Yen remains the biggest loser for the week even though Japan has stepped up with the rhetorics against “speculations”. Dollar is standing above 150 level against Yen for now, without clear sign of actual intervention. The pair is supported by 10-year yield which broke above 5.2 handle. Nevertheless, thanks to stabilization in overall market sentiment, the greenback is also among the weakest together with Swiss Franc. Commodity currencies are the winner for now. Sterling is a touch weaker against Euro, having little reaction to the continuous political chaos in the UK, while both are mixed.

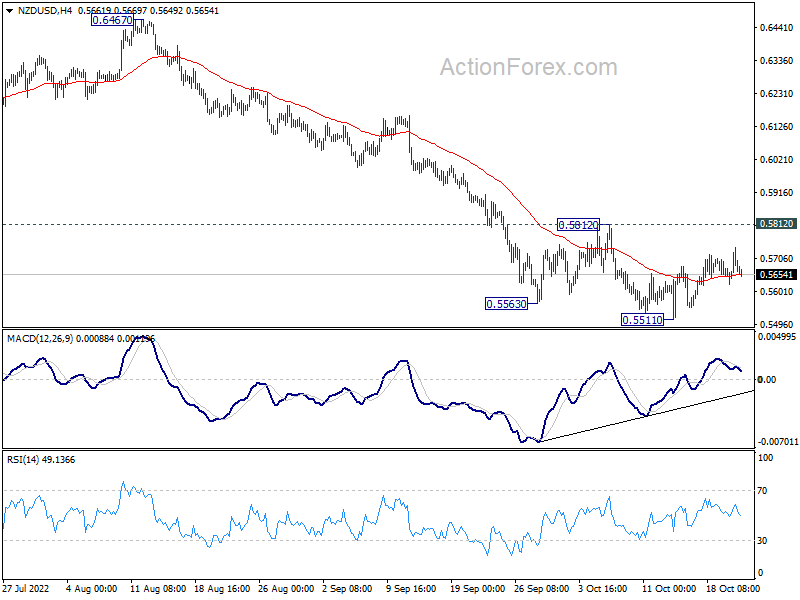

Technically, it should be emphasized that the recoveries in Aussie, Kiwi and Loonie are so far weak, and don’t warrant trend reversal. The key near term levels included 0.6362 resistance in AUD/USD, 0.5812 resistance in NZD/USD, and 1.3501 support in USD/CAD. As long as these level holds, selloffs in the three will more likely resume than not.

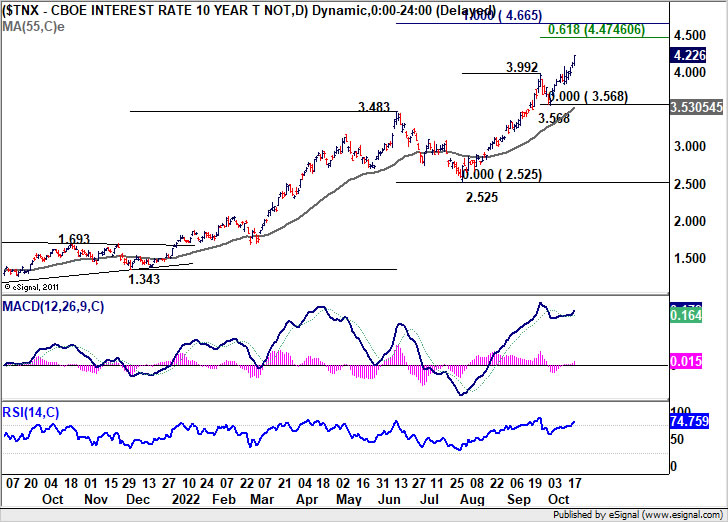

In Asia, at the time of writing, Nikkei is down -0.30%. Hong Kong HSI is down -0.17%. China Shanghai SSE is up 0.50%. Singapore Strait Times is down -1.07%. Japan 10-year JGB yield is up 0.0004 at 0.254. Overnight, DOW dropped -0.30%. S&P 500 dropped -0.80%. NASDAQ dropped -0.61%. 10-year yield rose 0.099 to 4.226.

Fed Harker: Interest will be well above 4% by year-end

Philadelphia Fed President Patrick Harker said yesterday, “We are going to keep raising rates for a while. Given our frankly disappointing lack of progress on curtailing inflation, I expect we will be well above 4% by the end of the year.”

“Sometime next year, we are going to stop hiking rates. At that point, I think we should hold at a restrictive rate for a while to let monetary policy do its work,” he said. “It will take a while for the higher cost of capital to work its way through the economy. After that, if we have to, we can tighten further, based on the data.”

Fed Cook: Ongoing rate hikes required to bring inflation down

Fed Governor Lisa Cook said, “Inflation is too high, it must come down and we will keep at it until the job is done. This likely will require ongoing rate hikes and then keeping policy restrictive for some time.”

“Policy must be based on whether we see inflation actually falling in the data, rather than just in forecasts. Policy should remain focused on restoring price stability, which will also set the foundation for a sustainably strong labor market,” she said.

Japan Suzuki: We are confronting speculators strictly

Japan stepped up verbal intervention as USD/JPY breaks above 150 level. Finance Minister Shunichi Suzuki warned today, “we are confronting speculators strictly.”

Yet, when asked if Yen was under attack by speculators, Suzuki said, “it’s inappropriate for me to comment on such a question under the current circumstances.”

Regarding BoJ policy, he said, “I’m not in a position to comment anything concrete. We’ll strive to maintain fiscal discipline with a major target of achieving primary budget surplus in fiscal 2025.”

Japan CPI core rose to 3% yoy in Sep

Japan headline CPI was unchanged at 3.0% yoy in September, below expectation of 3.1% yoy. CPI core (all items ex-fresh food) accelerated from 2.8% yoy to 3.0% yoy, matched expectations. CPI core-core (all items ex-fresh food and energy) accelerated from 1.6% to 1.8% yoy, below expectation of 2.0% yoy.

CPI core has now exceeded BoJ’s target for the 6th straight months, and hit the highest level since 1991 (excluding the effect of the 2014 sales tax hike). CPI core-core was also at the highest level since 2015. Yet, BoJ is seeing inflation as mostly driven by imports rather than domestic price pressures. This could be reflected in the 5.6% yoy rise in goods prices, and the sluggish 0.2% yoy rise in services prices.

NZ exports rose 37.% yoy in Sep, imports rose 16% yoy

New Zealand good exports rose 37% yoy or NZD 1.6B to NZD 6B in September. Goods imports rose 16% yoy or NZD 1.1B to NZD 7.6B. Monthly trade balance reported a deficit of NZD -1.6B.

Exports to all major trading partners were up, including China (+31% yoy), Australia (+33% yoy), USA (+13% yoy), EU (+21% yoy), and Japan (+42% yoy).

Imports from all major trading partners rose, except EU, including China (+20% yoy), EU (-5.3% yoy), Australia (+11% yoy), USA (+26% yoy), and Japan (+14% yoy).

Looking ahead

UK retail sales data is the main focus in European session. Later in the day, Canada will also release retail sales and new housing price index. Eurozone will release consumer confidence.

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.71; (P) 150.00; (R1) 150.44; More…

USD/JPY’s rally continues today and stays above 150 handle, without clear sign of intervention by Japan. Intraday bias stays on the upside. Current up trend would target 100% projection of 130.38 to 140.33 from 145.89 at 155.84 next. On the downside, break of 149.54 minor support will turn intraday bias neutral and bring consolidations But near term outlook will remain bullish as long as 145.89 resistance turned support holds.

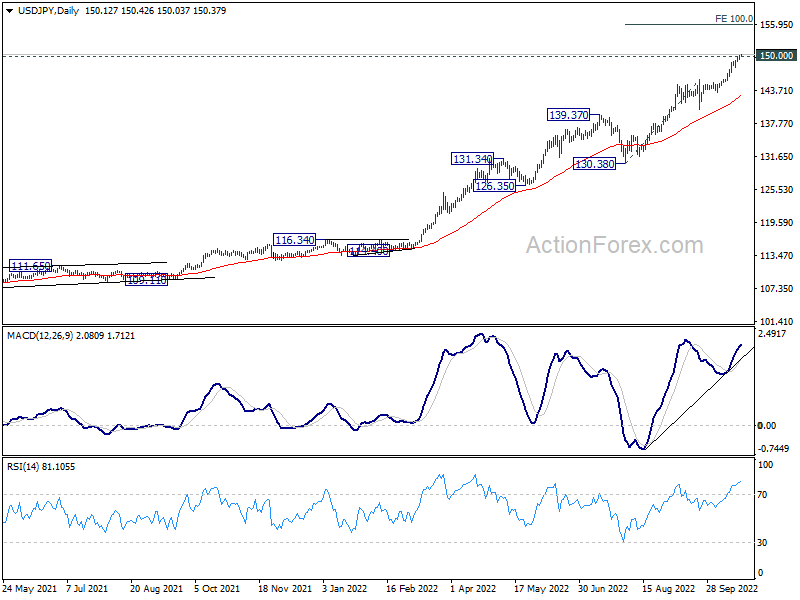

In the bigger picture, up trend from 101.18 is still in progress, as part of the whole up trend from 75.56 (2011 low). 147.68 (1998 high) was already met and there is no clearly sign of topping yet. In any case, break of 140.33 support is needed to be the first sign of medium term topping. Otherwise, further rise is in favor to next target at 160.16 (1990 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Sep | -1615M | -1413M | -2447M | -2625M |

| 23:01 | GBP | GfK Consumer Confidence Oct | -47 | -52 | -49 | |

| 23:30 | JPY | National CPI Core Y/Y Sep | 3.00% | 3.00% | 2.80% | |

| 06:00 | GBP | Retail Sales M/M Sep | -0.50% | -1.60% | ||

| 06:00 | GBP | Retail Sales Y/Y Sep | -5.00% | -5.40% | ||

| 06:00 | GBP | Retail Sales ex-Fuel M/M Sep | -0.30% | -1.60% | ||

| 06:00 | GBP | Retail Sales ex-Fuel Y/Y Sep | -5% | |||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Sep | 12.3B | 11.1B | ||

| 12:30 | CAD | New Housing Price Index M/M Sep | 0.20% | 0.10% | ||

| 12:30 | CAD | Retail Sales M/M Aug | 0.20% | -2.50% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Aug | % | -3.10% | ||

| 14:00 | EUR | Eurozone Consumer Confidence Oct P | -30.3 | -28.8 |

{kind=link}