/M Apr | 2.80% | 1.40% | 4.90% | |

| 06:00 | EUR | Germany PPI Y/Y Apr | 33.50% | 31.40% | 30.90% | |

| 14:00 | EUR | Eurozone Consumer Confidence May P | -21 | -22 |

{kind=link}