Dollar and Yen are staying as the weakest ones for the week as focus turns to US inflation data. European majors are the strongest ones so far, even though Euro’s rise is losing some momentum. Commodity currencies are mixed for now, despite improving risk sentiment.

Technically, EUR/JPY’s rally is slowing ahead of 61.8% projection of 124.37 to 144.26 from 133.38 at 145.67. For now, further rally is expected as long as 142.62 minor support holds. Firm break of 145.67 will pave the way to 149.76 long term resistance (2015 high). The next move could come as reaction to US CPI today.

In Asia, at the time of writing, Nikkei is up 0.21%. Hong Kong HSI is up 0.48%. China Shanghai SSE is up 0.33%. Singapore Strait Times is up 0.45%. Japan 10-year JGB yield is down -0.0029 at 0.248. Overnight, DOW rose 0.71%. S&P 500 rose 1.06%. NASDAQ rose 1.27%. 10-year yield rose 0.041 to 3.362.

Australia NAB business confidence rose to 10, conditions rose to 20

Australia NAB business confidence improved from 8 to 10 in August. Business conditions rose from 19 to 20. Trading conditions rose from 26 to 30. Profitability conditions dropped from 18 to 16. Employment conditions also dropped from 18 to 16.

“The recent strength in business conditions carried into August,” said NAB Group Chief Economist Alan Oster. “Official data for retail sales in July confirmed spending remained robust, as suggested by the previous survey, and today’s release shows little sign that August was much different. Conditions are strong across most industries other than construction, where profitability remains a challenge.”

“Confidence rose again in August, as did other forward indicators in the survey,” said Oster. “Confidence took a hit around June as interest rates first began to rise but it seems that firms’ initial concerns about the impact have eased and a more positive outlook is prevailing, at least for the time being.”

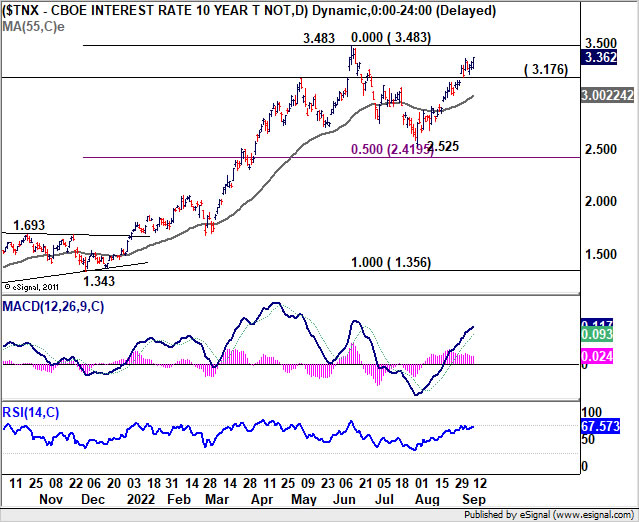

US 10-year yield extending rally ahead of CPI

US consumer inflation data will catch all attention today. Headline CPI is expected to decline -0.1% mom in August, with annual rate slowed from 8.5% yoy to 8.1% yoy. On the other hand, core CPI is expected rise 0.3% mom, with annual rate accelerated from 5.9% yoy to 6.0% yoy.

Today’s data is unlikely to alter Fed’s decision on on September 21, where markets are pricing in 88% chance of another 75bps hike. While inflation is starting to slow, the decline in energy prices could free up some money for consumer to spend, which supports the economy. Fed’s tightening will continue and there is a consensus that interest rate would reach 4% level by early next year.

Regarding market reaction to the data, some attention will be on 10-year yield, which rose 0.041 to 3.362 overnight. Current rise form 2.525 is expected to continue as long as 3.176 support holds, to retest 3.483 high. Such development should give Yen crosses a lift in general. But the next big move would depend more on whether 3.483 could be taken out decisively, at a later stage.

Elsewhere

Japan PPI rose 9.0% yoy in August, above expectation of 8.9% yoy. BSI large manufacturing index rose from -9.9 to 1.7 in Q3, above expectation of -8.1.

UK employment, Germany CPI final and ZEW economic sentiment, Swiss PPI will be released in European session. Later in the day, US CPI is the main focus.

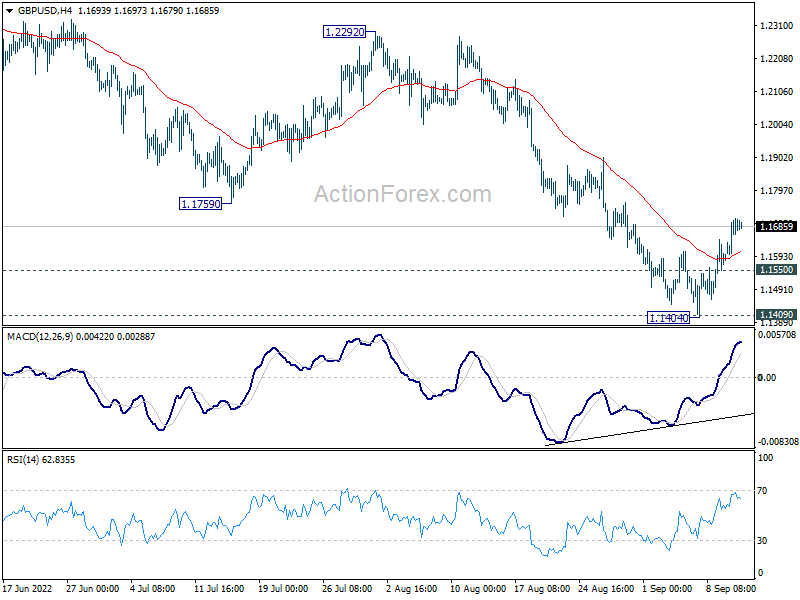

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.1618; (P) 1.1665; (R1) 1.1728; More…

GBP/USD’s rebound from 1.1404 short term bottom is in progress. Intraday bias stays on the upside for 55 day EMA (now at 1.1924). On the downside, below 1.1550 minor support will turn bias back to the downside. Decisive break of 1.1409 will resume larger down trend.

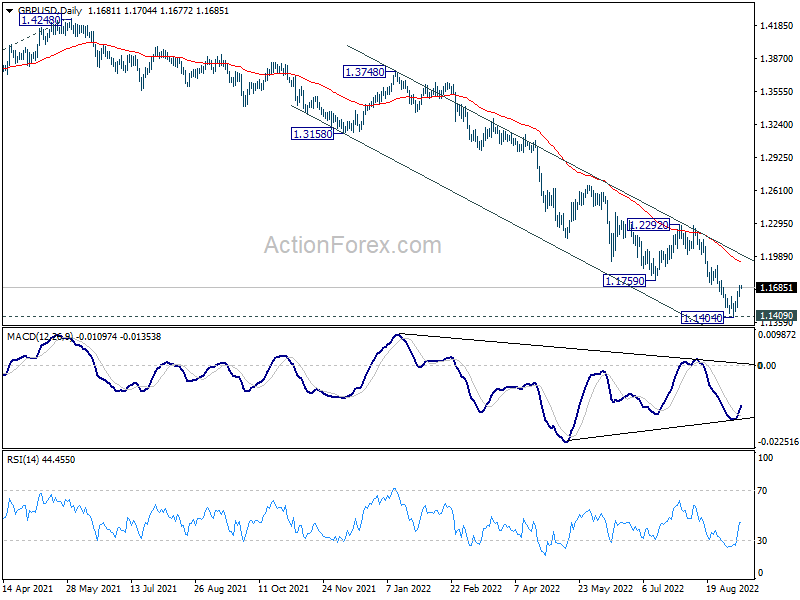

In the bigger picture, based on current momentum, fall from 1.4248 (2018 high) is probably resuming long term down trend from 2.1161 (2007 high). Sustained break of 1.1409 will target 61.8% projection of 1.7190 (2014 high) to 1.1409 (2020 low) from 1.4248 (2021 high) at 1.0675. This will remain the favored case for now as long as 1.2292 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Aug | 9.00% | 8.90% | 8.60% | 9.00% |

| 23:50 | JPY | BSI Large Manufacturing Index Q3 | 1.7 | -8.1 | -9.9 | |

| 01:30 | AUD | NAB Business Confidence Aug | 10 | 7 | 8 | |

| 01:30 | AUD | NAB Business Conditions Aug | 20 | 20 | 19 | |

| 06:00 | GBP | Claimant Count Change Aug | -9.2K | -10.5K | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) Jul | 3.80% | 3.80% | ||

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Jul | 5.20% | 5.10% | ||

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jul | 5.00% | 4.70% | ||

| 06:00 | EUR | Germany CPI M/M Aug F | 0.30% | 0.30% | ||

| 06:00 | EUR | Germany CPI Y/Y Aug F | 7.90% | 7.90% | ||

| 06:30 | CHF | Producer and Import Prices M/M Aug | 0.10% | -0.10% | ||

| 06:30 | CHF | Producer and Import Prices Y/Y Aug | 5.70% | 6.30% | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment Sep | -60 | -55.3 | ||

| 09:00 | EUR | Germany ZEW Current Situation Sep | -50.5 | -47.6 | ||

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Sep | -58.3 | -54.9 | ||

| 10:00 | USD | NFIB Business Optimism Index Aug | 90.6 | 89.9 | ||

| 12:30 | USD | CPI M/M Aug | -0.10% | 0.00% | ||

| 12:30 | USD | CPI Y/Y Aug | 8.10% | 8.50% | ||

| 12:30 | USD | CPI Core M/M Aug | 0.30% | 0.30% | ||

| 12:30 | USD | CPI Core Y/Y Aug | 6.00% | 5.90% |

{kind=link}