US stocks recovered overnight after Fed delivered the 75bps rate hike as market priced in, while Dollar and yields retreated. Asian markets are mixed with some weakness seen in Hong Kong HSI. For the week, the greenback remains the strongest one, except versus Yen which it’s paring gains against. Sterling is the worst performing as focus now turns to SNB and then BoE rate decision.

Technically, there is some downside prospect for Dollar for the near term, given then it was rejected against near term resistance levels against most peers. The levels include 1.0348 in EUR/USD, 0.6828 support in AUD/USD, 1.0063 resistance in USD/CHF and 1.3075 resistance in USD/CAD. Euro is the exception as it’s clearly weak against Sterling, Aussie and Canadian. In particular, eyes will be on whether side of the range of 0.8484/8720 would EUR/GBP breaks through.

In Asia, at the time of writing, Nikkei is up 0.82%. Hong Kong HSI is down -1.14%. China Shanghai SSE is down -0.28%. Singapore Strait Times is up 0.69%. Japan 10-year JGB yield is down -0.0118 at 0.244. Overnight, DOW rose 1.00%. S&P 500 rose 1.46%. NASDAQ rose 2.50%. 10-year yield dropped -0.088 to 3.395.

Fed hikes by 25bps, forecasts rate at 3.4% by end of 2022

Fed hikes by 75bps to 1.50-1.75%. Esther George dissented and voted for a 50bps hike only. Fed said that it’s “highly attentive to inflation risks” in the statement. Also, Fed now forecasts interest rate to be at 3.4% by the end of this year, sharply higher than prior estimate of 1.9%. Also, in the new dot plot, all members penciled in rate hikes to 3.125% and above by the end of 2022.

In the new median economic projections, federal funds rate is forecast to be at:

- 3.4% by the end of 2022 (up from 1.9%)

- 3.8% by the end of 2023 (up from 2.8%)

- 3.4% by the end of 2024 (up from 2.8%)

GDP growth is forecast to be at:

- 1.7% in 2022 (down from 2.8%)

- 1.7% in 2023 (down from 2.2%)

- 1.9% in 2024 (down from 2.0%)

PCE inflation is forecast to be at:

- 5.2% in 2022 (up from 4.3%)

- 2.6% in 2023 (down from 2.7%)

- 2.2% in 2024 (down from 2.2%)

Core PCE inflation is forecast to be at:

- 4.3% in 2022 (up from 4.1%)

- 2.7% in 2023 (up from 2.6%)

- 2.3% in 2024 (unchanged).

Unemployment rate is forecast to be at:

- 3.7% in 2022 (up from 3.5%)

- 3.9% in 2023 (up from 3.5%)

- 4.1% in 2024 (up from 3.6%)

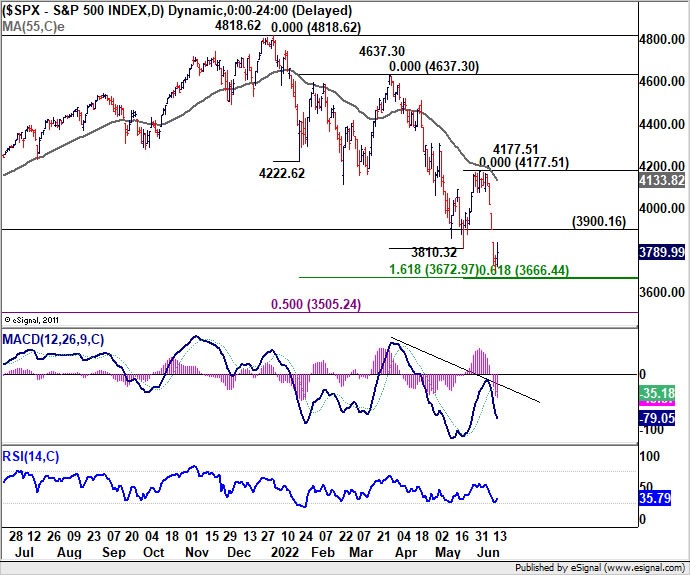

S&P 500 rose as traders covered on Fed news

US stocks closed higher overnight even though FOMC delivered an “uncommon” mega hike of 75bps. Fed Chair Jerome Powell also indicated at the post-meeting press conference that “either a 50 basis point or a 75 basis point increase seems most likely at our next meeting” while “ongoing rate increases will be appropriate.”

The recovery in stocks is more seen as a “sell-on-rumors-cover on news” move. Fed delivered what the markets have expected and the selloff was already done earlier in the week. Also, some would give a nod to Fed’s determination to combat inflation and create the conditions for a soft-landing, even though it’s a big challenge.

The condition for a stronger rebound in S&P 500 is there, give that it’s close to 3666.44/3672.97 cluster projection (61.8% projection of 4637.30 to 3810.32 from 4177.51 at 3666.44, 161.8% projection of 4818.62 to 4222.62 from 4637.30 at 3672.97). Yet, SPX will need to break through the top end of the latest gap at 3900.16 to indicate stabilization first. Otherwise, risk will remain heavily on the downside. Deeper fall into support zone between 3195.28 and 3505.24 (61.8% and 50% retracement of 2191.86 to 4818.62) is too early to be ruled out at this point.

Australia employment rose 60.6k in May, strong growth in hours worked

Australia employment rose 60.6k in May, better than expectation of 25.0k. Full-time jobs rose 69.4k while part-time jobs dropped -8.7k. Unemployment rate was unchanged at 3.9%, above expectation of 3.8%. Participation rate rose 0.3% to 66.7%. Monthly hours worked rose 0.9% mom or 17m.

Bjorn Jarvis, head of labour statistics at the ABS, said: “The increase in May 2022 was the seventh consecutive increase in employment, following the easing of lockdown restrictions in late 2021. Average employment growth over the past three months (30,000) continues to be stronger than the pre-pandemic trend of around 20,000 people per month.

“In addition to the continuing trend of increasing employment, we have continued to see relatively stronger growth in hours worked. This is something we also saw this time last year, before the Delta outbreak.”

New Zealand GDP fell -0.2% qoq in Q1, primary industries drove contraction

New Zealand GDP contracted -0.2% qoq in Q1, much worse than expectation of 0.6% qoq.

StatsNZ said: “Primary industries drove the decrease in GDP, down 1.2 percent in the quarter. Goods producing industries also experienced a slight decline, down 0.1 percent.

“The service industry group, which makes up approximately two thirds of the economy, remained flat. This result reflects falls in some industries being offset by rises in others.”

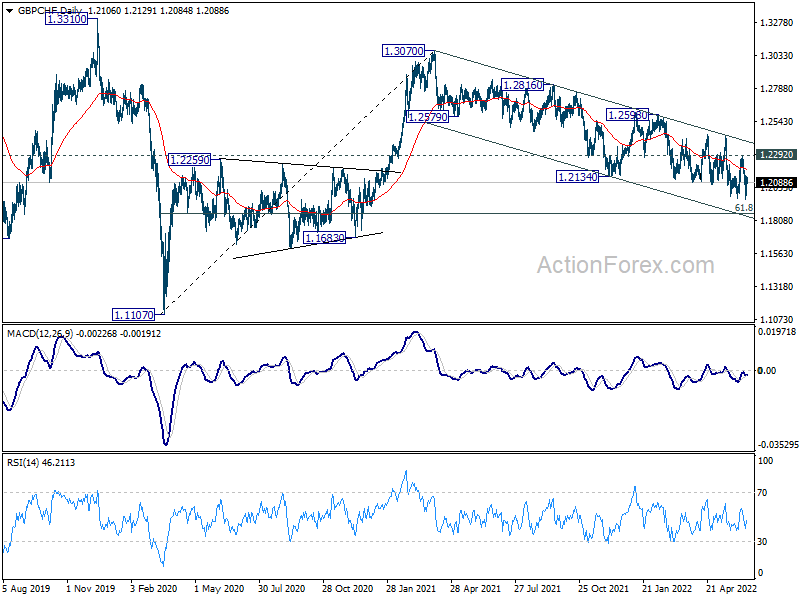

GBP/CHF staying bearish as SNB and BoE loom

SNB and BoE rate decisions are the next focuses for today. SNB is expected to policy unchanged today but start turning up a hawkish tone, setting the stage for the first rate hike in 15 years at the September meeting. Inflation reaching 2.9%, a 14-year high, in May isn’t much of a problem comparing to other parts of the world. Yet, ECB’s tightening stance is giving SNB much room to adjust policy now.

The situation for BoE is more complicated. A 25bps hike to 1.25% is the base case. There are arguments for a larger hike with inflation at 7.8% yoy. Yet, there are also arguments for a pause given that UK economy has already started a recession in Q2. The eventual decision and the voting could drive much volatility in the Pound.

Here are some previews for BoE and SNB:

- Bank of England Preview

- BoE Meeting Preview – 50bps or 25bps hike that is the question

- Bank of England: Steady as She Goes?

- SNB Meeting: Higher Rates or Patience?

GBP/CHF is staying in the down trend from 1.3070 for now and outlook remains bearish as long as 1.2292 resistance holds. But the structure of the decline suggests that it’s more of a corrective move. Downside potential could be limited with strong support at around 61.8% retracement of 1.1107 to 1.3070 at 1.1857 to complete the down trend.

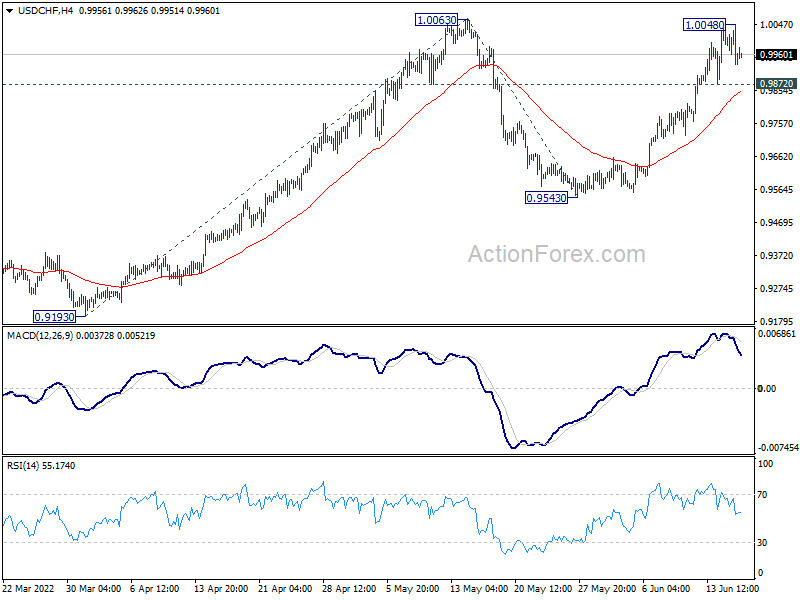

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9899; (P) 0.9974; (R1) 1.0017; More…

Intraday bias in USD/CHF is turned neutral again as it lost momentum ahead of 1.0063 resistance. On the upside, firm break of 1.0063 will resume larger up trend. Next target is 100% projection of 0.9193 to 1.0063 from 0.9543 at 1.0413. On the downside, below 0.9872 minor support will turn intraday bias to the downside, to extend the corrective pattern from 1.0063 with another falling leg.

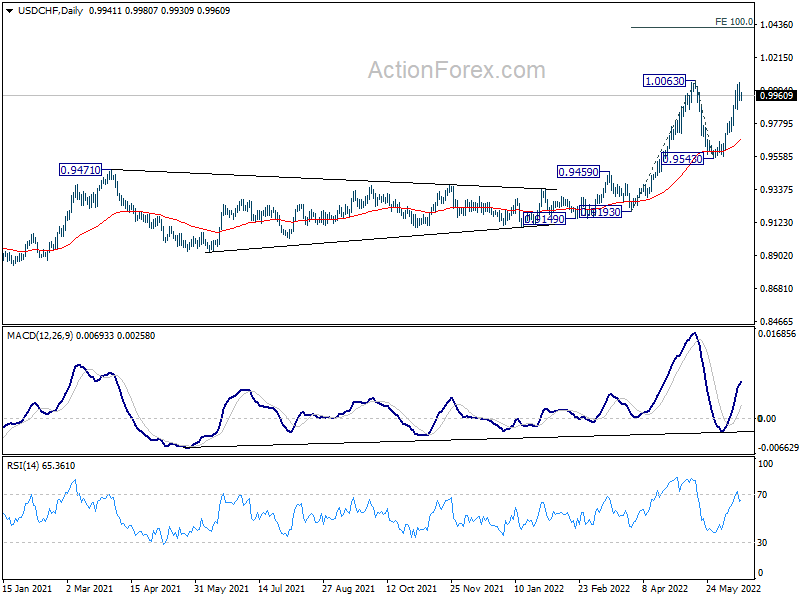

In the bigger picture, down trend from 1.0342 (2016 high) should have completed with three waves down to 0.8756 (2021 low) already. Rise from 0.8756 is likely a medium term up trend of its own. Next target is 1.0237/0342 resistance zone. This will remain the favored case as long as 0.9471 resistance turned support holds. However, sustained break of 0.9471 will extend long term range trading with another falling leg.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | GDP Q/Q Q1 | -0.20% | 0.60% | 3.00% | |

| 23:50 | JPY | Trade Balance (JPY) May | -1.93T | -1.70T | -1.62T | -1.58T |

| 01:00 | AUD | Consumer Inflation Expectations Jun | 6.70% | 5.00% | ||

| 01:30 | AUD | Employment Change May | 60.6K | 25.0K | 4.0K | 4.4K |

| 01:30 | AUD | Unemployment Rate May | 3.90% | 3.80% | 3.90% | |

| 07:30 | CHF | SNB Interest Rate Decision | -0.75% | -0.75% | ||

| 11:00 | GBP | BoE Interest Rate Decision | 1.25% | 1.00% | ||

| 11:00 | GBP | MPC Official Bank Rate Votes | 9–0–0 | 9–0–0 | ||

| 12:30 | CAD | Wholesale Sales M/M Apr | 0.50% | 0.30% | ||

| 12:30 | USD | Initial Jobless Claims (Jun 10) | 230K | 229K | ||

| 12:30 | USD | Housing Starts May | 1.71M | 1.72M | ||

| 12:30 | USD | Building Permits May | 1.79M | 1.82M | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Jun | 5.5 | 2.6 | ||

| 14:30 | USD | Natural Gas Storage | 92B | 97B |

{kind=link}