Sterling recovers today, in particular against Euro and Swiss Franc, after Boris Johnson resigns as UK Prime Minister. But Aussie is so far still the strongest for the day. Euro remains generally weak but Dollar and Yen are also paring some recent gains. For the week, Aussie is the best performer for now, followed by Dollar and then Yen. Euro is now the runaway loser, followed by Swiss Franc and then Canadian. But the overall picture could still be changed by tomorrow’s non-farm payrolls.

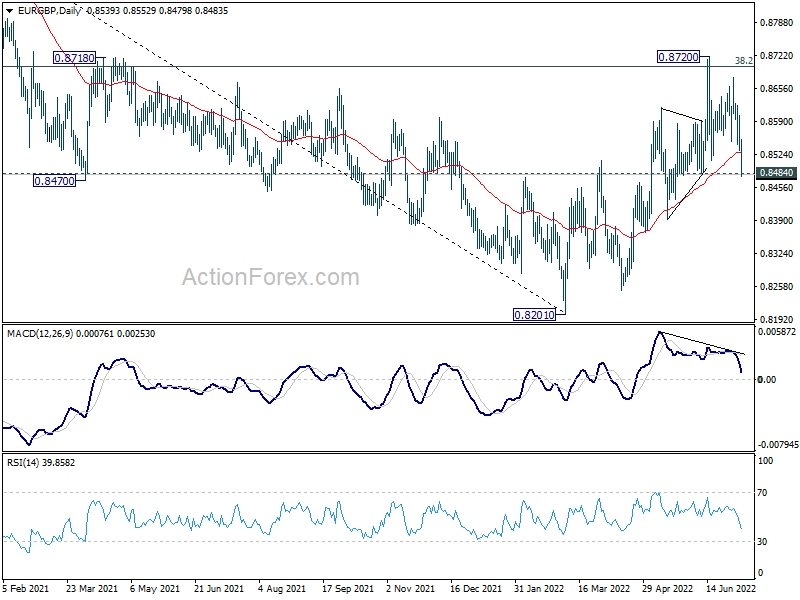

Technically, immediate focus is now on 0.8484 support in EUR/GBP. Sustained break there will argue that rebound from 0.8201 has completed at 0.8720, after rejection by 38.2% retracement of 0.9499 to 0.8201 at 0.8697. The would firstly retain medium term bearishness in the cross Secondly, deeper fall could be seen back to retest 0.8201 low.

In Europe, at the time of writing, FTSE is up 1.27%. DAX is up 1.84%. CAC is up 1.67%. Germany 10-year yield is up 0.071 at 1.232. Earlier in Asia, Nikkei rose 1.47%. Hong Kong HSI rose 0.26%. China Shanghai SSE rose 0.27%. Singapore Strait Times rose 0.83%. Japan 10-year JGB yield rose 0.0063 to 0.256.

US initial jobless claims rose to 235k

US initial jobless claims rose 4k to 235k in the week ending July 2, slightly above expectation of 230k. Four-week moving average of initial claims rose 750 to 232.5k.

Continuing claims rose 51k to 1375k in the week ending June 25. Four-week moving average of continuing claims rose 16.5k to 1335k.

ECB accounts: A number of members want door open for a larger hike in Jul

As noted in accounts of ECB’s June 8-9 monetary policy meeting, “most members” supported to signal the 25bps rate hike at the July meeting. Starting the rate-hiking cycle with a step of this magnitude was seen as a “proportionate first step”. But “a number of members expressed an initial preference for keeping the door open for a larger hike at the July meeting”

“It was broadly agreed that the Governing Council should at this point be more specific about its expectations for the September meeting and, in particular, open the door to an increase in the key ECB interest rates by more than 25 basis points,” the accounts added.

“Looking beyond September, members widely agreed that, on the basis of the current assessment, a gradual but sustained path of further interest rate increases would be appropriate, with the pace of adjustment depending on incoming data and developments in the medium-term inflation outlook.”

BoE Mann: It’s important to front-load policy

BoE MPC member Catherine Mann said, “what the research shows is when there is uncertainty about persistence versus transitory nature of inflation dynamics, it’s important to front-load policy.”

Mann also noted the recent depreciation in Sterling is feeding into the high inflation rate. Yet, it’s “not the point” to target exchanged rate. “The point is to have heightened awareness of the role of the currency, particularly in today’s climate of very high inflation rates,” she added.

Australia AiG services dropped to 48.8, two-speed pattern to gather pace

Australia AiG Performance of Services Index dropped -0.4 to 48.8 in June. Looking at some details, sales plummeted by -8.8 to 41.9. Employment surged 7.9 to 55.3. New orders ticked down by -0.8 to 58.9. Input prices rose 0.3 to 69.0. Selling prices rose 5.3 to 67.2. Averages jumped 10.3 to 67.7.

Innes Willox, Chief Executive Ai Group, said: “With interest rates rising for the first time in a decade, we have seen a ‘two-speed’ services sector emerge in June. Industries which are sensitive to sentiment changes – such as business & property, and personal & recreational services – declined into contraction. Less interest-rate-exposed services remained in a growth phase. With the RBA increasing rates by 50 basis points again this week, we would expect this two-speed pattern to gather pace.”

Also from Australia, goods and services exports rose 9.5% mom to AUD 58.4B in May. Goods and services imports rose 5.8% mom to AUD 42.4B. Trade surplus widened from AUD 13.2B to AUD 16.0B.

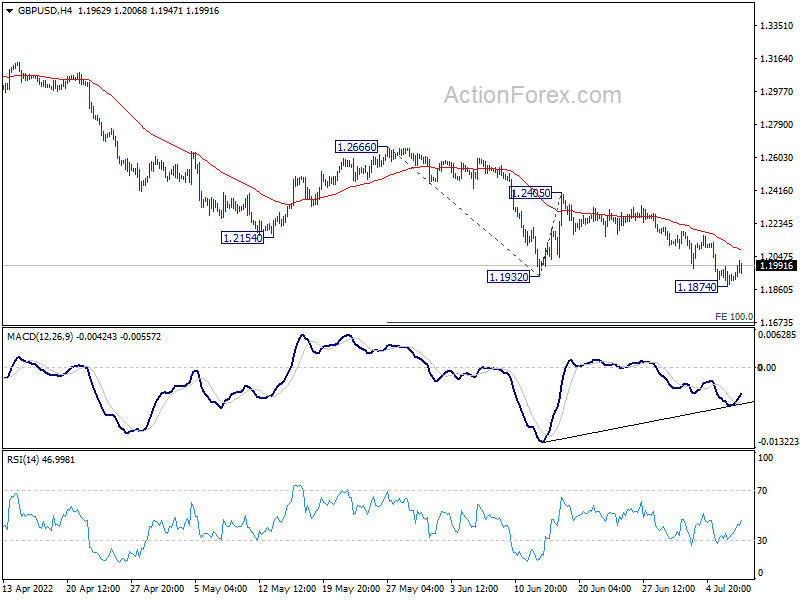

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1868; (P) 1.1929; (R1) 1.1982; More…

Intraday bias in GBP/USD is turned neutral with current recovery. Some consolidations could be seen but outlook stays bearish as long as 1.2405 resistance holds. On the downside, break of 1.1874 will resume larger down trend to t 100% projection of 1.2666 to 1.1932 from 1.2405 at 1.1671. Break there will target 1.1409 long term support.

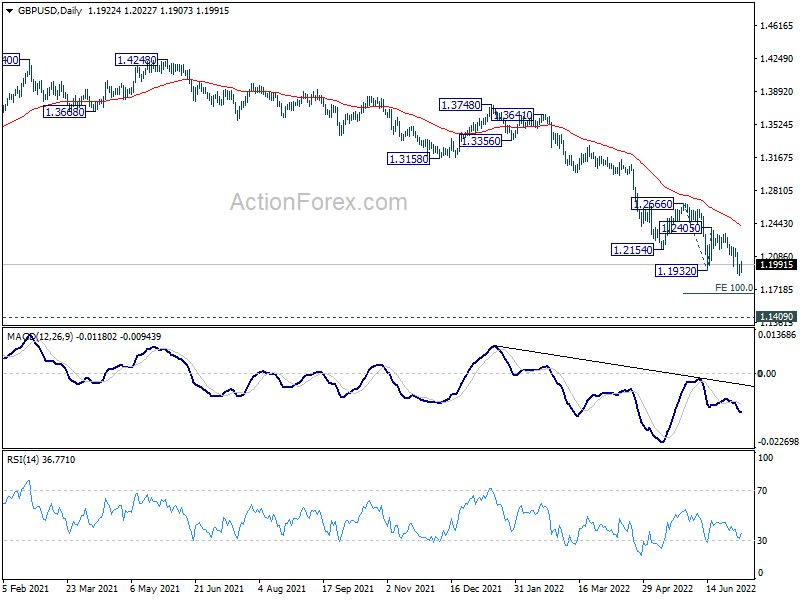

In the bigger picture, fall from 1.4248 (2018 high) could be a leg inside the pattern from 1.1409 (2020 low), or resuming the longer term down trend. Deeper decline is expected as long as 1.2666 resistance holds. Next target is 1.1409 low. However, firm break of 1.2666 will bring stronger rise back to 55 week EMA (now at 1.3103).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Services Index Jun | 48.8 | 49.2 | ||

| 01:30 | AUD | Trade Balance (AUD) May | 15.97B | 10.90B | 10.50B | 13.25B |

| 05:00 | JPY | Leading Economic Index May P | 101.40% | 101.60% | 102.90% | |

| 05:45 | CHF | Unemployment Rate Jun | 2.20% | 2.20% | 2.20% | |

| 06:00 | EUR | Germany Industrial Production M/M May | 0.20% | 0.40% | 0.70% | 1.30% |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Jun | 850B | 925B | ||

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 12:30 | USD | Initial Jobless Claims (Jul 1) | 235K | 230K | 231K | |

| 12:30 | USD | Goods and Services Trade Balance (USD) May | -85.5B | -85.0B | -87.1B | -86.7B |

| 12:30 | CAD | International Merchandise Trade (CAD) May | 5.3B | 2.5B | 1.5B | 2.2B |

| 14:00 | CAD | Ivey PMI Jun | 62.2 | 74 | 72 | |

| 14:30 | USD | Natural Gas Storage | 75B | 82B |

{kind=link}