Commodity currencies are experiencing selling pressure in Asian trading due to mild risk off sentiment. New Zealand Dollar is under added pressure following poor retail sales data. US Dollar and Japanese Yen are currently among the stronger currencies, with the latter showing little reaction to the dovish remarks made by the incoming BoJ Governor. Meanwhile, the European majors are showing a mixed performance, with Sterling having a slight advantage.

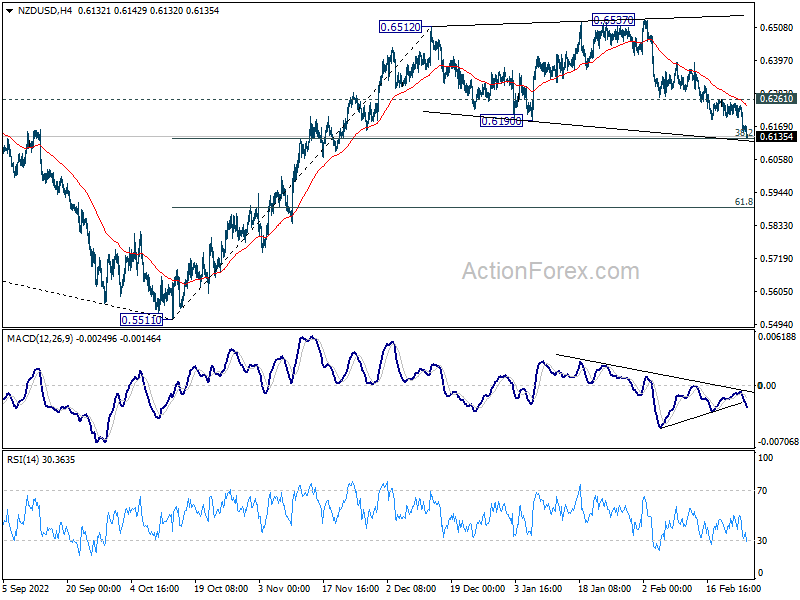

Technically, NZD/USD is extending the decline from 0.6537 and it’s pressing key fibonacci level at 38.2% retracement of 0.5511 to 0.6512 at 0.6130. Strong support could be seen there to bring rebound, and break of 0.6261 resistance will indicate short term bottoming. However, sustained break of 0.6130 increase the likelihood of bearish reversal and lead to a deeper fall towards the 61.8% retracement at 0.5893.

In Asia, Nikkei closed down -0.11%. Hong Kong HSI is down -0.67%. China Shanghai SSE is down -0.23%. Singapore Strait Times is down -0.31%. Japan 10-year JGB yield is down -0.0011 at 0.504.

ECB Visco: If we need to be more restrictive, we’ll be more restrictive

ECB Governing Council member Ignazio Visco told Bloomberg TV on Saturday, “I don’t think that we can indicate now what the terminal rate will be, not even if it’ll be 3.5%, 3.25% or 3.75%, because really it is data-dependent.

“Our objective is to go back to an inflation rate of 2% in the medium term. If we need to be more restrictive, we’ll be more restrictive,” he said.

Visco said “determined” steps are needed in Q2. “We have to be sure that core inflation isn’t remaining at this high level… This may induce wage increases beyond what is compatible with a medium-term 2% inflation rate, which is our target. So that is why we are observing this with a lot of care — but I’m not worried.”

BoJ Ueda: Benefits of current policy exceed the costs

Incoming BoJ Governor Kazuo Ueda told the upper house of parliament today, “there’s still some distance for Japan to see inflation sustainably and stably meet the BoJ’s 2% target.”

“Big improvements must be made in Japan’s trend inflation for the BoJ to shift towards monetary tightening,” he said.”It’s not that I have no ideas on how to tweak the BoJ’s current policy. But the desirable tweak will vary depending on economic changes at the time.”

“In guiding monetary policy, central banks must weigh the benefits and costs of each step,” Ueda said. “At present, the benefits of the BoJ’s current policy exceed the costs.”

“There are various side-effects emerging, but the BoJ’s current policy is necessary and appropriate” to achieve its 2% inflation target, he said.

NZ retail sales volume dropped -0.6% qoq in Q4, value up 1.7% qoq

New Zealand retail sales volume dropped -0.6% qoq in Q4, below expectation of 0.2% qoq rise. Retail sales value rose 1.7% qoq.

By industry, the largest movements in sales volume were: electrical and electronic goods retailing (down -9.7%), motor vehicle and parts retailing (up 2.3%), food and beverage services (up 2.4%), fuel retailing (up 2.6%), furniture, floor coverings, houseware, and textile goods (down -5.2%).

Focuses turn back to economic data

Major focuses will turn back economic data this week. Most attention will be on US consumer confidence and ISMs, Eurozone CPI flash’, Canada GDP, Australia CPI and GDP, New Zealand retail sales and business confidence, and. China PMIs

ECB minutes will also be watched closely. But they’ll likely just repeat that March move would be a 50bps rate hike. Beyond that, the path will depend on incoming data and economic outlook, in particular the economic projections to be published at next meeting.

Here are some highlights for the week:

- Monday: New Zealand retail sales; Eurozone M3 money supply; Canada current account; US durable goods orders, pending home sales.

- Tuesday: Japan industrial production, retail sales, housing starts; New Zealand ANZ business confidence; Australia current account, retail sales; Germany import prices; France GDP, consumer spending; Swiss GDP, KOF economic barometer; Canada GDP, US goods trade balance, house price index, Chicago PMI; consumer confidence.

- Wednesday: New Zealand building permits; Australia GDP, CPI; Japan PMI manufacturing final; China PMIs, Caixin PMI manufacturing; Germany CPI flash; Swiss retail sales, PMI manufacturing; Eurozone PMI manufacturing final; UK PMI manufacturing final, mortgage approvals; Canada PMI manufacturing; US ISM manufacturing, construction spending.

- Thursday: Australia building approvals; Japan monetary base, capital spending, consumer confidence; Eurozone CPI flash, unemployment rate, ECB meeting accounts; US jobless claims.

- Friday: Japan Tokyo CPI, unemployment rate; China Caixin PMI services; Germany trade balance; France industrial production; Eurozone PMI services final, PPI; UK PMI services final; Canada building permits, labor productivity; US ISM services.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6688; (P) 0.6756; (R1) 0.6793; More…

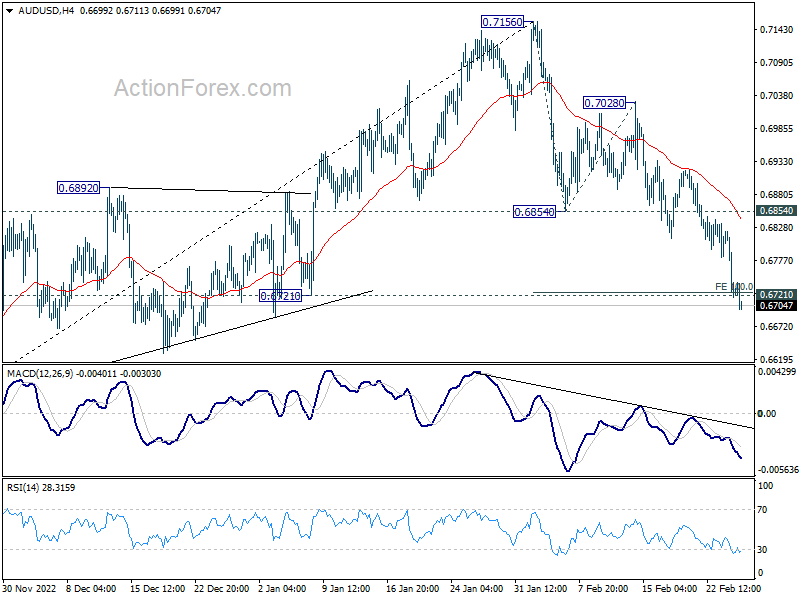

AUD/USD’s fall from 0.7156 continues today and breaks 0.6721 support. Current development argues that near term trend could be reversing. Intraday bias stays on the downside. Deeper decline would be seen to 161.8% projection of of 0.6854 to 0.7028 from 0.6854 at 0.6539. On the upside, break of 0.6854 support turned resistance is needed to indicate completion of the fall, or risk will stay on the downside in case of recovery.

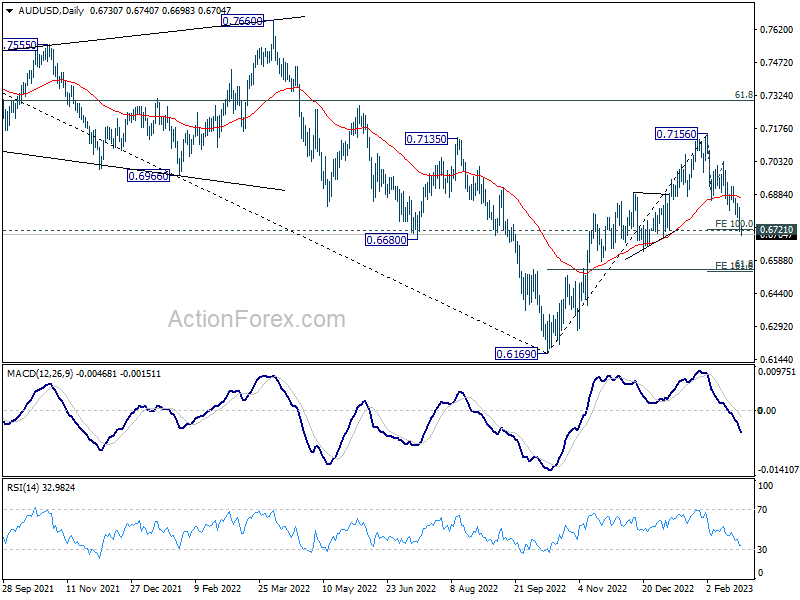

In the bigger picture, focus is now on 0.6721 structural support. Sustained break there will argue that whole rise from 0.6169 (2022 low) has completed at 0.7156, after rejection by 55 month EMA (now at 0.7179). Deeper decline would then be see back to 61.8% retracement of 0.6169 to 0.7156 at 0.6546, even as a corrective fall. Nevertheless, strong rebound from current level will retain medium term bullishness for another rise through 0.7156 later.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Retail Sales Q/Q Q4 | -0.60% | 0.20% | 0.40% | 0.60% |

| 21:45 | NZD | Retail Sales ex Autos Q/Q Q4 | -1.30% | 0.30% | 0.40% | 0.50% |

| 00:30 | AUD | Company Gross Operating Profits Q/Q Q4 | 10.60% | 1.50% | -12.40% | -11.50% |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Jan | 4.20% | 4.10% | ||

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Feb | 101 | 99.9 | ||

| 10:00 | EUR | Eurozone Industrial Confidence Feb | 2 | 1.3 | ||

| 10:00 | EUR | Eurozone Services Sentiment Feb | 12.4 | 10.7 | ||

| 10:00 | EUR | Eurozone Consumer Confidence Feb F | -19 | -19 | ||

| 13:30 | CAD | Current Account (CAD) Q4 | -11.0B | -11.1B | ||

| 13:30 | USD | Durable Goods Orders Jan | -4.00% | 5.60% | ||

| 13:30 | USD | Durable Goods Orders ex Transportation Jan | 0.00% | -0.20% | ||

| 15:00 | USD | Pending Home Sales M/M Jan | 0.90% | 2.50% |

{kind=link}