Euro is digesting this week’s gains in Asian session, as traders turn their focus to flash CPI data from Eurozone. Market analysts believe that a 50bps hike by ECB this month is already a “done deal”, as affirmed by rate-setters on several occasions. However, how far ECB will go with tightening measures depends very much on the upcoming economic projections, which are expected to be impacted by today’s data release.

Elsewhere in market, Dollar is also showing some strength, supported by extended rally in treasury yields. On the other hand, Swiss Franc and Sterling, along with Aussie and Kiwi, are experiencing weakness.

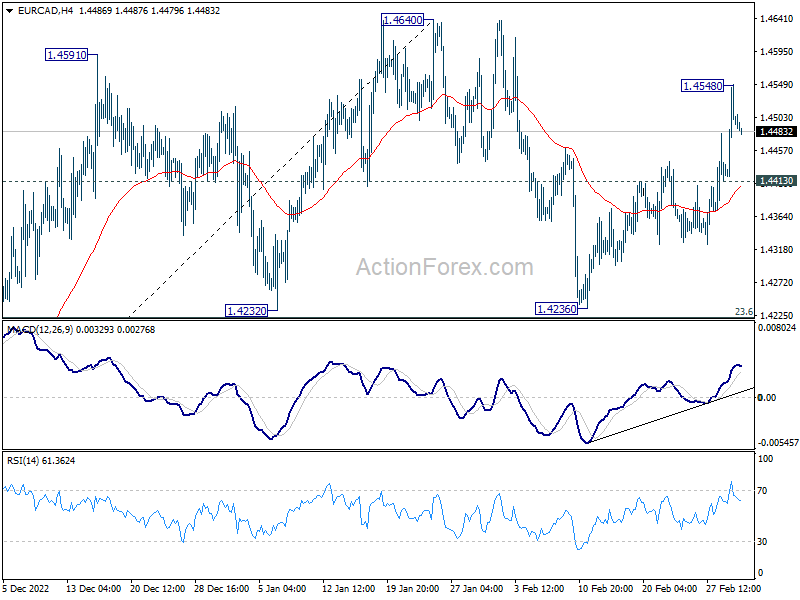

From a technical perspective, rebound of EUR/CAD from 1.4236 is currently taking a breather after reaching 1.4548. However, further rise is expected as long as the minor support level at 1.4413 holds. A break above 1.4548 will target 1.4640 high, and a decisive break there should resume larger uptrend from 1.2867. Furthermore, if a break of 1.4640 occurs, it could also be accompanied by a stronger rebound in EUR/USD towards 1.1032 high.

In Asia, Nikkei dropped -0.06%. Hong Kong HSI is down -0.73%. China Shanghai SSE is up 0.06%. Singapore Strait Times is down -0.59%. Japan 10-year JGB yield is up 0.0003 at 0.508. Overnight, DOW rose 0.02%. S&P 500 dropped -0.47%. NASDAQ dropped -0.66%. 10-year yield rose 0.078 to 3.994, after hitting 4.006.

US 10-year yield breaks 4% on inflation worry, more upside ahead

US treasury yields marched higher overnight, and look set to extend rally today. Two-year yield hit its highest level in 16 years and could soon challenge the 5% handle, while 10-year yield remains above the 4% handle in the Asian session.

It’s believed that persistent worries about inflation remaining at a higher level for an extended period are driving the moves. As a result, Fed may respond by accelerating the tightening pace again. There is growing expectation in the market that Fed will implement a 50bps rate hike on March 22, with a 30% chance of this happening compared to 24% a week ago. Moreover, there is a 55% chance that rate will peak at 5.50-5.75% in July.

Furthermore, the recent surge in European yields is considered an even stronger reason for the rally in US yields. The recovery in EUR/USD reflects this sentiment. Germany 10-year yield hitting the highest level since 2011 on similar worries about inflation and ECB policies. A peak above 4% for ECB is more likely than ever before, while a rate cut this year is all but ruled out.

From a technical perspective, as long as the support level at 3.863 holds, the rally in US 10-year yield from 3.334 is expected to continue. The current development affirms that correction from 4.333 has completed with three waves down to 3.334. A retest of 4.333 is likely to occur next. While it is still early to predict, the TNX could eventually hit the 61.8% projection of 2.525 to 4.333 from 3.334 at 4.451 before topping out.

Fed Kashkari: Risk of under-tightening greater than over-tightening

Minneapolis Fed President Neel Kashkari said yesterday that he is “open-minded” on either a 25bps or a 50bps rate hike at the March meeting. But he also noted, “I think my colleagues agree with me that the risk of under-tightening is greater than the risk of over-tightening

Kashkari also said, “what’s more important is what we signal in the dot plot… At this point I haven’t decided what my dot is, but I would lean towards continuing to push up my rate and policy path,”

“Given the data in the last month — the inflation report and strong jobs report — these are concerning data points suggesting we’re not making progress as fast as we’d like,” Kashkari said. “At same time we don’t want to overreact.”

Fed Bostic wants rate at 5-5.25% until well into 2024

Atlanta Fed President Raphael Bostic said Fed should hike by 50bps to 5.00-5.25%, and hold it at that level until well into 2024. “We must determine when inflation is irrevocably moving lower,” he wrote in an essay. “We’re not there yet.”

“That’s why I think we need to raise the federal funds rate to between 5-5.25% and leave it there well into 2024. This will allow tighter policy to filter through the economy and ultimately bring aggregate supply and aggregate demand into better balance and thus lower inflation.”

“If we are going to get inflation back in the range of our target, the breadth of inflation will have to narrow considerably,” Bostic wrote. “When inflation is no longer top of mind, our mission will largely be accomplished. We are clearly not there yet. But I—and the Committee—are committed to doing all we can to ensure that we get there as soon as possible.”

BoJ Takata: We need to patiently maintain monetary easing

BoJ board member Hajime Takata said said in a speech today, “now is the time where the BOJ must scrutinise whether the economy and prices can achieve a sustained, positive cycle.”

“While we need to be mindful of the impact of our massive stimulus program on market function, we’re at a stage where we need to patiently maintain monetary easing,” he said.

Looking ahead

Eurozone CPI flash is a major focus in European session while unemployment rate will be released too. ECB minutes will also be published. Later in the day, US will release jobless claims and non-farm productivity.

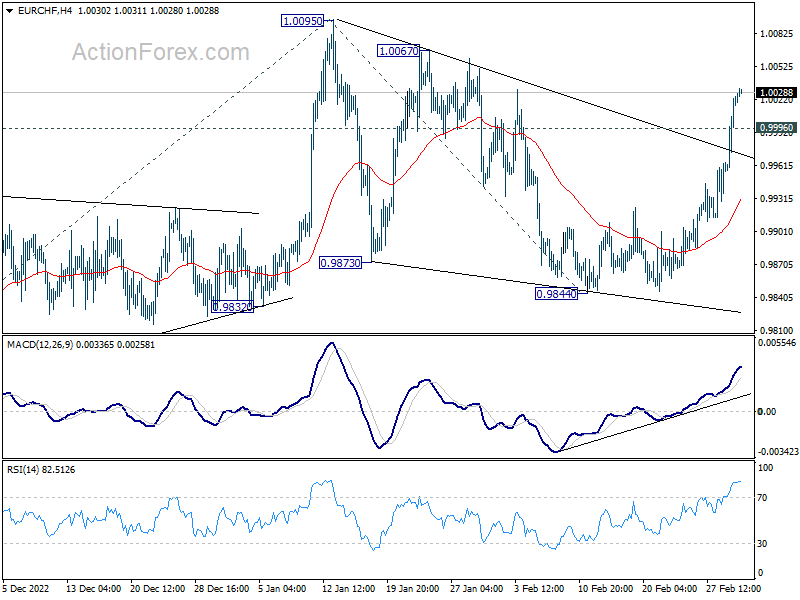

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9980; (P) 1.0004; (R1) 1.0049; More….

Intraday bias in EUR/CHF stays on the upside as rise from 0.9844 is in progress. The strong break of trend line resistance adds to the case that corrective pattern from 1.0095 should have completed with three waves down to 0.9844. Further rally should be seen back to retest 1.0095 high. On the downside, below 0.9996 minor support will turn intraday bias neutral and bring consolidations, before staging another rally.

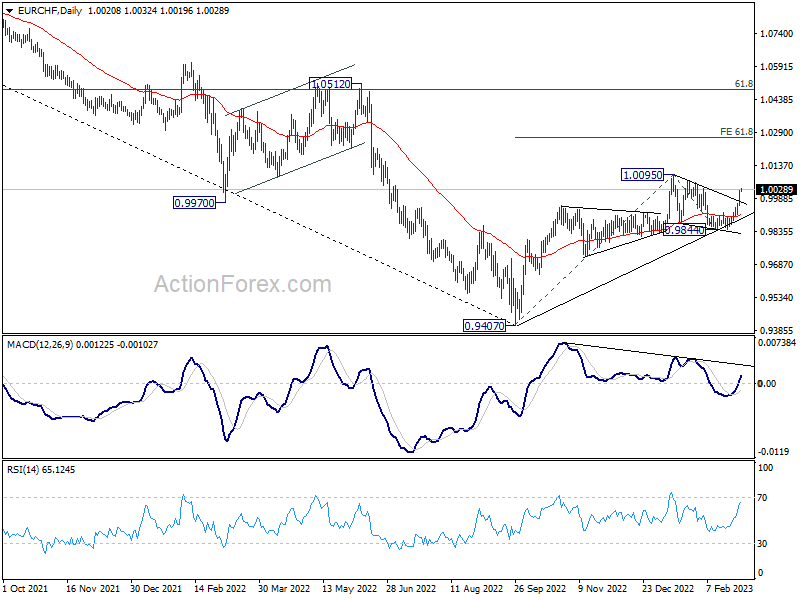

In the bigger picture, with 0.9832 support intact, rise from 0.9407 (2022 low) is still expected to continue. Break of 1.0095 and sustained trading above 55 week EMA (now at 1.0021) will be a medium term bullish signal, and bring further rally to 1.0505 cluster resistance (2020 low at 1.0505, 61.8% retracement of 1.1149 to 0.9407 at 1.1484). However, firm break of 0.9832 support will revive medium term bearishness and bring retest of 0.9407 low instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Terms of Trade Index Q4 | 1.80% | -1.70% | -3.40% | -3.90% |

| 23:50 | JPY | Capital Spending Q4 | 7.70% | 6.90% | 9.80% | |

| 23:50 | JPY | Monetary Base Y/Y Feb | -1.60% | -3.20% | -3.80% | |

| 00:30 | AUD | Building Permits M/M Jan | -27.60% | -7.60% | 18.50% | |

| 05:00 | JPY | Consumer Confidence Feb | 31.1 | 32 | 31 | |

| 09:00 | EUR | Italy Unemployment Jan | 7.80% | 7.80% | ||

| 10:00 | EUR | Eurozone Unemployment Rate Jan | 6.60% | 6.60% | ||

| 10:00 | EUR | Eurozone CPI Y/Y Feb P | 8.20% | 8.60% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Feb P | 5.30% | 5.30% | ||

| 12:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 13:30 | USD | Initial Jobless Claims (Feb 24) | 196K | 192K | ||

| 13:30 | USD | Nonfarm Productivity Q4 | 2.50% | 3.00% | ||

| 13:30 | USD | Unit Labor Costs Q4 | 1.40% | 1.10% | ||

| 15:30 | USD | Natural Gas Storage | -72B | -71B |

{kind=link}