Dollar’s rally has finally made some progress overnight and the momentum continues in Asian session. Other currencies are mixed for now with no clear loser. For the week, Aussie and Kiwi are on the weaker side while Euro and Canadian are the stronger ones. But the picture could easily flip before close. A question is on whether stock markets would have another surge which gives Yen extra pressure.

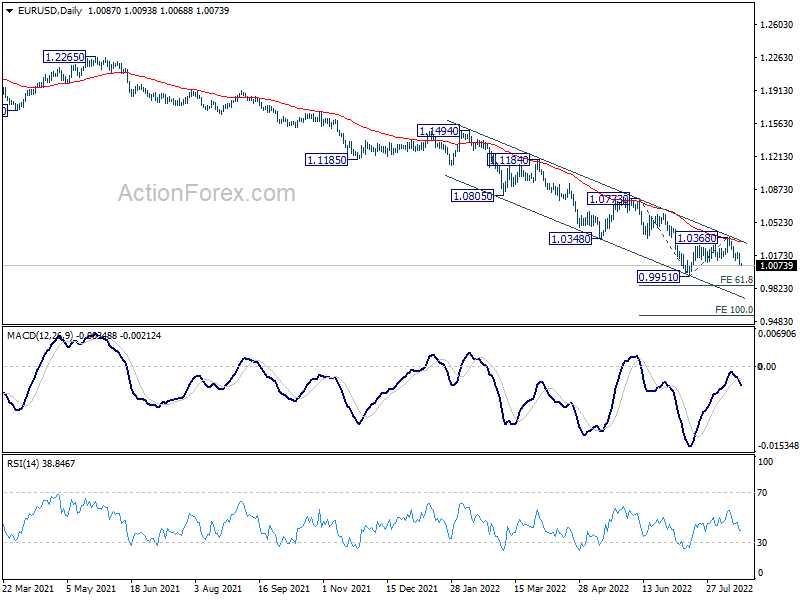

Technically, some attention remains on 0.6868 support in AUD/USD and 1.2984 resistance in USD/CAD. Break of these levels will confirm the underlying strength of Dollar against commodity currencies too. Such development could drag EUR/USD further lower through parity, towards 0.9951 low.

In Asia, Nikkei closed down -0.05%. Hong Kong HSI is up 0.25%. China Shanghai SSE is down -0.25%. Singapore Strait Times is down -0.74%. Japan 10-year JGB yield is down -0.0009 at 0.199. Overnight DOW rose 0.06%. S&P 500 rose 0.23% NASDAQ rose 0.21%. 10-year yield 10year yield dropped -0.013 to 2.880.

UK retail sales volume rose 0.3% mom in Jul

In volume term, UK retail sales rose 0.3% mom in July, better than expectation of -0.2% mom. Ex-auto sales rose 0.4% mom. Comparing to a year ago, retail sales dropped -3.4% yoy while ex-auto sales dropped -3.0% yoy.

In value term, retail sales rose 1.3% mom, 7.8% yoy. Ex-auto sales rose 1.4% mom, 5.7% yoy.

From Germany, PPI rose 5.3% mom, 37.2% yoy in July, above expectation of 0.5% mom, 31.5% yoy.

UK Gfk consumer confidence drooped to -44, another record low

UK Gfk consumer confidence dropped from -41 to -44 in August, hitting another record low. Personal financial situation over the next 12 months dropped from -26 to -31. General economic situation over the next 12 months dropped from -57 to -60, setting a new record low.

Joe Staton, Client Strategy Director, GfK says: “The Overall Index Score dropped three points in August to -44, the lowest since records began in 1974. All measures fell, reflecting acute concerns as the cost-of-living soars. A sense of exasperation about the UK’s economy is the biggest driver of these findings.”

Japan CPI core rose to 2.4% yoy, highest since 2014

Japan headline CPI rose from 2.4% yoy to 2.6% yoy in July, above expectation of 2.2% yoy. CPI core (all items ex-fresh food) rose from 2.2% yoy to 2.4% yoy, matched expectations. CPI core-core (all items ex-food, energy) rose from 1.0% yoy to 1.2% yoy, above expectations of 0.6% yoy.

Core inflation has now exceeded BoJ’s 2% target for four straight months, and hit the highest level since December 2014. The core-core reading was also the fastest since December 2015, while the headline reading was the strongest since 2008.

Both Prime Minister Fumio Kishida and BoJ Governor Haruhiko Kuroda have called for robust wage gains to ensure that inflation is sustainable. But the markets are expecting some pressure on the BoJ for acting on monetary policy if CPI hits 3%.

New Zealand goods exports rose 16% yoy in Jul, imports rose 26% yoy

New Zealand goods exports rose 16% yoy to NZD 6.7B in July. Goods imports rose 26% yoy to NZD 7.8B. Trade deficit came in at NZD -1.1B, comparing expectation of NZD 105m surplus.

China led the monthly rise in exports, up 13%. Exports to Australia was down -1.1%, USA up 5.8%, EU up 7.5%, Japan up 18%. Imports from China was up 19%, EU up 3.0%, Australia up 16%, USA up 34%, and Japan up 54%.

Fed George: Direction for rates pretty clear, but pace to be debated

Kansas City Fed President Esther George said yesterday that “the case for continuing to raise rates remains strong” and “the direction is pretty clear”.

But, “the question of how fast that has to happen is something my colleagues and I will continue to debate,” she added.

“We have done a lot, and I think we have to be very mindful that our policy decisions often operate on a lag. We have to watch carefully how that’s coming through,” she warned.

Separately, Minneapolis Fed President Neel Kashkari said the central bank needs to “urgently” bring down inflation. “The question right now is, can we bring inflation down without triggering a recession?” he said. “And my answer to that question is, I don’t know.”

Fed Bullard: We should continue to move expeditiously on rates

St. Louis Fed President James Bullard told WSJ, “we should continue to move expeditiously to a level of the policy rate that will put significant downward pressure on inflation” and “I don’t really see why you want to drag out interest rate increases into next year.”

Bullard also indicated that he backs another 75bps rate hike in September. He also reiterated he preference to have federal funds rate at 3.75-4.00% by the end of the year, from current 2.25-2.50%.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0047; (P) 1.0120; (R1) 1.0160; More…

EUR/USD’s fall from 1.0368 resumed by breaking through 1.0121. Intraday bias is back on the downside for retesting 0.9951 low first. Firm break there will resume larger down trend trend. Next near term targets are 61.8% projection of 1.0773 to 0.9951 from 1.0368 at 0.9860, and then 100% projection at 0.9546. On the upside, above 1.0203 minor resistance will turn intraday bias neutral. But risk will stay on the downside as long as 1.0368 resistance holds.

In the bigger picture, down trend from 1.6039 (2008 high) is still in progress. Next target is 100% projection of 1.3993 to 1.0339 from 1.2348 at 0.8694. In any case, outlook will stay bearish as long as 1.0773 resistance holds, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Jul | -1092M | 105M | -701M | -1102M |

| 23:01 | GBP | GfK Consumer Confidence Aug | -44 | -42 | -41 | |

| 23:30 | JPY | National CPI Core Y/Y Jul | 2.40% | 2.40% | 2.20% | |

| 06:00 | EUR | Germany PPI M/M Jul | 5.30% | 0.50% | 0.60% | |

| 06:00 | EUR | Germany PPI Y/Y Jul | 37.20% | 31.50% | 32.70% | |

| 06:00 | GBP | Retail Sales M/M Jul | 0.30% | -0.20% | -0.10% | -0.20% |

| 06:00 | GBP | Retail Sales Y/Y Jul | -3.40% | -3.30% | -5.80% | -6.10% |

| 06:00 | GBP | Retail Sales ex-Fuel M/M Jul | 0.40% | -0.20% | 0.40% | 0.20% |

| 06:00 | GBP | Retail Sales ex-Fuel Y/Y Jul | -3.00% | -2.80% | -5.90% | -6.20% |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Jul | 4.2B | 25.3B | 22.1B | 20.1B |

| 08:00 | EUR | Eurozone Current Account(EUR) Jun | -3.3B | -4.5B | ||

| 12:30 | CAD | Retail Sales M/M Jun | 0.40% | 2.20% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Jun | 0.90% | 1.90% |

{kind=link}