Dollar rises broadly in Asian session as helped by mild risk aversion. Nikkei hits a 2-week love as heavyweight technology stocks slip. Yen softens at the same time, after a former staff of the top runner for BoJ Governor Kazuo Ueda said he’s neither hawkish nor dovish, but data dependent. Kiwi and Euro are following the greenback as next stronger. Canadian and Swiss Franc follow Yen as next weakest. Overall, much volatility is expected in the week with BoJ Governor hearing in parliament, US and UK CPI data.

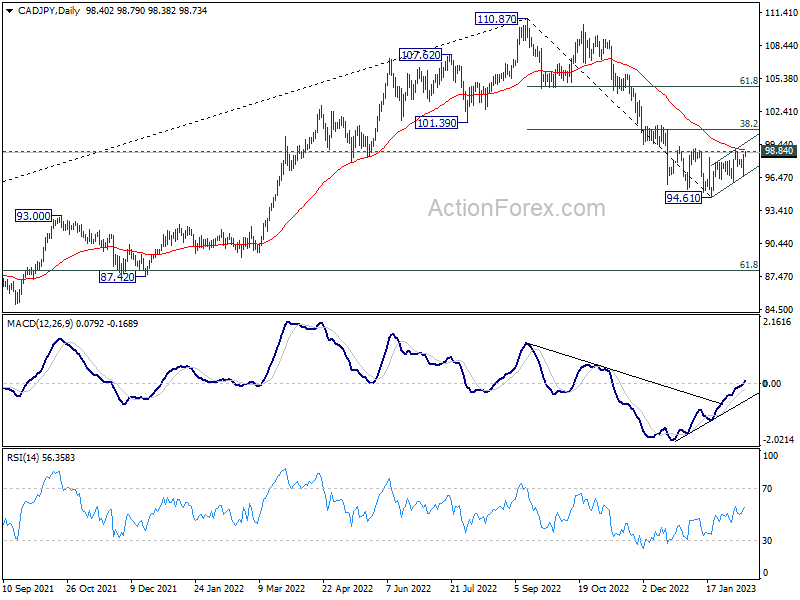

Technically, CAD/JPY looks ready to resume the choppy recovery from 94.61. Break of 98.84 resistance will bring stronger rise to 38.2% retracement of 110.87 to 94.61 at 100.82, even as a corrective move. The development, if happens, should be accompanied by break of 132.89 resistance in USD/JPY. A question is whether EUR/JPY and GBP/JPY would follow by breaking through 147.79 and 161.80 respectively.

In Asia, at the time of writing, Nikkei is down -1.05%. Hong Kong HSI is down -0.47%. China Shanghai SSE is up 0.53%. Singapore Strait Times is down -0.75%. Japan 10-year JGB yield is up 0.0083 at 0.499.

ECB Visco: Tightening should continue in a progressive but measured way

ECB Governing Council member Ignazio Visco said on Saturday, interest rates must continue to rise “in a progressive but measured way, on the basis of the incoming data and their use in the assessment of the inflation outlook”. But when asked how far interest rates could rise, he replied “we don’t know”.

Visco also said, “today, disinflation is obviously needed, but given the levels of private and public debts that prevail in the euro area, we must be careful to avoid engineering an unnecessary and excessive rise in real interest rates.”

“Indeed, I am convinced that the credibility of our actions is preserved not by flexing our muscles in the face of inflation, but by continually showing wisdom and balance.”

NZ BusinessNZ services rose to 54.5, but negative comments trend higher

New Zealand BusinessNZ Performance of Services Index rose from 52.0 to 54.5 in January. Looking at some details, activity/sales rose form 51.9 to 52.1. Employment rebounded strongly from 46.9 to 51.9. New orders/business dropped from 57.7 to 54.5. Stocks/inventories rose from 51.6 to 54.3. Supplier deliveries dropped from 53.9 to 52.0.

BusinessNZ chief executive Kirk Hope said: “Despite the halt in lower expansionary levels, the trend of a higher proportion of negative comments continued in January (61.7%), compared with 58.2% in December and 47.3% in November. The holiday season was a common theme, along with the shortage of labour and general market uncertainty that has been evident for some months now”.

BNZ Senior Economist Doug Steel said that “as encouraging as January’s PSI result might look, we are reluctant to read too much into one month’s result – especially around the holiday period”.

CPI to take center stage again

Consumer inflation data will once again take center stage this week, with CPI from Swiss, US and UK featured. Additionally, US and UK will publish retail sales. Australia and UK will release employment data.

In terms of central bank activities, main focus will be on nomination of the next BoJ Governor and Deputies. ECB will publish monthly economic bulletin.

Here are some highlights for the week:

- Monday: New Zealand BusinessNZ Services; Swiss CPI.

- Tuesday: Japan GDP; Australia NAB business confidence; New Zealand inflation expectations; UK employment; Swiss PPI; Eurozone GDP revision, employment change; US CPI.

- Wednesday: Japan tertiary industry index; UK CPI, RPI; Eurozone industrial production, trade balance; Canada housing starts, manufacturing sales, wholesale sales; US retail sales, Empire State manufacturing, industrial production, business inventories, NAHB housing index.

- Thursday: Japan trade balance, machinery orders; Australia employment; ECB monthly bulletin; US PPI, Philly Fed manufacturing, jobless claims, housing starts and building permits.

- Friday: UK retail sales; current account; Canada IPPI and RMPI; US import prices.

USD/JPY Daily Outlook

Daily Pivots: (S1) 130.21; (P) 131.04; (R1) 132.28; More…

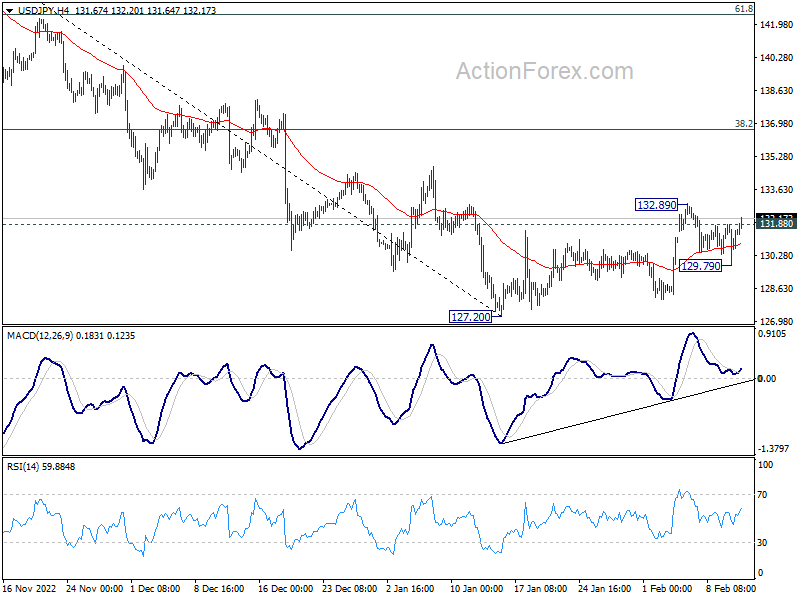

USD/JPY’s break of 131.88 minor resistance suggests that pull back from 132.89 has completed at 129.79 already. Intraday bias is back on the upside for 132.89 first. Break there will resume whole rebound from 127.20. Further rally should then be seen to 38.2% retracement of 151.93 to 127.20 at 136.64, even as a correction to the decline from 151.39. For now, further rally is in favor as long as 129.79 support holds, in case of retreat.

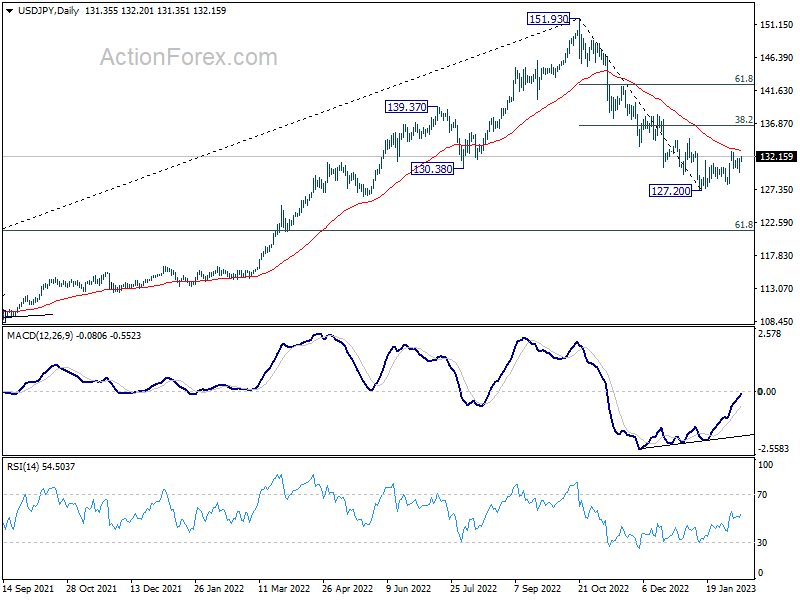

In the bigger picture, prior of 55 week EMA (now at 131.47) raises the chance of medium term bearish reversal, but that’s not confirmed yet. Strong rebound from current level, followed by sustained break of 38.2% retracement of 151.93 to 127.20 at 136.64 will argue that price actions from 151.93 is merely a corrective pattern. However, rejection by 136.64 will solidify medium term bearishness for 61.8% retracement of 102.58 to 151.93 at 121.43 and 38.2% retracement of 75.56 to 151.93 at 122.75.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | BusinessNZ Services Index | 54.5 | 52.1 | 52 | |

| 07:30 | CHF | CPI M/M Jan | 0.50% | -0.20% | ||

| 07:30 | CHF | CPI Y/Y Jan | 2.70% | 2.80% |

{kind=link}