Dollar is trading with a soft tone today, as focus turns to FOMC rate decision. Another 75bps hike is widely expected and Chair Jerome Powell is not expected to deliver any dramatic comments. Traders would likely come back after the event risk is cleared. In the currency markets, Euro is staying under much pressure on gas crisis but Sterling and Swiss Franc are not bothering too much. Commodity currencies are losing some upside momentum, but remain the relatively stronger ones.

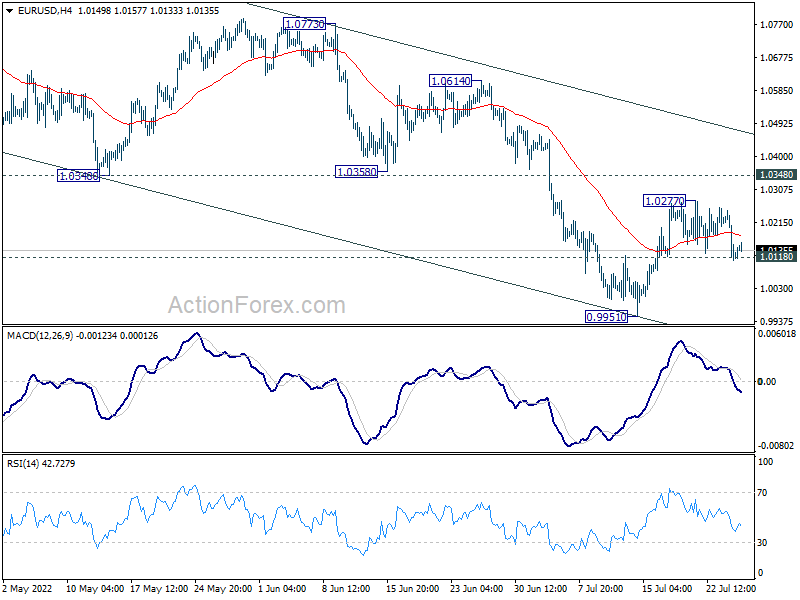

Technically, 1.0118 minor support in EUR/USD is the main focus today. It’s so far resiliently holding on to the level despite broad based Euro selloff. But firm break there will argue that rebound from 0.9951 has completed. More importantly, larger down trend would likely be ready to resume through 0.9951 low. This time, if happens, EUR/USD should trade below parity for a longer while before bottoming and reclaiming the psychological level.

In Asia, Nikkei rose 0.22%. Hong Kong HSI is down -1.04%. China Shanghai SSE is up 0.13%. Singapore Strait Times is up 0.02%. Japan 10-year JGB yield is down -0.0058 at 0.204. Overnight, DOW dropped -0.71%. S&P 500 dropped -1.15%. NASDAQ dropped -1.87%. 10-year yield dropped -0.033 to 2.787.

Australia CPI surged to record 6.1% yoy, but below expectations

Australia CPI rose 1.8% qoq in Q2, blow expectation of 1.9% qoq. For the 12-month period, CPI accelerated from 5.1% yoy to 6.1% yoy, below expectation of 6.3% yoy. RBA trimmed mean CPI came in at 1.5% qoq, 4.9% yoy, versus expectation of 1.5% qoq, 4.7% yoy.

The quarterly increase was the second highest since the introduction of the Goods and Services Tax (GST), following on from a 2.1% increase in Q1. The annual rise was the highest since the introduction of GST.

“Annual trimmed mean inflation was the highest since the series commenced in 2003 and annual goods inflation was the highest since 1987, as the impacts of supply disruptions, rising shipping costs and other global and domestic inflationary factors flowed through the economy,” said Head of Prices Statistics at the ABS, Michelle Marquardt.

Germany Gfk consumer sentiment hit another rock bottom at -30.6

Germany Gfk consumer sentiment for August dropped from -27.7 to -30.6, below expectation of -28.2. That’s another record low since the start of the series in 1991. In July, economic expectations dropped from -11.7 to -18.2. Income expectations dropped from -33.5 to -45.7. Propensity to buy dropped from -13.7 to -14.5.

“In addition to concerns about disrupted supply chains, the war in Ukraine and soaring energy and food prices, there are now worries about sufficient gas supplies for businesses and households next winter. This is currently causing consumer sentiment to hit rock bottom,” explains Rolf Bürkl, GfK consumer expert. “Especially as a tight supply of natural gas is likely to add to the pressure on energy prices and thus inflation.”

Fed to hike another 75bps again, some previews

Fed is widely expected to raise interest rates by 0.75% today, for the second time in a row, to bring the federal funds rate target rate to 2.25-2.50%. More tightening is expected afterwards, as most FOMC members believed that interest rates have enter into “restrictive” region to curb inflation, which is already at multi-decade high.

The questions are on the pace of tightening beyond the neutral range, its impact on economic activity, and risks of recession as a result. Fed Chair Jerome Powell will be grilled for these questions. But a concrete answer is unlikely for now. The next rate-setting meeting on September 21 is nearly two months away. Two sets of prices, jobs and activity data will be published during the time, and before the new economic projections. The situation is so uncertain for Powell to tell the markets anything meaningful.

Here are some previews on Fed:

- FOMC Preview – Assessing the Balance of Risk for Traders

- Fed to Likely Hike by 75 bps But May Still Weigh 100-bps Option

- FOMC Meeting Preview: Traders Looking for 75bps, Powell’s Presser Key

- All Eyes on Bond Yields ahead of FOMC

As for market reaction, a major focus is on 10-year yield. It’s so far still sitting comfortably above a key support zone of 2.709 and 38.2% retracement of 1.343 to 3.483 at 2.665. There is prospect of a rebound to flatten the yield curve of 2-year (3.053%) to 10-year (2.787%). But a firm break below 2.709 could signal a flush into bonds, which could send 10-year yield towards 50% at 2.413, and below. That will threaten the curve of 3-month (2.507) to 10-year yield, which will be a big warning.

Elsewhere

Swiss ZEW expectations and Eurozone M3 money supply will be released in European session. US will release goods trade balance, whole sales inventories, durable goods orders and pending home sales.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2835; (P) 1.2868; (R1) 1.2919; More…

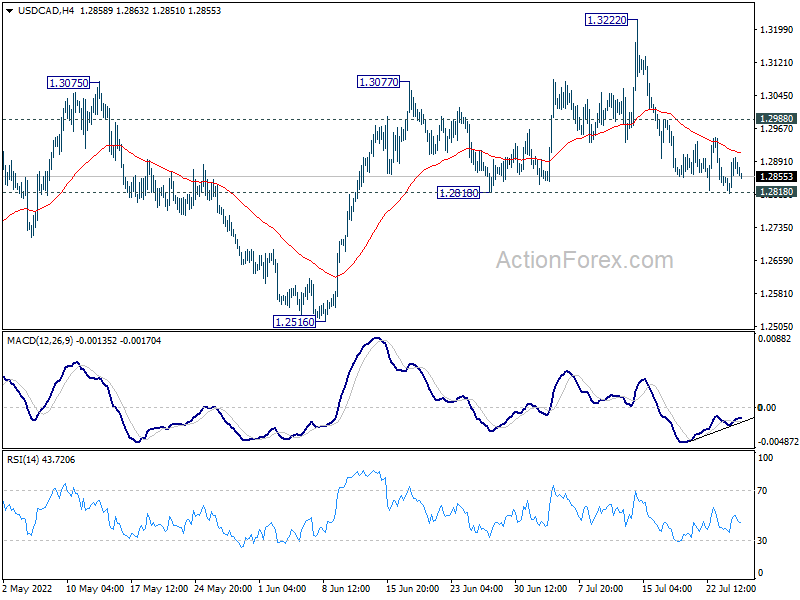

Intraday bias in USD/CAD remains neutral at this point. On the downside, firm break of 1.2818 support will bring deeper fall back to 1.2516 key support. This will also raise the chance of near term bearish reversal. On the upside, above 1.2988 minor resistance will reinforce near term bullishness, and turn bias back to the upside for retesting 1.3222 instead.

In the bigger picture, down trend from 1.4667 (2020 high) should have completed at 1.2005, after defending 1.2061 long term cluster support. Rise from there should target 61.8% retracement of 1.4667 to 1.2005 (2021 low) at 1.3650. This will remain the favored case now as long as 1.2516 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | CPI Q/Q Q2 | 1.80% | 1.90% | 2.10% | |

| 01:30 | AUD | CPI Y/Y Q2 | 6.10% | 6.30% | 5.10% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Q/Q Q2 | 1.50% | 1.50% | 1.40% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Y/Y Q2 | 4.90% | 4.70% | 3.70% | |

| 06:00 | EUR | Germany Gfk Consumer Confidence Aug | -30.6 | -28.2 | -27.4 | |

| 08:00 | CHF | CHF ZEW Expectations Jul | -72.7 | |||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Jun | 5.50% | 5.60% | ||

| 12:30 | USD | Goods Trade Balance (USD) Jun P | -103.2B | -104.3B | ||

| 12:30 | USD | Wholesale Inventories Jun P | 2.00% | 1.80% | ||

| 12:30 | USD | Durable Goods Orders Jun | -0.50% | 0.80% | ||

| 12:30 | USD | Durable Goods Orders ex Transportation Jun | 0.40% | 0.70% | ||

| 14:00 | USD | Pending Home Sales M/M Jun | 0.50% | 0.70% | ||

| 14:30 | USD | Crude Oil Inventories | -1.5M | -0.4M | ||

| 18:00 | USD | Fed Interest Rate Decision | 2.50% | 1.75% | ||

| 18:30 | USD | FOMC Press Conference |

{kind=link}