Dollar is staying generally firm today but lacks clear-cut momentum to extend last week’s rally. Overall sentiment is mildly on the risk-off side, with major European indexes and US futures in red while benchmark treasury yields jump. For now, Yen remains the worst performer for the day, followed by Kiwi and then Aussie. Swiss Franc and Sterling are the stronger ones, followed by the greenback. The question is on whether Dollar could pick up momentum again, probably with help from hawkish Fedspeaks.

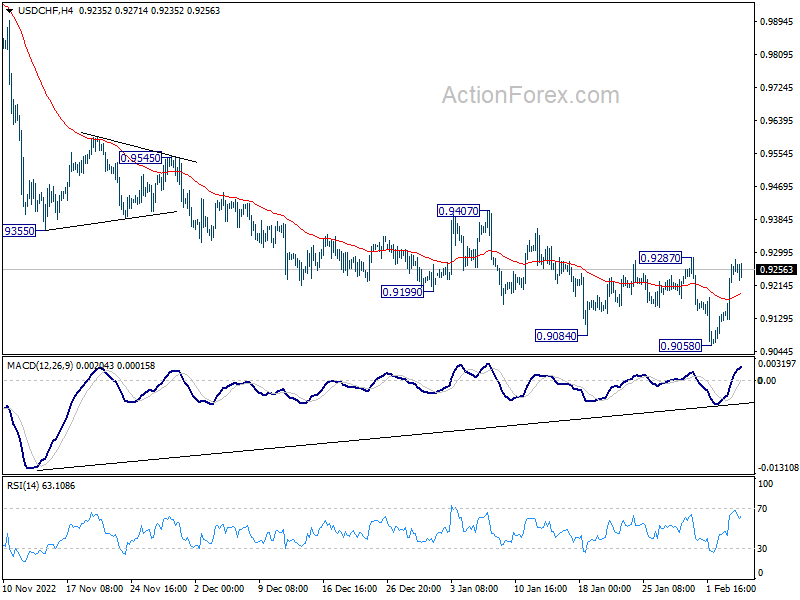

Technically, to solidify more upside momentum in Dollar, USD/CHF will need to break through 0.9287 resistance in USD/CHF to confirm short term bottom. The pair might look into GBP/CHF for some help. A rebound could be due as GBP/CHF is already close to support zone of 1.1045/1094. Break of 1.1206 minor resistance with be a sign of bottoming and turn bias back to the upside for 1.1433 resistance. That might give USD/CHF an extra lift.

In Europe, at the time of writing, FTSE is down -0.69%. DAX is down -0.86%. CAC is down -1.31%. Germany 10-year yield is up 0.1007 at 2.291. Earlier in Asia, Nikkei rose 0.67%. Hong Kong HSI dropped -2.02%. China Shanghai SSE dropped -0.76%. Singapore Strait Times rose 0.05%. Japan 10-year JGB yield rose 0.0094 to 0.500.

BoE hawk Mann: Next step more likely another hike than a cut or hold

BoE MPC member Catherine Mann, a known hawk, said in a speech that “we need to stay the course, and in my view the next step in Bank Rate is still more likely to be another hike than a cut or hold.”

She noted that “some (global) central bankers are seeing a turning point in data to which they are responding with an inflection in their respective policy paths”.

Also, “recent market chatter has focused on when central banks will stop hiking and if they will reverse, with fears torn between the risks of overtightening and stopping too soon.

But for assessment on the turning point, she is looking for “significant and sustained deceleration in higher frequency price increases and in the underlying inflation measures and expectations towards inflation rates that are consistent with achieving the 2% target”.

She emphasized, “uncertainty around turning points should not motivate a wait-and-see approach, as the consequences of under tightening far outweigh, in my opinion, the alternative.”

UK PMI construction dropped to 48.4, weakest in 2 1/2 years

UK PMI Construction dropped slightly from 48.8 to 48.4 in January, below expectation of 49.5. S&P Global noted that residential work had the steepest drop for 32 months. New orders and employment continued to decrease. But business activity expectations rebounded.

Tim Moore, Economics Director at S&P Global Market Intelligence, said: “A sharp and accelerated decline in house building activity led to the weakest UK construction sector performance for just over two-and-a-half years in January…. However, there were positive signals for longer-term prospects across the construction sector, with business activity expectations staging a swift rebound from the low point seen last December.”

Eurozone Sentix rose to -8 in Feb, stagnation with mini-growth the consequence

Eurozone Sentix Investor Confidence rose from -17.5 to -8.0 in February, above expectation of -11.8. That;s also the highest since March 2022. Current Situation Index rose from -19.3 to -10.0, highest since June 2022. Expectations Index rose from -15.8 to -6.0, highest since February 2022. All three indexes had the fourth increase in a row.

Sentix said: “Up to now, investors have been assuming a recession, the course of which was initially expected to be severe but has now eased considerably. With the recent improvement, the scenario of stagnation is gaining in contour. The absence of an energy crisis and the rosy corporate news are contributing to the turnaround from the original recessionary path.”

“However, the following must be critically observed: So far, the improvement in all subcomponents is running at a negative level. In addition, it is noticeable that the expectations component is hardly running ahead of the current situation. Normally, at economic turning points, the expectations values turn positive much faster, while the current situation is still deep in the red. In these cases, a new, positive perspective emerges. However, this has not been the case so far! Investors expect the status quo of the economy to be maintained to some extent. Stagnation with mini-growth would be the consequence.”

Eurozone retail sales dropped -2.7% mom in Dec, EU down -2.6% mom

Eurozone retail sales volume dropped -2.7% mom in December, worse than expectation of -2.5% mom. The volume of retail trade decreased by -2.9% for food, drinks and tobacco and by -2.6% for non-food products, while it grew by 2.3% for automotive fuels.

EU retail sales contracted -2.6% mom. Among Member States for which data are available, the largest monthly decreases in the total retail trade volume were registered in the Netherlands (-6.3%), Germany (-5.3%) and Luxembourg (-3.8%). The highest increases were observed in Slovakia (+2.3%), Austria (+1.6%) and Romania (+1.3%).

ECB Holzmann: Monetary policy must continue to show its teeth

ECB Governing Council member Robert Holzmann said in a conference, “the risk of over-tightening seems dwarfed by the risk of doing too little.”

“Monetary policy must continue to show its teeth until we see a credible convergence to our inflation target,” he added.

Holzmann also hailed that the central bank’s timely tightening helped keep inflation expectation anchored, but people were still feeling the impact. “Ultimately, the losses we as euro-area policymakers incur by consistently missing our inflation target come at our own peril.”

BoJ Kuroda: Monetary easing steps a necessary approach shared by others

BoJ Governor Haruhiko Kuroda told the parliament today, “with our monetary easing steps, we sought to stimulate economic activity and tighten the labour market so that prices and wages would rise more.”

“This was a necessary approach and one that is shared by other central banks,” he said. There was “no better way” to aim at sustainably achieving its 2% inflation target.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9154; (P) 0.9211; (R1) 0.9317; More…

No change in USD/CHF’s outlook as intraday bias remains neutral, with focus on 0.9285 resistance. Firm break there will confirm short term bottoming at 0.9058, and bring stronger rise to 0.9407 resistance. On the downside, however, sustained break of 0.9058 will resume larger decline from 1.0146 instead.

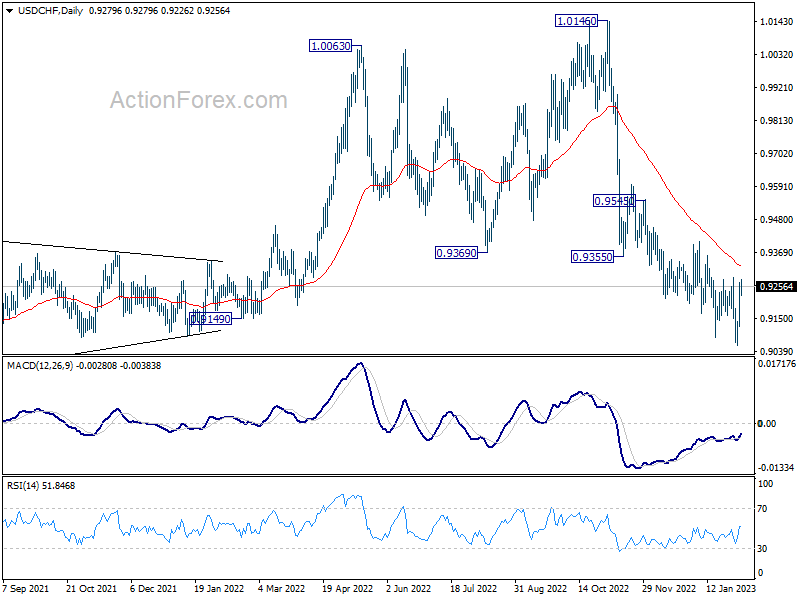

In the bigger picture, rise from 0.8756 (2021 low) has completed at 1.0146, well ahead of 1.0342 long term resistance (2016 high). Based on current downside momentum, fall from 1.0146 should be a medium term down trend itself. Next target is a test on 0.8756 low. Strong support should be seen there to bring rebound. Still, further decline will now be expected as long as 0.9407 resistance holds, in any case.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | AUD | TD Securities Inflation M/M Jan | 0.90% | 0.20% | ||

| 07:00 | EUR | Germany Factory Orders M/M Dec | 3.20% | 2.00% | -5.30% | -4.40% |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Feb | -8 | -11.8 | -17.5 | |

| 09:30 | GBP | Construction PMI Jan | 48.4 | 49.5 | 48.8 | |

| 10:00 | EUR | Eurozone Retail Sales M/M Jan | -2.70% | -2.50% | 0.80% | 1.20% |

| 15:00 | CAD | Ivey PMI Jan | 42.3 | 33.4 |

{kind=link}