Dollar regains some growth today, and even rises to new 32-year high against Yen. Momentum is somewhat weak, however, as traders are guarding against intervention by Japan. Meanwhile, markets are mixed elsewhere. Sterling dips after UK Finance Minister Kwasi Kwarteng announced his resignation ahead of Prime Minister Liz Truss’s press conference later in the day. For now, the Pound is still the strongest for the week, followed by Kiwi and the Dollar. Yen is worst, followed by Aussie and the Swiss Franc. But there is scope for some changes in position in the final hours.

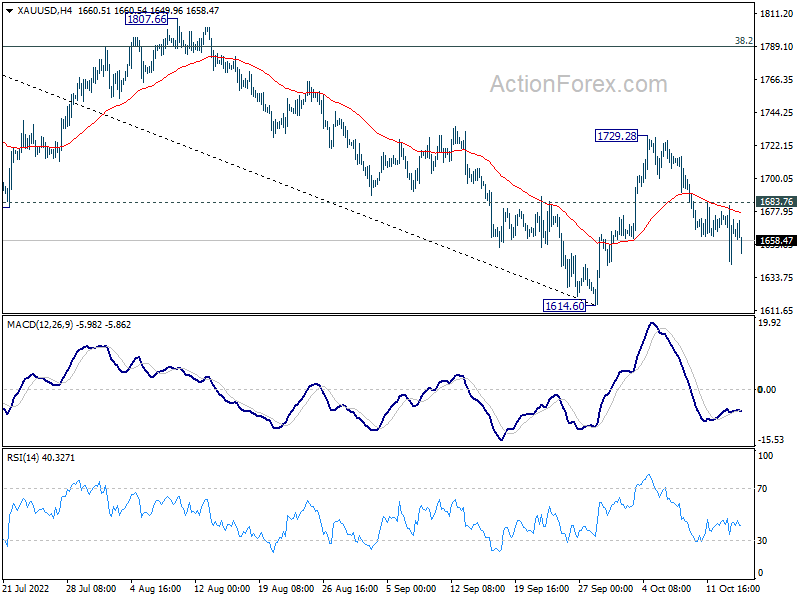

Technically, while Dollar retreated quite notably yesterday, the recovery in gold was so far very weak. Current development suggests that rebound from 1614.60 has completed at 1729.28 already. Further decline is now in favor as long as 1683.76 minor resistance holds, to retest 1614.60 low. Firm break there will resume larger decline.

In Europe, at the time of writing, FTSE is up 1.04%. DAX is up 1.16%. CAC is up 1.64%. Germany 10-year yield is down -0.108 at 2.173. Earlier in Asia, Nikkei rose 3.25%. Hong Kong HSI rose 1.21%. China Shanghai SSE rose 1.84%. Japan 10-year JGB yield rose 0.0028 to 0.254.

US retail sales growth flat in Sep, ex-auto sales up 0.1% mom

US retail sales growth was flat at 0.0% mom in September, at USD 684.0B. Ex-auto sales rose 0.1% mom, better than expectation of -0.1% mom. Ex-gasoline sales rose 0.1% mom. Ex-auto and gasoline sales rose 0.3% mom. Total sales for July through September period were up 9.2% from the same period a year ago.

Also released, import price index dropped -1.2% mom in September, below expectation of -1.1% mom.

From Canada, manufacturing sales dropped -2.0% mom in August, versus expectation of -1.1% mom. Wholesale sales rose 1.4% mom, above expectation of 0.1% mom.

ECB Lagarde: Valuations vulnerable to a range of possible negative surprises

ECB President Christine Lagarde said the financial markets may be overly optimistic about the economic outlook. “This makes valuations vulnerable to a range of possible negative surprises, whether from growth, inflation, monetary policy or corporate profitability,” she said.

Vice President Luis de Guindos said, “what we considered as our downside scenario in September, is coming closer to the baseline scenario… I think we are going to face a very difficult combination of low economic growth, including the possibility of a technical recession, and high inflation,”

Governing Council member Bostjan Vasle said, “We won’t stop at the neutral rate, we need to keep powering through… I’m of the opinion that we will have to go above the neutral level in order to calm inflation pressures, which are currently in the pipeline.

Eurozone exports rose 24.0% yoy in Aug, imports rose 53.6% yoy

Eurozone exports of goods rose 24.0% yoy to EUR 231.1B in August. Imports rose 53.6% yoy to EUR 282.1B. Trade deficit came in at EUR -50.9B. Intra-Eurozone trade rose 34.8% yoy to EUR 210.5B.

In seasonally adjusted term, exports rose 3.5% mom to EUR 245.5B. Imports rose 5.5% mom to EUR 292.8B. Trade deficit widened from EUR -40.5B to EUR -47.3B, much larger than expectation of EUR -40.0B. Intra-Eurozone trade rose from EUR 230.9B to EUR 239.2B.

NZ BNZ manufacturing dropped to 52.0, positive trend with ongoing volatility

New Zealand BusinessNZ Performance of Manufacturing Index dropped back from 54.8 to 52.0 in September, comparing to July’s 53.5 and June’s 50.2. Looking at some details, production dropped from 54.5 to 52.0. Employment dropped from 53.6 to 51.9. New orders tumbled sharply from 59.7 to 48.4. Finished stocks rose from 52.0 to 55.0. Deliveries edged down from 55.0 to 54.5.

BNZ Senior Economist, Doug Steel stated “the overall trend remains positive, but with ongoing volatility around it. On the positive side, the PMI’s 3-month moving average has continued to edge higher this month but, not so good, the 52.0 monthly reading is now back below the PMI’s longer-term norm”.

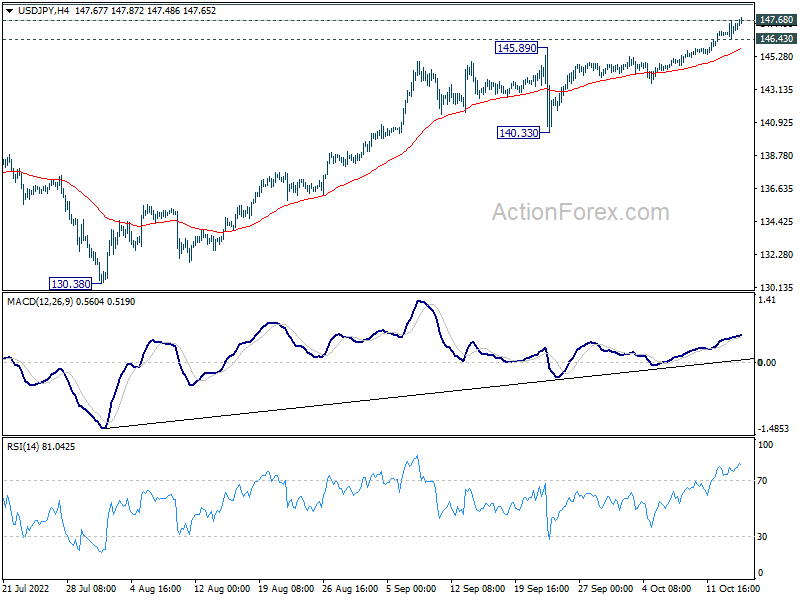

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.58; (P) 147.12; (R1) 147.78; More…

USD/JPY’s rally continues and breaks 147.68 long term resistance. Intraday bias stays on the upside for 149.25 projection level, and possibly to 150 psychological level. On the downside, break of 146.43 minor support will now suggest short term topping, and turn bias back to the downside for deeper pull back.

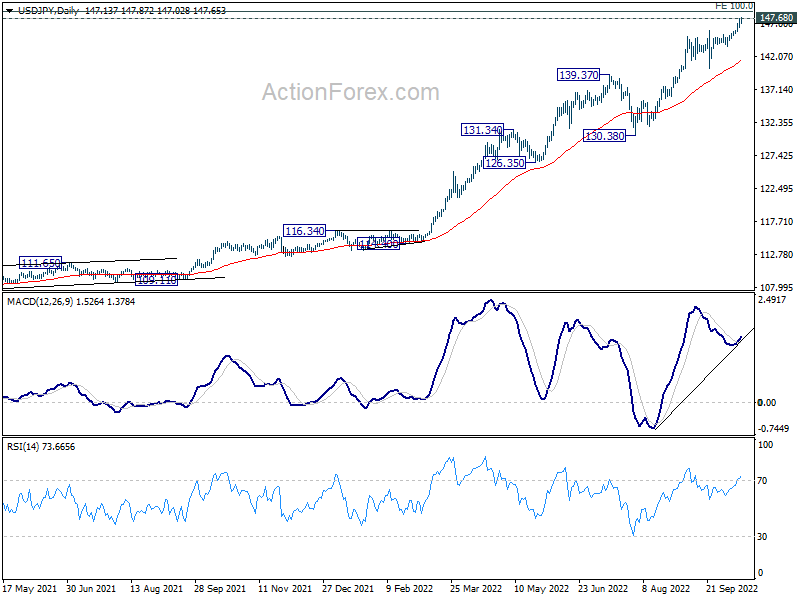

In the bigger picture, up trend from 101.18 is still in progress, as part of the whole up trend from 75.56 (2011 low). Further rise should be seen to 147.68 (1998 high), and possibly to 100% projection of 75.56 (2011 low) to 125.85 (2015 high) from 98.97 at 149.26, For now, break of 130.38 support is needed to be the first indication of medium term topping. Otherwise, outlook will stay bullish even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PMI Sep | 52 | 54.9 | 54.8 | |

| 23:50 | JPY | Money Supply M2+CD Y/Y Sep | 3.30% | 3.40% | 3.40% | |

| 01:30 | CNY | CPI Y/Y Sep | 2.80% | 2.80% | 2.50% | |

| 01:30 | CNY | PPI Y/Y Sep | 0.90% | 1.10% | 2.30% | |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Aug | -47.3B | -40.0B | -40.3B | |

| 12:30 | CAD | Manufacturing Sales M/M Aug | -2.00% | -1.10% | -0.90% | -0.60% |

| 12:30 | CAD | Wholesale Sales M/M Aug | 1.40% | 0.10% | -0.60% | |

| 12:30 | USD | Retail Sales M/M Sep | 0.00% | 0.20% | 0.30% | 0.40% |

| 12:30 | USD | Retail Sales ex Autos M/M Sep | 0.10% | -0.10% | -0.30% | -0.10% |

| 12:30 | USD | Import Price Index M/M Sep | -1.20% | -1.10% | -1.00% | -1.10% |

| 14:00 | USD | Michigan Consumer Sentiment Index Oct P | 58.8 | 58.6 | ||

| 14:00 | USD | Business Inventories Aug | 0.90% | 0.60% |

{kind=link}