Euro is leading European majors higher today, with a little boost from improving consumer sentiment in Germany. However, it is likely that the rise is more due to concerns over regional bank woes in the US, which are triggering some risk-off sentiment. Australian Dollar is the worst performer for the day, with selloffs deepening, followed by New Zealand and Canadian Dollars. Meanwhile, Dollar is mixed for now, along with Yen. The relative performance of the US and Japanese currencies will largely depend on whether this week’s decline in US treasury yields extends.

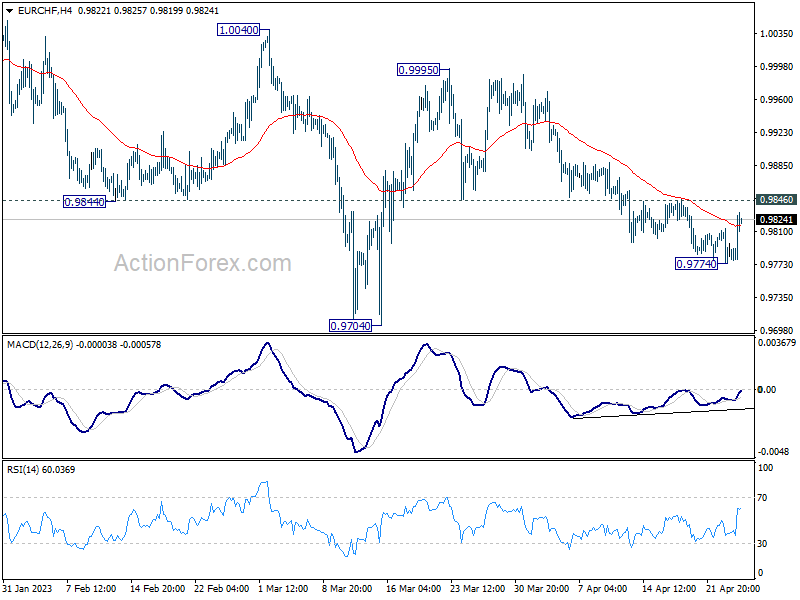

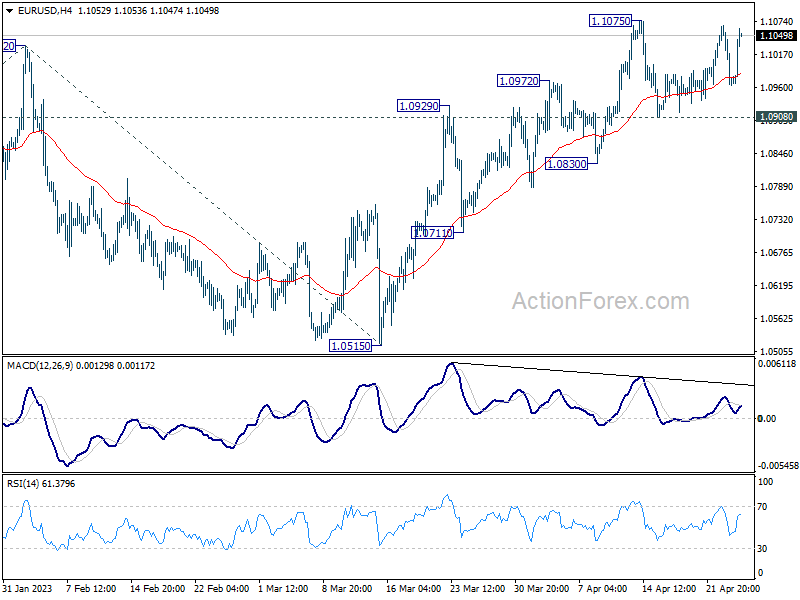

Technically, the main focuses for the US session today will be on 1.1075 resistance in EUR/USD, 0.8858 support in USD/CHF, and to a lesser extent, 1.2545 resistance in GBP/USD. Decisive breaks of these levels will confirm resumption of recent downtrend of Dollar against Europeans. Another focus is the 0.9846 minor resistance in EUR/CHF. A firm break there will confirm short-term bottoming at 0.9774 and bring a stronger rebound. This could help push EUR/USD through the mentioned 1.1075 resistance and possibly prompt upside acceleration above that level.

In Europe, at the time of writing, FTSE is down -0.27%. DAX is down -0.58%. CAC is down -0.95%. Germany 10-year yield is up 0.0022 at 2.387. Earlier in Asia, Nikkei dropped -0.71%. Hong Kong HSI rose 0.71%. China Shanghai SSE dropped -0.02%. Singapore Strait Times dropped -0.08%. Japan 10-year JGB yield dropped -0.0170 to 0.463.

US durable goods orders rose 3.2% mom in Mar, ex-transport orders up 0.3% mom

US durable goods orders rose 3.2% mom to USD 276.4B in March, well above expectation of 0.8% mom. Ex-transport orders rose 0.3% mom to USD 179.0B, above expectation of -0.2% mom. Ex-defense orders rose 3.5% mom to USD 259.3B. Transportation equipment rose 9.1% mom to USD 97.4B.

US goods trade deficit narrowed to USD -84.6B in Mar

US goods exports rose USD 4.9B to USD 172.7B in March. Goods imports dropped USD -2.5B to 257.3B. Trade deficit came in at USD -84.6B, smaller than expectation of USD -89.8B.

Wholesale inventories rose 0.1% mom to USD 919.9B. Retail inventories rose 0.7% mom to USD 773.4B.

Germany Gfk consumer sentiment rose to -25.7, improved economic and income expectations

Germany Gfk Consumer Sentiment for May improved from -29.3 to -25.7, above expectation of -27.5. In April, Economic Expectations rose sharply from 3.7 to 14.3. Income Expectations rose from -24.3 to -10.7. Propensity to Buy rose from -17.0 to -13.1.

The seventh increase in a row indicates that consumer sentiment is gathering momentum. “Following a rather small increase in the previous month, consumer sentiment is showing clear signs of an upswing this month,” explains Rolf Bürkl, GfK consumer expert.

“However, the value still remains below pre-pandemic levels of around three years ago. On another positive note, income expectations have risen for the seventh time in a row, returning to the level prior to the start of the war in Ukraine for the first time.”

Australia CPI down to 7.0% yoy in Q1, 6.3% yoy in Mar

Australia CPI slowed from 7.8% yoy to 7.0% yoy in Q1, slightly above expectation of 6.9% yoy. For the quarter, CPI rose 1.4% qoq, down from prior 1.9% qoq, below expectation of 1.3% qoq. Trimmed mean CPI rose 1.2% qoq, 6.6% yoy while weighted median CPI rose 1.2% qoq, 5.8% yoy.

Michelle Marquardt, ABS head of prices statistics, said “CPI inflation slowed in the March quarter, with the quarterly rise being the lowest since December 2021. While prices continued to rise for most goods and services, many of these increases were smaller than they have been in recent quarters.”

Monthly CPI slowed from 6.8% yoy to 6.3% yoy in March, below expectation of 6.5% yoy. Excluding volatile items (Fruit and vegetables and Automotive fuel) CPI, rose from 6.8% yoy to 6.9% yoy.

NZ imports surged 10% yoy, export rose 0.6% yoy in Mar

New Zealand goods exports rose 0.6% yoy or NZD 40m to NZD 6.5B in March. Imports rose 10% yoy or NZD 719m to NZD 7.8B. Monthly trade balance recorded a deficit of NZD -1.3B, larger than expectation of NZD -0.5B.

Australia contributed the most to the growth in monthly exports, with a 30% rise. Goods exports to the US was up 4.1%, EU up 28%, but down -9.6% to Japan and down -5.7% to China.

On the other hand, imports from the US leads the monthly rise, up 39%. Imports from EU and South Korea grew 24% and 20% respectively. On the other hand, imports from China was down -13%, Australia down -4.0%.

BoJ Ueda: Dealing with cost-push inflation is very difficult

In an address to parliament today, BoJ Governor Kazuo Ueda highlighted the difficulties central banks face when dealing with cost-push inflation.

Ueda explained, “In general, dealing with cost-push inflation is very difficult for central banks. On the one hand, you’d like to curb inflation. On the other hand, you don’t want to tighten monetary policy knowing that cost-push inflation will cool the economy.”

The governor emphasized the importance of striking the right balance, which he said, “depends on economic developments at the time, including where inflation stood at the outset.”

Ueda also noted that cost-push inflation in Japan is likely to ease as prices of imported raw materials have probably peaked.

These comments come ahead of BoJ’s two-day policy meeting starting on Thursday, during which the central bank is widely anticipated to maintain its ultra-loose monetary policy.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0936; (P) 1.1002; (R1) 1.1039; More…

Immediate focus is back on 1.1075 resistance with today’s rebound in EUR/USD. Decisive break there will resume larger up trend from 0.9534 to 1.1273 fibonacci level. Break there will target 61.8% projection of 0.9534 to 1.1032 from 1.0515 at 1.1441. Meanwhile, outlook will remain bullish as long as 1.0908 support holds, in case of another retreat.

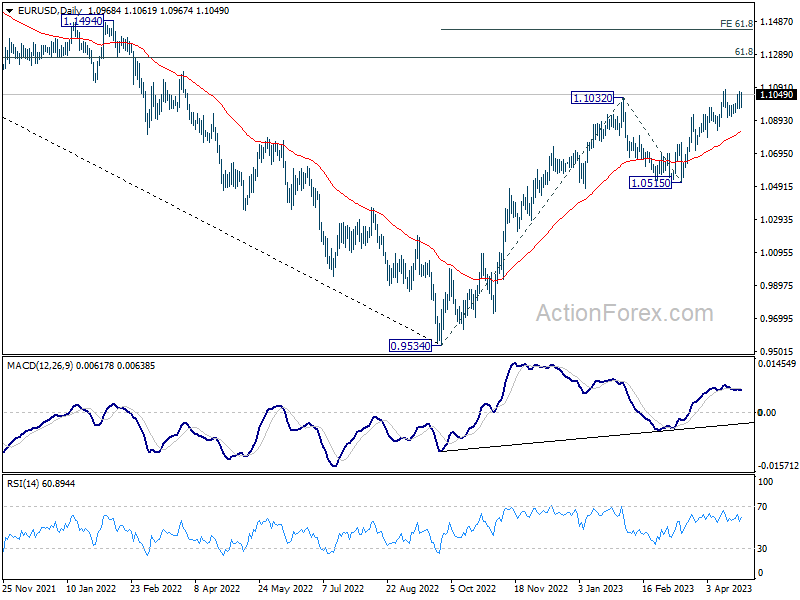

In the bigger picture, rise from 0.9534 (2022 low) is in progress for 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high). This will now remain the favored case as long as 1.0515 support holds, even in case of deeper pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Mar | -1273M | -500M | -714M | |

| 01:30 | AUD | Monthly CPI Y/Y Mar | 6.30% | 6.50% | 6.80% | |

| 01:30 | AUD | CPI Q/Q Q1 | 1.40% | 1.30% | 1.90% | |

| 01:30 | AUD | CPI Y/Y Q1 | 7.00% | 6.90% | 7.80% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Q/Q Q1 | 1.20% | 1.40% | 1.70% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Y/Y Q1 | 6.60% | 7.20% | 6.90% | |

| 06:00 | EUR | Germany Gfk Consumer Confidence May | -25.7 | -27.5 | -29.5 | -29.3 |

| 08:00 | CHF | Credit Suisse Economic Expectations Apr | -33.3 | -41.3 | ||

| 12:30 | USD | Goods Trade Balance (USD) Mar P | -84.6B | -89.8B | -91.6B | |

| 12:30 | USD | Wholesale Inventories Mar P | 0.10% | -0.20% | 0.10% | |

| 12:30 | USD | Durable Goods Orders Mar | 3.20% | 0.80% | -1.00% | |

| 12:30 | USD | Durable Goods Orders ex Transport Mar | 0.30% | -0.20% | -0.10% | |

| 14:30 | USD | Crude Oil Inventories | -1.3M | -4.6M |

{kind=link}