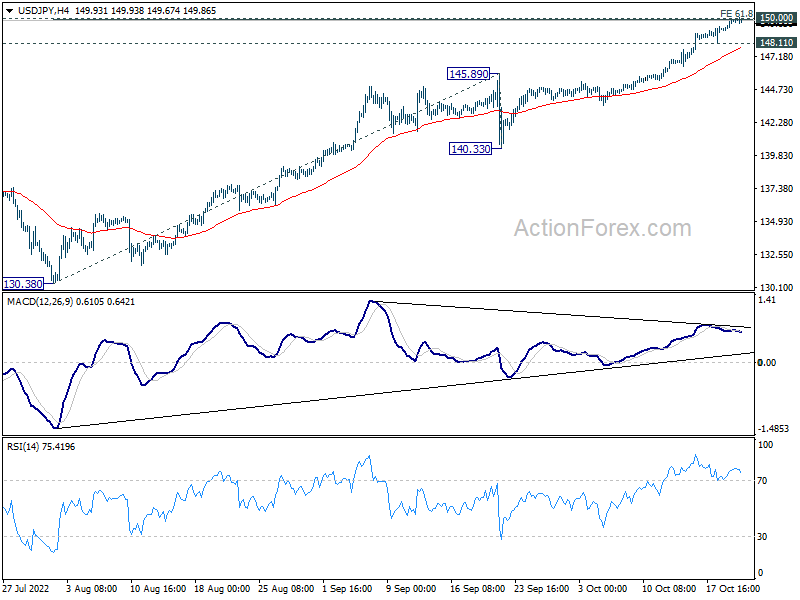

Dollar softens slightly today after failing to have a decisive rally against Yen. Nevertheless, the battle for 150 is still on. Sterling is lifted slightly by news of UK Prime Minister Liz Truss’s resignation, but there is no follow through buying. Commodity currencies are trading mildly higher as risk sentiment stabilized. Overall, there is no clear, committed direction entering into US session.

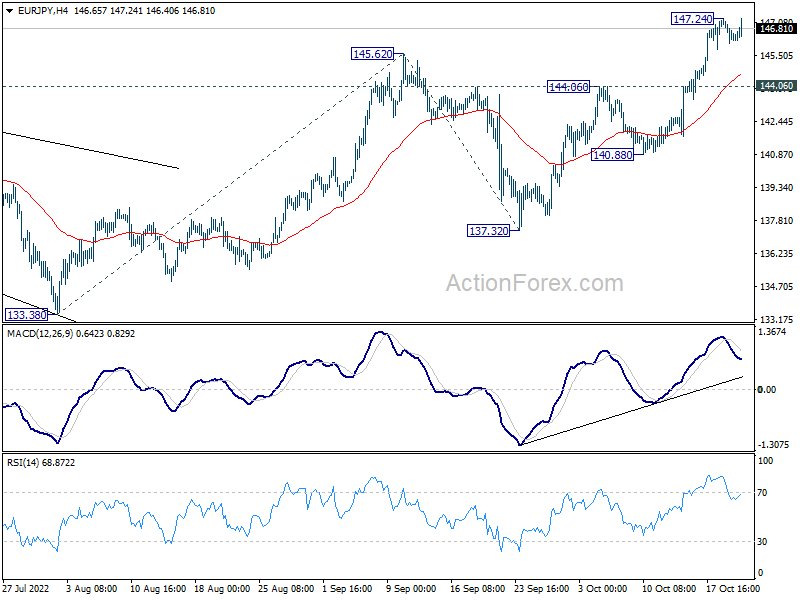

Technically, as USD/JPY is struggling around 150 for now, focus is back on 147.24 temporary top in EUR/JPY and 170.07 in GBP/JPY. Break of these levels will indicate completion of brief consolidation and recent up trends are ready to resume. That might give USD/JPY a hand on 150.

In Europe, at the time of writing, FTSE is down -0.01%. DAX is down -0.30%. CAC is up 0.32%. Germany 10-year yield is up 0.023 at 2.401. Earlier in Asia, Nikkei dropped -0.92%. Hong Kong HSI dropped -1.40%. China Shanghai SSE dropped -0.31%. Singapore Strait Times closed flat. Japan 10-year JGB yield dropped -0.0006 to 0.254.

US initial jobless claims dropped to 214k

US initial jobless claims dropped -12k to 214k in the week ending October 15, lower than expectation of 235k. Four-week moving average of initial claims rose 1k to 212k.

Continuing claims rose 21k to 1385k in the week ending October 8. Four-week moving average of continuing claims rose 2k to 1365k.

Philly Fed manufacturing rose slightly from -9.9 to -8.7 in October, below expectation of -5.

BoE Broadbent: Energy price guarantee’s inflationary effect outweighs limiting inflation

BoE Deputy Governor Ben Broadbent said in a speech that firstly, “for as long as it’s in place, the government’s Energy Price Guarantee has the effect of limiting headline inflation and, to that extent, any related strengthening of second-round (and more persistent) effects on domestic inflation.”

Secondly, “by the same token, however, it mitigates the severity of the hit to household incomes and thereby supports domestic demand,” he added. “As the Committee noted last month, this would – all else equal – add to inflation in the medium term.”

“Compared with the forecast we had in August, the MPC has judged that the second effect is likely to outweigh the first,” he said.

But Broadbent added, there is uncertainty about the “nature and duration” of the energy subsidies. “The MPC will take account of any fiscal news in the forthcoming Medium-Term Fiscal Plan, as well as any other news relevant for the medium-term inflation outlook, in its next set of forecasts,” he said.

Australia employment grew 0.9k in Sep, unemployment rate unchanged at 3.5%

Australia employment rose 0.9k in September, below expectation of 25.0k. Full-time employment increased by 13.3k while part0time employment contracted -12.4k.

Unemployment rate was unchanged at 3.5%, matched expectations. Participation rate was unchanged at 66.6%. Monthly hours worked dropped -1m hours to 1853 hours.

“It is important to remember that the 1,000 employed people is a net figure – the difference between two large numbers. While employment growth has slowed in recent months, there are still close to half a million people entering employment each month, and around the same number leaving employment each month,” Bjorn Jarvis, head of labour statistics at the ABS, said.

Japan exports rose 28.9% yoy in Sep, imports surged 45.2% yoy

Japan’s exports rose 28.9% yoy to JPY 8189B in September. Exports to China grew 17.1% yoy while shipments to the US increased 45.2% yoy. Imports rose 45.9% yoy to JPY 10913B. However, the surge in import was unlikely a reflection of domestic demand, but sharp depreciation in Yen’s exchanged rate. Trade deficit came in at JPY -2094B, down from August’s record high of JPY -2817B

In seasonally adjusted term, exports rose 3.2% mom to JPY 8672B. Imports dropped -0.6% mom to JPY 10682B. Trade deficit narrowed to JPY -2010B, slightly smaller than expectation of JPY -2.06T.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.38; (P) 149.64; (R1) 150.18; More…

Focus remains on USD/JPY’s reaction to 150 psychological level, as Japan might intervene. Break of 148.11 support should confirm short term topping and turn bias back to the downside for deeper pull back. However, sustained break of 150 will extend larger up trend, and pave the way to 100% projection of 130.38 to 140.33 from 145.89 at 155.84 next.

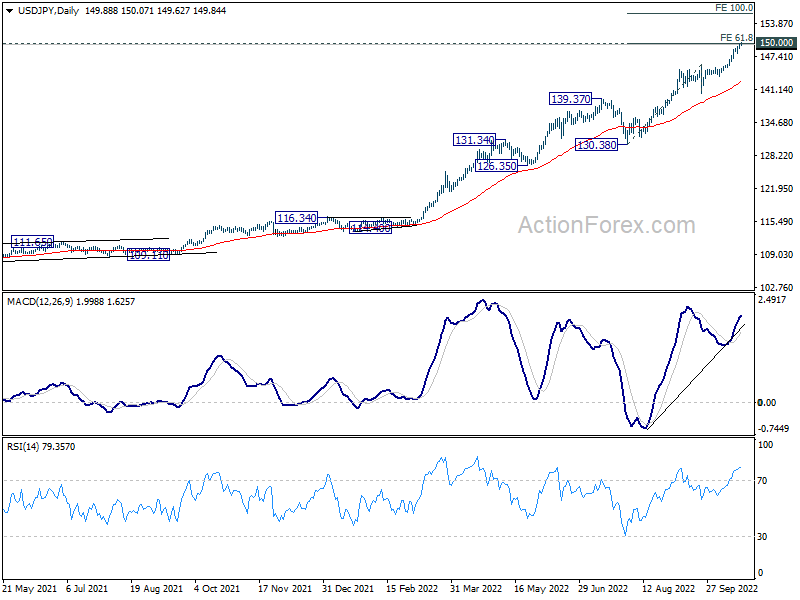

In the bigger picture, up trend from 101.18 is still in progress, as part of the whole up trend from 75.56 (2011 low). 147.68 (1998 high) was already met and there is not clearly sign of topping yet. In any case, break of 139.37 resistance turned support is needed to be the first sign of medium term topping. Otherwise, further rise is in favor to next target at 160.16 (1990 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Sep | -2.01T | -2.06T | -2.37T | -2.34T |

| 00:30 | AUD | NAB Business Confidence Q3 | 9 | 5 | ||

| 00:30 | AUD | Employment Change Sep | 0.9K | 25.0K | 33.5K | 36.3K |

| 00:30 | AUD | Unemployment Rate Sep | 3.50% | 3.50% | 3.50% | |

| 06:00 | CHF | Trade Balance (CHF) Sep | 4.00B | 4.23B | 3.42B | 3.32B |

| 06:00 | EUR | Germany PPI M/M Sep | 2.30% | 1.30% | 7.90% | |

| 06:00 | EUR | Germany PPI Y/Y Sep | 45.80% | 44.00% | 45.80% | |

| 08:00 | EUR | Eurozone Current Account (EUR) Aug | -26.3B | -20.3B | -19.9B | |

| 12:30 | USD | Initial Jobless Claims (Oct 14) | 214K | 235K | 228K | 226K |

| 12:30 | USD | Philadelphia Fed Manufacturing Oct | -8.7 | -5 | -9.9 | |

| 14:00 | USD | Existing Home Sales Sep | 4.69M | 4.80M | ||

| 14:30 | USD | Natural Gas Storage | -173.5B | 125B |

{kind=link}